Vermont Business Magazine This week marked a crucial milestone for Vermont’s public education system as the House passed the annual yield bill, H.887, which aims to provide relief to property taxpayers and sets a clear path forward for education finance and taxation. It passed out of the House Wednesday on a vote of 101- 39, which, as is, would be sufficient to override a gubernatorial veto if it were to come to that. Governor Phil Scott has frequently made the point that Vermonters are already overtaxed, and this plan would raise property taxes by an average of 15%. The bill is now in the Senate Finance Committee for review (see Joint Fiscal Office bill description below).

The JFO estimates that the yields and rates in this bill will correspond with an average increase of approximately 14.97% for homestead property tax bills and income education tax bills, and an average increase of 17.99% for nonhomestead property tax bills. Governor Scott suggested at his weekly press conference Wednesday that the Senate could temper the impact of the House-passed bill. See his comments below.

"Balancing the needs of our children and the needs of taxpayers is a shared responsibility between districts, the administration, and the legislature," remarked Rep. Emilie Kornheiser, Chair of the House Ways and Means Committee. "There is no perfect next step, but it’s an important and necessary step in ensuring that our schools are funded, our obligations are met, and we are on a path to continue Vermont’s commitment to an equitable education system."

"This bill reflects our belief that we must transform our public school system in Vermont into one that is the right size, sustainable and supports excellence in student achievement at a price Vermonters can afford," stated Rep. Peter Conlon, Chair of the House Education Committee. "We need a shared vision for our public education system. If we have clear goals for a Vermont public education system, we will make the necessary hard decisions together and for each other."

H.887 (An act relating to homestead property tax yields, nonhomestead rates, and policy changes to education finance and taxation) is a comprehensive piece of legislation that addresses the issues faced by Vermont's education system. Among its key provisions:

- Property Tax Relief: Lowers anticipated homestead property tax rates by 5%, repeals the exemption to sales tax for cloud based services, and a modest increase (1.5% added to the meals and rooms tax) on short-term rental purchases.

- Stabilization of the Education Fund: Recognizing the need for long-term stability, H.887 includes measures to stabilize the education fund across multiple years. This includes the reinstatement of the excess spending threshold at 120%, with adjustments to ensure fairness for all districts.

- Creation of the Commission on the Future of Public Education: This commission will study the provision of education in Vermont and make recommendations for a statewide vision for the public education system. Its goal is to ensure that all students are afforded substantially equal educational opportunities in an efficient, sustainable, and equitable education system.

“This bill provides some immediate relief to taxpayers and lays the groundwork for a sustainable, equitable, and enriching public education system for all Vermont children,” said House Speaker Jill Krowinski. “As we move forward, it is imperative that we continue to work together to shape the future of education in Vermont. Vermonters, and our children, are counting on us to deliver meaningful change.”

Governor Scott had a different view and enunciated it at this Wednesday press conference:

"When it comes to the yield bill being considered today in the House and the huge property tax increase it will bring, I don't believe it is something most Vermonters can accept. And from what I've heard, I don't think the Senate will either. Vermonters simply cannot afford a historic double digit increase in their property taxes or a substantial hike in their rents, which will also be impacted because landlords will have no choice but to pass those increases on to renters. (Voters are) making that clear at the polls, and I hope they're making it clear to their representatives in Montpelier. This is especially true after a 20% hike in DMV fees, a new payroll tax coming July 1, inflation, and the hike in home heating costs we know is coming as a result of the Clean Heat Standard they passed and I vetoed last year and they overrode. Vermonters are clear. They've had enough. As a yield bill moves out of the House into the Senate, I'm hoping the Senate will work with us to prevent this enormous tax increase from happening this year and making sure we're not in the same exact situation next year and in the years to come."

Joint Fiscal Office

April 18, 2024

Bill Summary

This bill sets the property dollar and income dollar equivalent yields for the purpose of setting homestead tax rates. It also sets the nonhomestead property tax rate. The bill expands revenues to the Education Fund by repealing the sales tax exemption for prewritten software accessed remotely. It also imposes a 1.5% surcharge on short-term rentals, with all revenues dedicated to the Education Fund. The bill establishes several working groups and commissions, including the “Commission on the Future of Public Education in Vermont,” the “Educational Opportunity Payment Task Force,” and the “Education Fund Advisory Committee.”

Fiscal Impact

The Joint Fiscal Office (JFO) cannot estimate the overall impact of the bill on the Education Fund in future fiscal years. The following sections may have a fiscal impact on the Education Fund:

• Section 2 sets the property dollar equivalent yield, income dollar equivalent yield, and nonhomestead property tax rate for fiscal year 2025. JFO estimates that these yields and rates would correspond to an average increase of approximately 14.97% for homestead property tax bills and income education tax bills, and an average increase of 17.99% for nonhomestead property tax bills. The section also includes a one-time increase of 14.97% to each claimant’s property tax credit for fiscal year 2025.

• Sections 3 and 4 repeal the sales tax exemption for prewritten software accessed remotely. JFO estimates this change would generate $20.4 million in additional revenue for the Education Fund in fiscal year 2025.

• Section 5 imposes a 1.5% surcharge on short-term rentals and dedicates the revenue to the Education Fund. JFO estimates this surcharge would generate $6.5 million for the Education Fund in fiscal year 2025.

• Sections 10 and 11 repeal the suspension of the school budget ballot language requirement and amend the language. JFO can neither estimate the impact of this on voter behavior nor the corresponding fiscal impact.

• Section 11 creates an “Education Fund Advisory Committee” to monitor Vermont’s education

finance system, conduct analyses, and make recommendations for the Education Fund.

• Sections 13 through 17 adjust calculations regarding the application of the local common level of appraisal (CLA). JFO estimates this will have no impact on property tax rates after the application of the CLA, so long as a district’s per pupil spending is greater than the property yield. JFO cannot estimate if this section will impact voter decisions or district budgeting.

• Section 18 establishes an excess spending threshold for per pupil education spending in fiscal years 2026 and 2027 to be included in tax rate calculations. JFO cannot estimate the fiscal impact of this section on the Education Fund because total education spending is ultimately determined by local votes.

The bill also expands the use for a fiscal year 2024 General Fund appropriation and includes intent language for the appropriation of $125,000 from the General Fund to the Agency of Education (AOE) in fiscal year 2025.

• Section 1 establishes the “Commission on the Future of Public Education in Vermont. To fund the costs associated with the Commission, the bill expands the allowable uses of a $200,000 General Fund appropriation to the Agency of Education in fiscal year 2024.

• Section 8 states that, to the extent possible, $125,000 would be appropriated from the General Fund to AOE in fiscal year 2025 for a new education finance data analyst position.

Background and Details

Section 1: The Commission on the Future of Public Education in Vermont Section 1 creates a “Commission on the Future of Public Education in Vermont” to study and make recommendations for a statewide vision for Vermont’s public education system. The Commission will be comprised of 23 members. Members of the Commission not employed by the State are entitled to per diem compensation and reimbursement of expenses under 32 V.S.A § 1010 for a maximum of 30 meetings. The Commission will cease to exist on December 31, 2025. It shall have the support of AOE, which is charged with contracting with an independent consultant to provide technical and legal assistance to the Commission. To fund costs associated with Commission, the bill expands the allowable uses of a $200,000 General Fund appropriation to the Agency of Education in fiscal year 2024. Additional appropriations may be required in fiscal year 2026 to continue to support the work of the commission.

Section 2: Yields, Property Tax Rates, and Property Tax Credits for Fiscal Year 2025 Section 2 sets the property dollar equivalent yield at $9,846, income dollar equivalent yield at $10,060, and the nonhomestead property tax rate at $1.442 for fiscal year 2025. JFO estimates that these yields and rates will correspond with an average increase of approximately 14.97% for homestead property tax bills and income education tax bills, and an average increase of 17.99% for nonhomestead property tax bills. These yields and rates are set at a level estimated to be sufficient to fully fund the Education Fund. This section also includes a one-time increase of 14.97% to each claimant’s property tax credit for bills issued for fiscal year 2025. JFO estimates this will cost the Education Fund $23.7 million in fiscal year 2025.

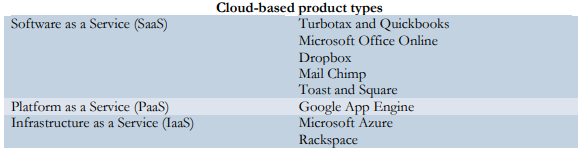

Sections 3 and 4: Sales and Use Tax on Prewritten Computer Software Accessed Remotely Under current law the retail sale of tangible personal property, including prewritten software, is subject to the sales and use tax. However, Act 51 (2015) created an exemption for prewritten software accessed remotely. This exemption currently applies to three types of cloud-based services: Software as a Service (SaaS); Platform as a Service (PaaS); and Infrastructure as a Service (IaaS). Examples are provided below.

Sections 3 and 4 would repeal the exemption and subject sales of these programs to the 6% Vermont sales and use tax. The repeal of the exemption would not apply to custom software or IT services. JFO estimates this would generate $20.4 million in additional revenue in fiscal year 2025 and $22.3 million annualized, beginning in fiscal year 2026. Revenue may increase year over year due to the strong projected growth in the cloud-based services market.

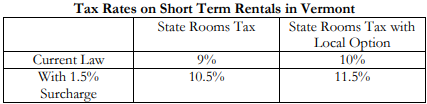

Section 5: Short-Term Rental Surcharge Section 5 imposes a 1.5% surcharge on short-term rentals, which are defined as a “furnished house, condominium, or other dwelling room or self-contained dwelling unit rented to the transient, traveling, or vacationing public for a period of fewer than 30 consecutive days and for more than 14 days per calendar year.” This includes both entire units and single rooms if the rental is for less than 30 consecutive days. Currently, these rentals are subject to the 9% rooms tax (10% in towns with a local option tax), which is allocated to the General Fund (69%), Education Fund (25%), and the Clean Water Fund (6%). 2 The rooms tax allocation would remain the same but the entirety of the surcharge would go to the Education Fund.

AirDNA data from the Vermont Housing Finance Agency (VHFA) website, which aggregates information from major booking platforms like AirBNB and VRBO, showed that during fiscal year 2023 the monthly number of entire units available as short-term rentals ranged between 9,378 and 10,358. Average monthly revenue was approximately $4,000. In the same period, 1,400 rooms were available and had an average monthly revenue of approximately 25% of that for entire units. JFO estimates that 1.5% of overall revenue from these rentals will generate $6.5 million for the Education Fund in fiscal year 2025 and $7.4 million annualized, beginning in fiscal year 2026. An important consideration is the extent to which the surcharge leads to fewer bookings due to price increases or changes in the dynamic pricing model used by major platforms to account for changes in demand. However, a surcharge of 1.5% is quite low and therefore unlikely to substantially change behavior in many cases. For example, on a $700 rental, the surcharge would be $10.50.

Section 6: Technical Clarifications to Education Fund Statute Section 6 puts all revenue sources to the Education Fund in the same place in statute. It does not change revenue sources to the Education Fund.

Section 7: District Quality Standards for Maximum Reserve Fund Accounts Section 7 requires AOE to undertake rulemaking to update District Quality Standards rules to include recommended reserve fund account standards. Any fiscal impact of this section would depend on the rules established.

Section 8: Creation and Funding of One Position of Education Finance Data Analyst Section 8 establishes a new permanent classified education finance data analyst position at AOE. Section 8 states that, to the extent possible, $125,000 would be appropriated from the General Fund to AOE in fiscal year 2025 for a new education finance data analyst position.

Section 9 and 10: School Budget Ballot Language Sections 9 and 10 amend the school budget ballot language requirement and repeal its suspension. JFO can neither estimate the impact of the ballot language on voter behavior nor its corresponding fiscal impact.

Section 11 and 12: Education Fund Advisory Committee Section 11 creates an “Education Fund Advisory Committee” to monitor Vermont’s education finance system, conduct analyses, and make recommendations on multiple considerations of Vermont’s Education Fund. The Committee is composed of 12 members. Members not employed by the State are entitled to per diem compensation and reimbursement of expenses under 32 V.S.A § 1010 for a maximum of four meetings per year. The Committee will cease to exist on July 1, 2034. It will have the support of the Department of Taxes and AOE.

Section 13 – Section 17: Common Level of Appraisal Sections 13 through 17 adjust calculations regarding the application of the local common level of appraisal (CLA). These changes will have a de minimis impact on the revenue raised by districts and will solely reduce the difference between the tax rates pre- and post- application of the CLA. JFO estimates this will have no impact on property tax rates after the application of the CLA, so long as a district’s per pupil spending is greater than the property yield. JFO cannot estimate if this section will impact voter decisions or district budgeting.

Section 18 – Section 20: Excess Education Spending The excess spending threshold is a provision that adjusts tax rates so that districts spending above it are taxed a second time on the excess spending amount. Section 18 amends the excess spending threshold so that it is calculated as the statewide average per pupil spending in fiscal year 2025, increased for inflation, multiplied by 120%. This section repeals all exclusions in current law for the calculation of excess spending threshold. The section adds an exclusion for increases in voter-approved bond payments year over year. Districts with education spending above the threshold see a more significant increase in their local tax rate. However, JFO cannot estimate the fiscal impact of this section on the Education Fund because total education spending is ultimately determined by local votes. Act 127(2022) suspended the excess spending threshold through fiscal year 2029. Section 19 repeals that suspension and makes the threshold effective as of July 1, 2025, meaning that it will be used for the calculation of tax rates starting in fiscal year 2026.

Section 21: Report on Property Tax Credit Claims and Asset Declarations Section 21 requires that the Commissioner of Taxes recommend improvements for property tax credit claims, including the use of an asset declaration, in a report to the House Committee on Ways and Means and the Senate Committee on Finance on or before December 15, 2025. This section is not estimated to have a fiscal impact.

Sections 22 and Section 24: Act 127 Conforming Amendments Sections 22 through 24 amend statute to align it with Act 127 and will not have a fiscal impact.

1 The full text of the bill can be found at the following link:

https://legislature.vermont.gov/Documents/2024/Docs/BILLS/H-0887/H-0887%20As%20Introduced.pdf

2 In Burlington, short-term rentals also charge a 9% gross receipts tax.

For more information on H.887, please visit the legislative website.

Source: 4.26.2024. Montpelier, VT - Speaker of the House. Joint Fiscal Office.

To support great journalism, access our archives and get unique features like our award-winning profiles, Book of Lists & Business-to-Business Directory, subscribe HERE!