Program Weaknesses Increased Risk that Large Sums Would Be Provided to Entities That Needed Less or Didn’t Need State Assistance at All

by Timothy McQuiston, Vermont Business Magazine State Auditor Doug Hoffer released an audit today of the Department of Economic Development’s implementation of two programs funded with $50 million of federal COVID money – the Capital Investment Program and the Community Recovery and Revitalization Program. The two programs were created to address the negative economic impacts of the pandemic while leveraging opportunities to grow Vermont’s economy. The programs were chosen for audit because the Department’s administration of an earlier COVID business grant program had internal control problems, raising the risk that taxpayer funds would be misspent.

The Legislature allocated $50,580,000 of this funding across these two new grant programs and authorized the DED to design them. Under CIP, grant awards were limited to the lesser of $1.5 million or the estimated net State fiscal impact (NFI) of the project which was to be calculated by the Legislature’s and Administration’s economists. At the request of DED, this guardrail required by law was removed for CRRP. As a result, there was no analysis of the economic or fiscal impact of individual CRRP projects.

“It can be tempting to say that any dollar used to ‘grow the economy’ is a dollar well spent. Obviously, that can’t be true if the recipient of the money didn’t need it, or if they got more than they needed,” said Hoffer. “And every dollar that was misspent was one dollar not available for clear-cut public needs like flood resiliency, affordable housing, and school infrastructure. Unquestionably some of the grants went to worthy projects. Nonetheless, our audit once again finds holes in the Department’s program management that are worrying.”

Hoffer added: “I also want to remind Vermonters of something that’s unique about the work my staff does. The professional auditing standards governing the work of the auditors who produce audits like this one require that all of our findings and conclusions be backed up by evidence that is documented. Responses from the departments we audit, on the other hand, do not need to be supported by facts, and can include opinions, political positions, and statements that are misleading or inaccurate. The facts our auditors present are not disputable. What to do with those facts is a different question, and one about which reasonable people may disagree. The Department owes it to taxpayers to address the facts we’ve presented – it is, after all, their money that was being spent.”

DED Commissioner Joan Goldstein took issue with many of the findings in audit, including that the rules the department had to follow were federal because it was federal funds that were being dispersed.

"DED would like to say for the record that thorough due diligence was applied to our processes and decision making was informed by input from relevant stakeholders, including subject matter experts," Goldstein wrote as part of her response. "Additionally, DED documented the rationale for award amounts to ensure transparency and fully complied with state law in all its actions and decisions.

"The SAO performance analysis focuses on compliance with state statutes while disregarding that the program funding was provided under federal guidelines that control the use of the funds and the associated compliance requirements. Doing so led the SAO to assert that DED failed to follow the rules. We categorically deny this. Further, the SAO emphatically complained to the Vermont Legislature about DED's interpretation of the US Treasury directive for CIP implementation. The SAO then issued a technical inquiry to the US Treasury, which subsequently confirmed that DED's methodology was aligned with ARPA rules.

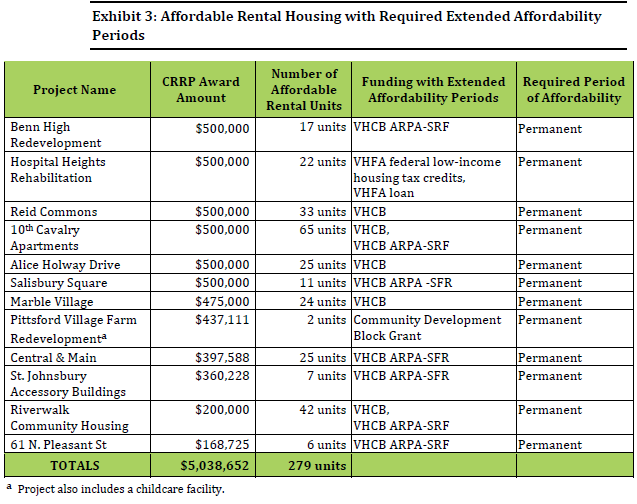

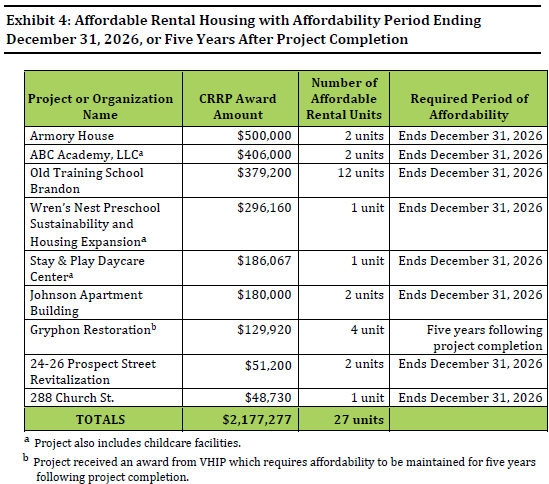

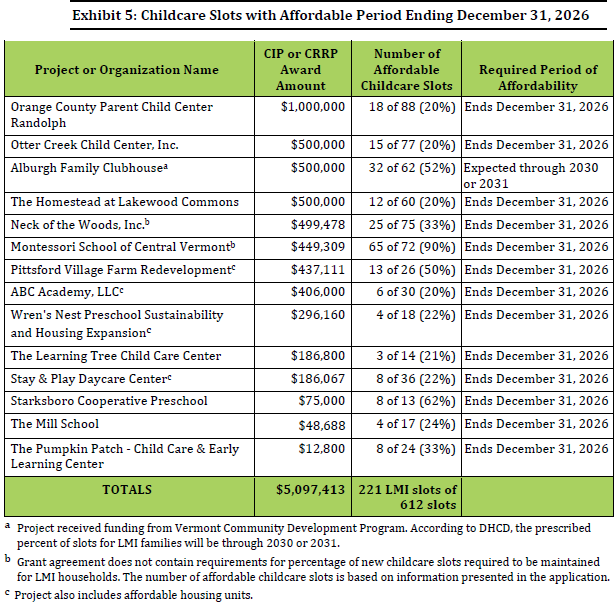

"The SAO raises a valid point regarding the affordable housing grants. The SAO recommends an affordability extension beyond our current grant closeout date of 12/31/2026. Because such an extension would be after the closeout date, DED will endeavor to find a solution for how this could be achieved legally and administratively."

Key findings of the audit include (See associated Exhibits at bottom with CIP awardees, projects and dollar amounts at bottom. Complete list HERE):

• The Department made little effort to validate applicants’ claims that they needed grant funds, even though Vermont law requires applicants to demonstrate “that grant funding is needed to complete the project.”

• Three grant recipients indicated that their projects would proceed in the absence of CIP or CRRP funding, but they received grant funds anyway.

• The Department made no distinction between applicants who had substantial cash-on-hand with which to proceed with their projects, and those who had no reserves at all. While not all reserves could or should be drawn down to fund a capital project, the Department’s complete dismissal of an applicant’s self-financing capacity risked providing taxpayer funds to applicants who didn’t need it or needed less of it. In one instance, an awardee had cash on hand that was 27 times the total cost of the project.

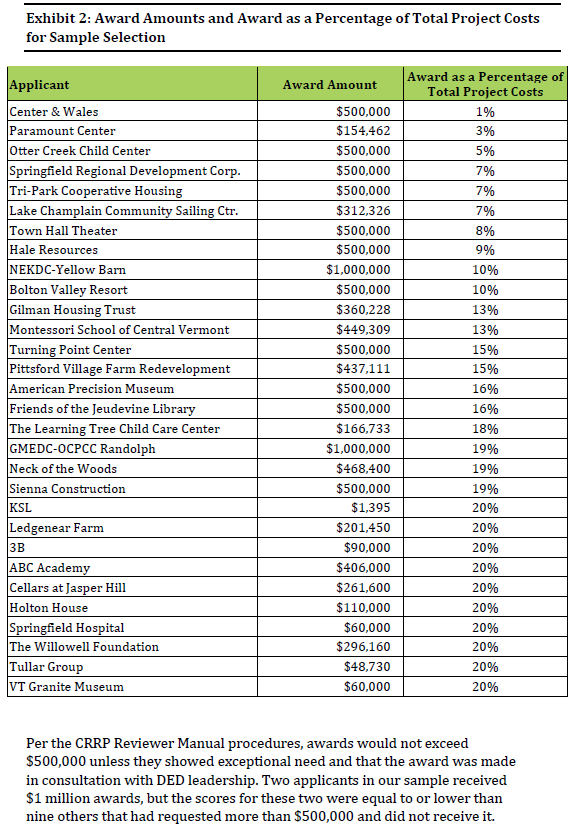

• A lack of documentary evidence makes it impossible to know why some CRRP applicants received funding while others did not, or why they received the amounts they received. When state officials do not adequately document their decisions, they can’t be transparent with the public or demonstrate whether decisions were equitable and based on the requirements in law.

• When designing the CRRP, the Department successfully advocated for the removal of a CIP requirement that grants not exceed the expected financial benefit a project would deliver to the state. As a result, some grants likely exceeded their value to the Vermont economy.

• Because the Department did not incorporate any affordability requirements into their grant agreements, some housing and childcare projects that received funding will not be required to maintain any affordability past the end of the grant agreement on December 31, 2026.

“There’s risk involved whenever the government distributes taxpayer funds to private entities. That’s why it’s so important for state officials to include tight guardrails with such programs. Unfortunately, that’s not what we saw in this audit,” Hoffer added.

The Department seemed to have particular challenges administering the CIP and CRRP both because of the evolving rules established by the U.S. Treasury and because of the nature of the projects themselves. Rather than deploy these precious one-time federal funds to support well-established programs with clear guidelines, the Legislature acceded to the Department’s request to create a new program (CRRP), effectively giving them authority to make substantial funding decisions with few constraints.

As they rushed to spend the funds by the federal deadlines, the Department didn’t apply the type of rigorous review required by most longtime state economic development and housing funding programs.

Hoffer added: “My team of professional auditors made a series of recommendations to the Department to tighten up their administration of grant funds in the future. While we are discouraged that Department leadership indicated that their shortcomings can be excused because of the dynamic nature of large capital projects, we are hopeful that the Legislature will be more prescriptive in the future to require the Department to adopt greater taxpayer protections.”

On September 23, 2024, the Commissioner of the Department of Economic Development provided an amended version of written comments on a draft of this report. The Commissioner disagreed with many of our findings but acknowledged that we made a valid point regarding affordable housing grants and would seek a solution for extending the affordability period. These comments are reprinted in Appendix VI. SAO evaluation of these comments is in Appendix VII.

NOTE: The SAO PDF did not include live links in Goldstein's letter below. Here are the relevant links:

Community Recovery and Revitalization Program

SAO memo from March 2022 to Vermont Legislature

SAO attachment to memo from March 2022

Agency of Administration memo dated August 2024

CIP Awards

This report with responses to Commissioner Goldstein's statement is also available online here.

Source: 9.30.2024. MONTPELIER, VT – State Auditor

To support vital journalism, access our archives and get unique features like our award-winning profiles, Book of Lists & Business-to-Business Directory, subscribe HERE!