Vermont Business Magazine Today, Speaker Jill Krowinski made the following statement on the House passage of H.955, an act relating to next steps in transforming Vermont’s education system. The bill passed on a 79-62 vote. The vote, as is, would be well-short of the vote needed to override a promised veto from Governor Scott. It has now moved to the Senate.

“Today, the House of Representatives gave final passage to H.955, a landmark education transformation bill built on more than 18 months of community engagement across the state,” said Speaker Krowinski. “The bill makes education more affordable for Vermonters by establishing a new tax framework which includes a tax on second homes that will over time reduce taxes on primary residences. The bill restarts Vermont's school construction program with up to $50 million annually in bonding capacity and full coverage of districts’ existing construction debt.

“H.955 creates seven regional Cooperative Educational Service Areas (CESAs) to deliver services more efficiently, expand access to specialized programs, coordinate transportation and back-office support, especially for small and rural schools. Any merger of school districts is entirely voluntary, decided locally, and must be approved by voters. The bill does not force top-down mergers from the state.

“Vermonters have been clear about what they want: a strong public education system that saves money, expands opportunity for kids, and respects the role of local communities in making decisions,” said Chair Peter Conlon. “H.955 delivers exactly that. A plan grounded in evidence, built through collaboration, and designed to work for Vermont, not against it.”

“This bill is the product of years of listening," said Chair Emilie Kornheiser. “Listening to educators, school boards, parents, and communities in every corner of Vermont. It lowers costs for homeowners, brings real resources to students regardless of their zip code, and finally addresses the school construction crisis we have been putting off for too long.”

“The House took the time to do this work right. We listened to thousands of Vermonters, we worked with education experts and community leaders, and we produced a plan that is thoughtful, fair, and genuinely responsive to what people across this state have been asking for,” said Speaker Krowinski. “The Governor's approach, drafted without meaningful partnership with Vermont communities, built around an unrealistic timeline, and designed by outside consultants rather than Vermonters, is simply not the answer. Vermonters deserve better than that, and this bill delivers it."

Democratic leadership in both the House and Senate favor voluntary school district mergers while Governor Phil Scott insists that the only way toward meaningful cost control is for mandatory school mergers. He said at his weekly press conference on Wednesday that communities have had a decade to work out mergers voluntarily and have failed to do so. He also said that not only have costs risen well beyond just the hike in health care costs (which has also driven school costs higher), but educational outcomes have also suffered, despite Vermont having one of the highest cost-per-pupil spending in the nation.

Joint Fiscal Office

April 13, 2026.

H.955 – An act relating to next steps in transforming Vermont’s education system

As recommended by the House Committee on Ways and Means, Draft 4.21

Bill Summary

This bill would modify the mechanism for supervisory unions to provide regional and statewide services. H.955 would replace Boards of Cooperative Education Services (BOCES) with Cooperative Educational Service Areas (CESAs), and assign the State’s supervisory unions to seven CESAs.3

This bill would specify the minimum shared services CESAs would offer. Additionally, it would require school districts to participate in committees to study forming unified union school districts.

This bill would also amend contingent effective dates within Act 73 (2025), create guidelines for special education funding safeguards, initiate education policy rulemaking, and create systems and reporting on prekindergarten (PreK) administration and costs.

This bill would establish regional assessment districts in statute, further establish property classifications, and significantly amend the State Aid for School Construction Program.

Effective dates and contingencies of this bill vary by section. Appendix 1 of this fiscal note outlines the effective dates and associated contingencies of each section.

Fiscal Impact

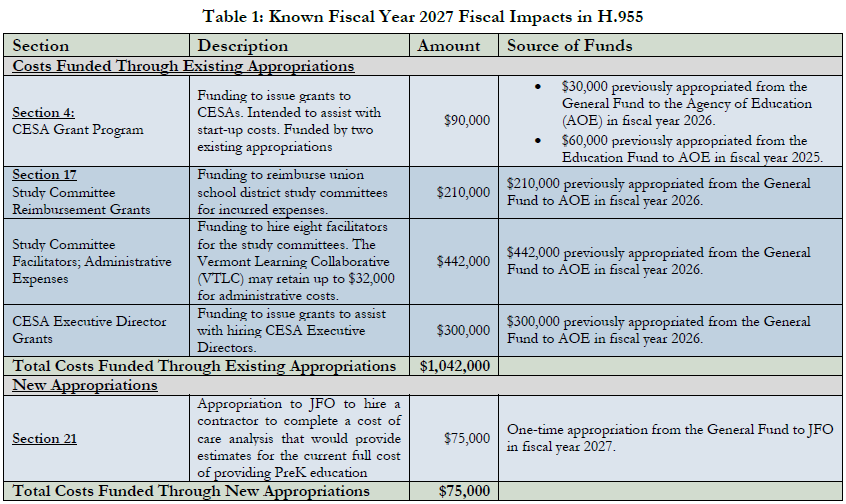

H.955 would amend the uses of funds previously appropriated from the Education and General funds for education transformation. This bill would appropriate $75,000 from the General Fund to the Joint Fiscal Office (JFO) in fiscal year 2027 to hire a contractor to help determine an appropriate funding amount for PreK students. Appropriation changes and new appropriations are summarized in Table 1 of this fiscal note.

The overall fiscal impact of this bill is unclear. Impacts would depend on outstanding policy decisions at the State and local levels. The “Background and Details” section of this fiscal note outlines potential fiscal implications by section.

Background and Details

Section 2: Cooperative Educational Service Areas (CESAs)

Effective July 1, 2026, Section 2 would amend statute to replace Boards of Cooperative Education Services (BOCES) with Cooperative Educational Service Areas (CESAs). A CESA would be a group of supervisory unions (SUs), intended to provide members with shared programs and services in a cost-effective manner. A CESA would be a distinct entity, with a governing board, budget, and employees.

Section 2 would create seven CESAs in statute and specify their member SUs, including the existing Vermont Learning Collaborative (VTLC). CESAs would create their own bylaws; these would include the programs or services offered by the CESA, the financial terms of the CESA, and the required fees for members.

CESA staff would include, initially, an executive director who reports to the CESAs board. The need for additional staff and administrative resources would depend on the services offered. At a minimum, a CESA would offer services related to special education, business and administrative services, and facilitate union school district creation. Participation in services offered by a CESA would be voluntary.

The total fiscal impact of this section is currently unclear. If CESAs offered cost-effective services that member SUs shared, there may be cost savings. However, potential cost savings are unclear, due to outstanding unknowns including the range of services offered, their cost compared to services they are replacing, and participation in services.

The creation and operation of CESAs would necessitate additional expenditures, including the hiring of staff. Total staffing levels are unknown and would likely depend on the services operated by a CESA. In addition to staff, there would likely be non-personnel operating costs for a CESA and its programs.

Section 3: Report Repeal

Effective July 1, 2026, Section 3 would repeal Act 168’s (2024) transition report from the Secretary of Education because it would no longer be relevant. This section is not expected to have a fiscal impact.

Section 4: CESA Start-Up Grant Program

Effective July 1, 2026, Section 4 would amend Act 168’s BOCES grant program so that CESAs would be eligible to receive start-up grants. Each CESA could receive a grant from the Agency of Education (AOE) for $15,000. This grant could offset a CESA’s initial costs, such as creating articles of agreement or bylaws.

This section would make $90,000 available from existing appropriations for providing grants to CESAs in fiscal year 2027. Grants would be partly funded by a fiscal year 2025 Education Fund appropriation to AOE ($60,000). The remaining $30,000 would be funded by a fiscal year 2026 appropriation to AOE in Act 73 (2025), as amended by Sec. C.103 of the fiscal year 2027 appropriations act as passed by the House.

Sections 5-11: CESA Language

Effective July 1, 2026, Sections 5 through 11 would amend statute to replace the term Boards of Cooperative Education Services with Cooperative Educational Service Area. These sections would have no fiscal impact.

Section 12: CESA Transition

Effective July 1, 2026, Section 12 would establish CESA board creation and the timing for the first board meeting. This section would have no fiscal impact.

Section 13: Union School District Study Committees, Reports

Section 13 would set out the process for establishing study committees to explore forming unified union school districts (“union district”). This process would take place between October 1, 2026 and November 7, 2028.

By October 1, 2026, VTLC would be required to hire eight individuals as union school district facilitators. The facilitators would be charged with organizing school districts into study committees to explore forming a unified union school district (“union district”). When creating study committees, the facilitators would use the school district groupings in Section 14 of this bill as guidance, and would consider districts’ net grand list values and current education spending when establishing the final committees. A study committee’s member districts would have a combined average daily membership of at least 2,000 students and would be contiguous. School districts would be required to participate in the committees, and committees would first meet by December 1, 2026.

By December 1, 2027, each study committee would complete and submit a final report outlining whether it found it advisable to form a union district. The report would be submitted to the school boards of districts considered “necessary” or “advisable” to creating the new district. If the committee chose not to form a union district, the report would be issued to the participating districts’ school boards. The boards would have until February 1, 2028, to review the submitted report and any articles of agreement.

If the committee advises forming a union district, its report would be sent to the Secretary of Education. The Secretary would submit the report, along with their recommendation on the proposed union district, to the State Board of Education (SBE) by April 1, 2028. The SBE would have until June 1, 2028, to review and issue its findings on the proposed district. Following the SBE’s review, voters of the districts considered “necessary” or “advisable” for the proposed district’s creation would vote on unification by November 7, 2028.

By February 1, 2027, the AOE must, with facilitator input, submit a report to the House Committees on Education and Ways and Means, and the Senate Committees on Education and Finance. The report would detail the membership and status of the study committees.

The total fiscal impact of this section is unclear. Funds for hiring the facilitators and reimbursing some study committee expenditures are detailed in Section 17. Beyond these funds, committee expenses above the reimbursement grant would be funded by the member districts. All else equal, additional expenditures by school districts would increase statewide Education Spending. If Education Spending increases, the homestead property tax rates and/or the nonhomestead property tax rate would need to be raised.

Section 14: Union School District Groupings

Effective July 1, 2026, Section 14 outlines the 21 district groupings that the facilitators should consider when forming study committees. There is no fiscal impact of this section.

Section 15: Study Committee Results, Facilitator Reports

Effective July 1, 2026, Section 15 would require VTLC’s lead facilitator to submit a report to the House and Senate Committees on Education by January 1, 2029 detailing the final results of each study committee, including factors which impacted the committee’s deliberation. There is no fiscal impact of this section.

Section 16: AOE Report on Boundaries

Effective July 1, 2026, Section 16 would require AOE to submit a report to the House and Senate Committees on Education by January 1, 2029. This report would make recommendations for adjusting SU and CESA boundaries to account for any union districts formed by the study committees. There is no fiscal impact of this section.

Section 17: Grants and Appropriations

Effective July 1, 2026, Section 17 would create several grants to be administered by AOE to assist study committees and CESAs in their work. This section makes the funds associated with these grants an allowable use of the appropriation made in Act 73, as amended by Sec. C.103 of the fiscal year 2027 appropriations act as passed by the House. All appropriations referenced in this section are already accounted for in that bill.

Under this section AOE would reimburse legal and technical expenses of study committees. Each study committee would be eligible for up to $10,000 in reimbursement grants. The total $210,000 would be an allowable use of the appropriation in Act 73 as amended.

The $442,000 grant to VTLC in fiscal year 2027 to hire the study committee facilitators outlined in Section 13 would be an allowable use of the Act 73 appropriation as amended. VTLC could retain up to $32,000 for administrative costs.

Finally, Section 17 would create CESA executive director grants. These grants would each equal $50,000 and would be awarded by AOE to six of the CESAs outlined in this bill; VTLC would be ineligible for these grants. This section would make $300,000 for these grants an allowable use of the Act 73 appropriation as amended.

The fiscal impact of this section would be a net-neutral shift of $952,000 General Fund appropriated in fiscal year 2026. JFO expects that many of these funds would be expended in fiscal year 2027, but some expenditures like the study committee reimbursement grants could occur in fiscal year 2028.

Section 18: Amending Act 73 Effective Dates and Contingencies

Effective on passage, Section 18 would amend effective dates and contingencies for some Act 73 sections. This section would include new contingencies and would push back the timeline for many sections of Act 73 by two years. The revised effective dates and contingencies are summarized in Appendix 1.

The implementation of many education and finance policy sections would still only take effect if certain contingencies are met; this section would amend those contingencies to include:

- school districts have had an opportunity to study the advisability of forming a new union school district, and the clerk of each school district voting on a union district proposal has certified the vote’s results;

- JFO has provided the General Assembly with an analysis comparing total State funds appropriated to school districts under current law to the funds districts would have received under Act 73 by December 15, 2029; and

- the General Assembly has enacted legislation that addresses: suitable geographic measurements for sparsity;

- whether it costs more to educate secondary students, and if so, the appropriate weight;

- how to account for Career and Technical Education in Act 73’s funding formula;

- how to account for differences in operating costs in different regions of the state; and

- how to fund special education, school construction, transportation, and PreK.

These contingencies would be in addition to the contingency already created by Act 73 that the expert tasked in Section 45a of Act 73 has provided its report to the General Assembly.

The fiscal impact of this section is unclear. JFO cannot estimate the overall impact of implementing these sections of Act 73, as there are several outstanding policy decisions.

Section 21: PreK and JFO Financing Considerations

Effective on July 1, 2026, Section 21 would mandate several reports on PreK education administration and costs:

- AOE, the Department for Children and Families (DCF), and Building Bright Futures (BBF) would establish a system to jointly monitor and evaluate prekindergarten education programs and collect data that will inform future decisions. Annually in January, BBF would report to the General Assembly on this system and data collection.

- On or before December 1, 2026, BBF would submit a report on the status of its work on its federal Preschool Development Grant, including information about student demographics and the number of hours offered by PreK programs by district. The report would also include data gaps, outstanding questions, and recommendations for legislative action. BBF would provide a progress report to Joint Fiscal Committee (JFC) on or before October 1, 2026.4

- JFO would contract to conduct an updated cost of care analysis for the provision of PreK education within Vermont’s education system. The contractor would reference previous cost of care analyses and collaborate with AOE, DCF, and BBF to ensure necessary data and appropriate factors are included in financial modeling. It would provide estimates for the current full cost of providing PreK education.

In addition to these reports, this section would also require JFO to provide the General Assembly with a report on the considerations associated with different funding mechanisms that may be used to distribute funds for education costs within the new financing formula.

This section would appropriate $75,000 from the General Fund to JFO in fiscal year 2027 to hire a contractor to provide this cost of care analysis.

Section 22: Data Collection

Effective July 1, 2026, Section 26 would require each student who receives tuition for public education to complete forms used to collect information on all weighting categories.

JFO cannot estimate the impact of this section. If this results in additional weighting data being captured by school districts, then this could result in an increase in the overall weighted student count which would shift tax capacity under current law and increase funding levels under the foundation formula.

Section 23: Special Education Funding

Effective July 1, 2026, Section 23 would prohibit school districts from reducing staff, programs, or funding which would disproportionately affect students with disabilities. It would require AOE to issue guidance for districts on implementing Act 73 while complying with this section and federal requirements. Districts would be required to follow this guidance and document how significant program changes would affect students with disabilities.

The fiscal impact of this section is unclear. If future special education funding systems do not provide sufficient funding, school districts would be unable to significantly reduce special education services. This could require a district, all else equal, to reduce services for non-special education students; alternatively, a district would need to find additional funding sources to maintain special education services.

Section 24: Tuition Fee Prohibition

Effective July 1, 2030 and assuming all contingencies are met, Section 24 would prohibit any school that receives tuition from a sending school district from requiring any other tuition or fees from a tuitioned student.

The fiscal impact of this section is unclear. If a receiving school or school district decides to increase its tuition in the absence of the ability to charge fees or additional tuition, this section could result in an increase in tuition payments, and thus education costs.

Section 25: Study Committee Budget Approval

Effective July 1, 2026, Section 25 would increase the threshold of a union district study committee’s budget before voter approval is needed. Under current law, if the committee budget exceeded $50,000 it must be approved by the member districts’ voters. Under this section, the threshold to trigger a vote would be raised to $500,000.

The fiscal impact of this section is unknown. If every study committee created budgets up to the new threshold, this would result in approximately $9.5 million in additional spending. As budgets would ultimately flow from the Education fund, any increase in spending from this section would require an adjustment to the homestead and/or nonhomestead property tax rates. JFO cannot predict how study committees would respond to this change.

Section 26: Small and Sparse School Rulemaking

Effective July 1, 2026, Section 26 would require the SBE to update its rules for Education Quality Standards to define criteria for schools to be considered “small by necessity” or “sparse by necessity”. Rules would need to be consistent with prior recommendations made by the SBE and would be required by March 31, 2027.

The fiscal impact of this section is unknown. Defining “small by necessity” and “sparse by necessity” would impact how many school districts receive school support grants under Act 73. JFO cannot determine the impact until rulemaking is complete.

Sections 27-27d: Agency of Education and State Board Rulemaking

Under these sections, AOE and the SBE would be charged with initiating education policy rulemaking.

Effective July 1, 2026, Section 27 would require AOE to update the District Quality Standards (DQS) to include guidance on how resources are budgeted within a district. This would be due by March 31, 2027.

Effective on passage, Section 27a would require AOE, in consultation with stakeholders, to update DQS with recommended reserve fund standards. These standards would include minimum and maximum reserve balances, acceptable uses of reserves, and best practices for replenishing them. These would be due by March 31, 2027.

Effective July 1, 2026, Section 27b would require AOE to submit a report on statewide school-transportation and financing. This report would be due by December 31, 2026.

Effective on passage, Section 27c would require AOE, in consultation with school business officials, to develop a statewide student profile form. This would be used by districts to collect student weighting information for students grades PreK-12 whom the State pays tuition for. This form would be due by September 1, 2026.

Effective July 1, 2026, Section 27d would require the SBE to update its rules for the length of a school day for each grade.

JFO cannot determine the fiscal impact of these sections. Any potential impacts would depend on the revised rules and how they would be implemented. Under Section 27c, all else equal, districts’ long-term weighted membership could increase. If this form resulted in additional weighting data being captured by school districts, then this could result in an increase in the overall weighted student count, which would shift tax capacity under current law and increase funding levels under the foundation formula.

Section 28-29: Small Schools and Sparse Schools

Section 28 would repeal the small school and sparse school language Act 73 (2025), Sec. 37 and reintroduce the language with clarifying changes under this bill’s Section 29. Section 29 would also charge AOE with annually determining if a school meets the criteria of “small by necessity” and/or “sparse by necessity”. Determinations would be made using the SBE’s rules on small or sparse by necessity.

JFO cannot estimate the fiscal impact of these sections. The fiscal impact would depend on the rules developed by the SBE and how they are implemented by AOE.

Section 29a: Definitions

Section 29a. would establish definitions for a number of terms used in Title 16. There is no fiscal impact of this section.

Sections 30 – 57: Regional Assessment Districts

Sections 30 – 57 would establish regional assessment districts and associated provisions. The following outlines significant sections of the bill related to regional assessment districts that may have fiscal implications.

Ultimately, the overall fiscal impact for establishing regional assessment districts cannot be estimated. If the changes increase the frequency of reappraisals, additional costs may occur. If they increase efficiency of reappraisals, there may be savings. Further, Section 35 would establish that the State would provide a payment for full reappraisals. The annual fiscal impact of this section would depend on the estimated full cost of reappraisals and the timing of reappraisals.

Unless noted otherwise, the sections focused on regional assessment districts would take effect on January 1, 2031.

Section 30: Establishment of Regional Assessment Districts

Section 30 would establish guidelines and requirements regarding regional assessment districts. Member municipalities of a regional assessment district would be required to fully reappraise their grand list every six years. This section would also require the Director of Property Valuation and Review (PVR) to establish standard guidelines and procedures for regional assessment districts and a reappraisal schedule for each regional assessment district. This section would also establish a valuation appeals process. Finally, it would create regional assessment district appeals boards to hear appeals for valuations within its district as the first step of a grievance process.

Section 32: Grand List Equalization Process

Section 32 would clarify that all municipalities within a regional assessment district would be treated as a single entity for the grand list equalization process.

Section 35: State Payment for Full Reappraisals

Effective July 1, 2026, Section 35 would establish a State payment for full reappraisals. When a municipality is scheduled to reappraise, the municipality may notify the Commissioner of Taxes that it is prepared to commence reappraisal. Within 30 days, the Commissioner will estimate the full cost of the reappraisal and transfer to the municipality the lesser of two-thirds of the estimated cost or $66 per grand list parcel.

This section would result in an increased cost to the State, however the scale and scope of these costs in a single year is unclear. There would be no payments under this provision until the year after regional assessment districts begin. For context, in fiscal year 2027, there were a total of 340,280 parcels in the State that could be eligible for this payment. The cost to reappraise all of these parcels would result in a maximum cost of approximately $22.5 million, which would not be incurred until regional assessment districts are in place, and the cost will likely be spread over the first six years and into the future.

Section 53: Transition to Regional Assessment Districts

Section 53 would limit timing for new municipal reappraisal orders and would require the Commissioner of Taxes to submit a report annually through 2031 on the progress of implementing regional assessment districts.

Section 54: Proposed Boundaries

Section 54 would require the Commissioner of Taxes to submit proposed geographic boundaries for regional assessment districts.

This section would be effective December 15, 2029, contingent on school districts having have had an opportunity to study the advisability of forming a union district.5

Section 55: Abated Education Tax From Error

Section 55 would allow the Commissioner of Taxes to reimburse a municipality for abated education tax if there was a clear or obvious error of the listers, and if the municipality abated municipal tax in the same proportion. This is estimated to have a de minimis impact to the Education Fund.

Section 58 - 64: Property Tax Classifications

Sections 58 – 64 would establish property tax classifications and associated provisions. The following outlines significant sections of the bill related to property tax classifications that may have fiscal implications.

The overall fiscal impact of these sections is unclear and will depend on outstanding policy choices, including tax rate multipliers.

The implementation of the tax classifications would take effect on July 1, 2030, if all contingencies in Section 18 have been met and if tax rate multipliers have been set as discussed in Section 63.

Section 58: Establishing Property Classes

Section 58 would establish three property tax classes: homestead, nonhomestead nonresidential, and nonhomestead residential. This section would also establish the definitions for these classes, as well as other definitions to be used for property classification.

This section would also establish a dwelling use attestation which would be used to describe how a dwelling unit will be used in the current year for purposes of assigning a tax classification. This section would establish that properties with a dwelling unit that has no homestead declaration or dwelling use attestation would be assigned the tax classification with the highest statewide education tax rate multiplier.

Section 59: Errors or Omissions in Filed Dwelling Use Attestation

Section 59 includes provisions relating to instances where the Commissioner determines that a filed dwelling use attestation contains errors or omissions. If the Commissioner determines the error was not made with fraudulent intent, the municipality would be permitted to include a penalty of up to 5% of the education tax on the property. If the Commissioner determines the error was made with fraudulent intent, the Commissioner would impose a penalty equal to 100% of the education property tax and any interest of late payment that was due.

Section 60: Collection of Property Classification Data

Section 60 would establish the collection of property tax classification data for calendar year 2029 and would require that data to be submitted to JFO by October 1, 2029.

Section 63: Prospective Repeal

Section 63 would create a prospective repeal. If new tax rate multipliers to be used in a tax classification system are not established by July 1, 2030, then this section would repeal the sections establishing the property classification.

Sections 65 - 78: School Construction

Sections 65 – 78 would amend the State Aid for School Construction Program to expand State aid to include general obligation bonding. The following outlines significant sections of the bill related to school construction that may have fiscal implications.

The overall fiscal impact of these sections is unclear and will depend on outstanding policy and funding decisions. Any future impacts to the State’s general obligation debt service costs would be directly related to any increase in bonded indebtedness and market conditions at the time of the debt issuance. Additionally, any material increase in general obligation debt service would, per statute, impact the calculation of the General Fund transfer to the Cash Fund for Capital and Essential Investments.

Per 32 V.S.A. § 1001b(b)(1)(A), the General Fund transfer to the Cash Fund is calculated at 4% or less of the last completed fiscal year’s General Fund appropriations, less the amount necessary to fund the State’s general obligation debt service in the year for which the transfer is being made. When all else is equal, an increase in general obligation debt service, due to increased bonding for things such as school construction, would reduce the amount available to transfer to the Cash Fund.

Unless noted otherwise, the sections on school construction would take effect on July 1, 2026.

Section 66: AOE School Construction Division

Section 66 would establish four permanent, classified positions in AOE, which would then be required to include funding for the positions in its fiscal year 2028 budget request. The fiscal impact of this section will depend on the costs associated with these positions and associated funding decisions.

Section 67: Rules on School Construction and Capital Outlay

Section 67 would require AOE to adopt rules on school construction and capital outlay by March 31, 2027. Rules would have to address prioritization and bonus incentives that support the construction or renovation of school facilities that support the consolidation of school governance structures and improve access to educational opportunities for public school students as well as the treatment of school districts’ outstanding capital indebtedness as of December 31, 2025.

Section 68: Report on School Construction Opportunities

Section 68 would require the State Aid for School Construction Advisory Board to submit a report to the General Assembly identifying opportunities for school construction by December 1, 2026. The report would be required to identify opportunities, provide a full siting study for each opportunity including cost and location, and evaluate different statewide scenarios for pursuing multiple opportunities for consolidation.

Section 70: State Bonding in Budget Request

Section 70 would require AOE to include in its annual budget submitted to the Governor any projects contemplated for funding through State bonding.

Section 72: School Construction Projects, Debt Service Subsidy and State Bonding

Section 72 would amend the approval and funding of school construction projects. This section would require AOE to identify projects for funding through general obligation bonding in its request for appropriations. It would also require the House Committees on Education and on Ways and Means and the Senate Committees on Education and on Finance to recommend a total annual school construction appropriation for inclusion in an aggregate education payment.

This section would amend the award provisions of the Program to provide aid of 50-95% of the total approved cost of a project in the form of a debt service subsidy, State bonding, or a combination of both. It would remove the requirement for bond authorization before prioritization and final approval so that a school district’s bond authorization reflects the amount of State aid it will receive. The amounts would be awarded annually, be subject to annual appropriation, and only be released once the applicant has voted to fund or authorized a bond for the total estimated cost of the project.

Section 72 would also require the Treasurer, in consultation with the Capital Debt Affordability Advisory Committee (CDAAC), to recommend the annual total State bonding support available and the annual debt subsidies to be awarded.

Section 73: Repeal Prohibition on Aid Resulting from Deferred Maintenance

Section 73 would repeal the prohibition on State aid for school construction projects where “the need for the project or construction has arisen in whole or in part from significant deferred maintenance” under 16 V.S.A. § 3454. While repealing this prohibition would expand aid to a broader pool of projects, JFO cannot estimate the fiscal impact of this section.

Section 74: Legacy Debt Aid Program

Section 74 would establish a legacy debt aid program for school districts that incurred debt for costs related to facility construction and renovation on or before December 31, 2025. Districts would be eligible to receive aid equal to 100% of the debt service cost on this indebtedness. The maximum total annual amount of aid would be $61 million. Legacy debt aid would be subject to an annual appropriation, and it is unclear from which fund. Assuming the legacy debt aid is awarded, this would have a fiscal impact to whichever fund from which the appropriation is made.

Under current law, all school district debt service costs are included in a district’s education spending and thus the annual Education Payment appropriation from the Education Fund. If the appropriation for these costs was instead made directly from the Education Fund, this would not increase costs to the Education Fund but would shift property tax burden, so all property taxpayers are equally covering the cost of legacy debt regardless of where the property is located.

Sections 75 and 76: Education Payment

Sections 75 and 76 would require the General Assembly to appropriate funds for an Education Payment that includes the amount obligated to provide for school construction.

Sections 77 and 78: Supplemental District Spending and School Construction

Effective July 1, 2030 assuming all contingencies are met, Section 77 would exempt all school construction expenditures from the cap on supplemental district spending. The school board of a district would be required to submit for authorization supplemental district spending to cover debt service costs for school construction only at the initial authorization of indebtedness.

The fiscal impact of this section is unclear as it will depend on district decisions. However, it is likely this section would result in increased supplemental district spending because it would expand the total amount of supplemental district spending that would be permitted.

Sections 79 – 83: Foundation Formula Transitions

Sections 79 -83 would amend the foundation formula transition mechanisms in Act 73 to align with the effective dates that would be established by this bill.

Because these transition mechanisms were already established by Act 73, and this section would only amend the dates, there is no estimated fiscal impact of these sections.

1 The Joint Fiscal Office (JFO) is a nonpartisan legislative office dedicated to producing unbiased fiscal analysis – this fiscal note is meant to provide information for legislative consideration, not to provide policy recommendations. ,

2 The link to H.955 as introduced is available here: https://legislature.vermont.gov/Documents/2026/Docs/BILLS/H-0955/H-0955%20As%20Introduced.pdf

- A Board of Cooperative Education Services is outlined in 16 V.S.A. Chapter 10 as a mechanism for supervisory unions to provide shared programs and services on a regional and statewide level.

- More information on the $12.7 million Preschool Development Grant from the U.S. Department of Health and Human Services can be found here. Overall, the grant contains three goals: reconcile fragmented elements (including PreK) into a unified system; expand childcare program availability, quality, and viability; and align and share information and data systems.

- The full contingency is included in Section 18 of this bill, which amends 2025 Acts and Resolves No. 73, Sec. 70(f)(1)(A).

To support vital journalism, access our archives and get unique features like our award-winning profiles, Book of Lists & Business-to-Business Directory, subscribe HERE!

Vermont Business Magazine

Vermont Business Magazine