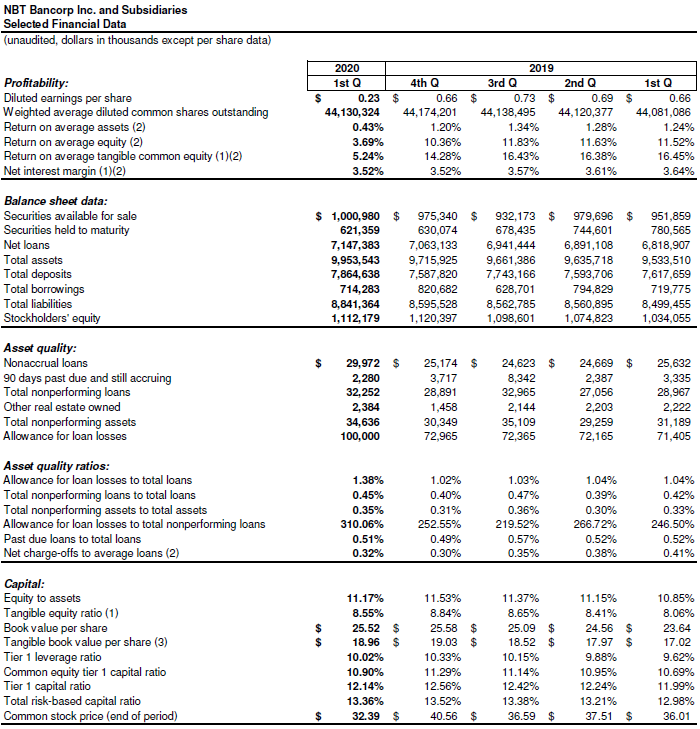

Vermont Business Magazine NBT Bancorp Inc (NASDAQ: NBTB) reported net income of $10.4 million, or $0.23 per diluted common share, for the three months ended March 31, 2020. NBT’s results in the first quarter of 2020 reflect the Current Expected Credit Losses accounting methodology, including the estimated impact of the COVID-19 pandemic on expected credit losses. Net income was down 64% from the previous quarter and from the first quarter of 2019 ($0.66) primarily due to higher provision for loan losses related to the deterioration of economic conditions caused by the COVID-19 pandemic.

Norwich, NY-based NBT Bank has branches in Northwest Vermont.

Pre-provision net revenue (“PPNR”)1, excluding securities gains (losses), for the first quarter was $42.5 million compared to $42.9 million from the previous quarter and $43.0 million in the first quarter of 2019.

CEO Comments

“In the face of the rapidly changing economic conditions brought on by the COVID-19 pandemic, we have been aggressive in our response to deliver support and solutions to our customers in distress while providing for the health and safety of our employees,” said John H. Watt, Jr. “We are extremely proud of our team members who have been able to process high volumes of loans through the SBA’s Paycheck Protection Program that are helping businesses in the communities we serve to retain tens of thousands of workers.”

Watt continued, “Our earnings for the first quarter were significantly impacted by the COVID-19 pandemic and the resulting increase to our provision for expected losses under CECL accounting. The quarter was marked by strong loan growth and consistent underlying operating financial performance even in the face of a 150-basis-point drop in the federal funds rate. Our strong balance sheet and capital position, disciplined approach to credit and risk management, technology investments and diversified fee business are attributes that provide NBT with resources and flexibility to navigate these difficult times. We moved forward to complete the acquisition of Alliance Benefit Group of Illinois, Inc. as planned on April 1, 2020 by our EPIC Retirement Plan Services business unit. Our experienced and seasoned management team and knowledgeable local bankers across 7 states will maintain focus on the fundamentals of our business while supporting our customers, communities and shareholders to ensure we all emerge from the current challenges stronger together.”

First Quarter Highlights

|

Net Income |

|

|

Net Interest Income / NIM |

|

|

PPNR |

|

|

Loans and Credit Quality |

|

|

Capital |

|

Company Response to Pandemic

The COVID-19 pandemic has significantly disrupted the global and local economy and the customers and communities served by NBT. In response, the Company immediately formed an Executive Task Force and engaged its established Incident Response Team to execute a comprehensive pandemic response plan. Actions taken to address the safety of employees and the needs of customers are highlighted below.

- Employees

- 90% of non-branch employees quickly deployed to work remotely.

- New scheduling protocols implemented to optimize social distancing for branch staff, including drive-up/ATM and appointment-only banking.

- Additional paid time off provided to address health and childcare needs.

- Cross-training and redeployment programs directing staff resources to areas of greatest need.

- Internal and external communication increased to address rapidly changing business environment and personal impact to employees.

- Customers

- 82% of branches remain open for drive-up service and remaining branch staff redeployed to assist in other areas.

- Leveraged technology tools such as robotic process automation for payment extension requests and onboarding loans; increased use of electronic signatures.

- Digital communication channels significantly enhanced with dedicated webpages and social media content.

- Increased use of self-service with a 60% increase in mobile deposits and over 50% increase in mobile and online banking enrollment.

- As of April 17, 2020, 11.6% of loans are in payment deferral programs:

- 74% are commercial and 26% are consumer borrowers.

- Over $385 million in Paycheck Protection Plan (“PPP”) loans processed through April 16; will actively participate in second PPP appropriation.

Loans

- Period-end total loans were $7.2 billion at March 31, 2020 compared to $7.1 billion at December 31, 2019.

- Commercial real estate increased $100.0 million to $2.2 billion; commercial and industrial loans increased $36.4 million to $1.3 billion; total consumer loans decreased $25.2 million to $3.7 billion.

- Commercial line of credit utilization rate of 32% at March 31, 2020 remained consistent with December 31, 2019 of 32% and compared to 36% at March 31, 2019.

Deposits

- Average total deposits in the first quarter of 2020 were $7.7 billion, compared to $7.6 billion in the fourth quarter 2019, with annualized growth of 3.8%.

- Seasonal inflow of municipal deposits resulted in increases of $37 million on a period-average basis and $182 million on a period-end basis.

Net Interest Income and Margin

- Net interest income for the first quarter was comparable to the fourth quarter of 2019 at $77.2 million and down slightly from the first quarter of 2019 of $77.7 million.

- The net interest margin on a fully taxable equivalent (“FTE”) basis of 3.52% was flat from the fourth quarter of 2019 and down 12 basis points (“bps”) from the first quarter of 2019.

- Earning asset yields were down 6 bps from the prior quarter and down 21 bps from the same quarter in the prior year. Earnings assets grew $124.2 million or 1.4% from the prior quarter.

- The cost of interest-bearing liabilities decreased 8 bps from the prior quarter to 0.82% at March 31, 2020 and compared to 0.92% for the first quarter of 2019.

- Cost of interest-bearing deposits decreased 8 bps from the prior quarter and were 61 bps for the month of March.

- Total cost of deposits was 48 bps for the first quarter of 2020, down 6 bps from the prior quarter and flat with the same period in the prior year.

Credit Quality and CECL

- Asset quality metrics remained stable in the first quarter of 2020.

- Net charge-offs to total average loans of 32 bps compared to 30 bps in the prior quarter and 41 bps in the first quarter of 2019.

- Nonperforming assets to total assets were 0.35% compared to 0.31% at December 31, 2019 and 0.33% at March 31, 2019, driven primarily by one commercial credit of $4.2 million.

- Provision expense increased $23.6 million from the fourth quarter of 2019 primarily due to an increase in expected losses resulting from deterioration of the economic forecast due to the COVID-19 pandemic.

- The allowance for loan losses was $100.0 million, or 1.38%, of total loans compared to 1.02% at December 31, 2019 and 1.07% Day 1 CECL (January 1, 2020).

- Day 1 CECL impact resulted in a $3.0 million increase to the allowance for loan losses and a $2.8 million increase to the unfunded loan commitment reserve; retained earnings decreased $4.3 million (after-tax) compared to year-end 2019.

Noninterest Income

- Total noninterest income, excluding securities gains (losses), was consistent with the prior quarter at $36.2 million and up $2.5 million from the prior year quarter.

- As compared to the prior quarter, seasonally higher insurance revenues and retirement plan fees in the first quarter of 2020 were offset by lower levels of swap fees.

- Increase from the prior year first quarter was driven by higher swap fees in other noninterest income and higher wealth management income partly reduced by lower insurance agency seasonal revenues.

- Securities losses of $0.8 million were driven by mark-to-market adjustments on equities securities.

Noninterest Expense

- Total noninterest expense for the first quarter was up 0.8% from the previous quarter and up 3.5% from the first quarter of 2019.

- Significant variances to the prior quarter:

- Salaries and benefits seasonally higher due to higher payroll taxes and stock-based compensation expenses ($1.5 million).

- Other noninterest expense was higher in the first quarter of 2020 due to a $2.0 million increase in reserves for unfunded loan commitments due primarily to CECL adoption and COVID-19 pandemic expected losses and was partly offset by $0.7 million lower pension costs.

- Significant variances to the first quarter of 2019:

- Higher salaries and benefits primarily due to merit increases, higher number of employees, one additional business day and higher medical costs.

- Other expenses increased $1.8 million due to an increase to the unfunded loan commitments reserve, partly offset by lower pension costs.

- Remaining portion of FDIC insurance assessment credit was used in the first quarter of 2020.

Income Taxes

- Effective tax rate was 14.2% for the first quarter of 2020 compared to 22.0% in the fourth quarter of 2019 and 21.8% in the first quarter 2019 due to lower level of taxable income relative to total income.

Capital

- Capital ratios remain strong with tangible common equity to tangible assets increasing 49 bps since first quarter of 2019.

- March 31, 2020 CET1 capital ratio of 10.90%, total leverage ratio of 10.02% and total risk-based capital ratio of 13.36%.

- Tangible common equity to tangible assets1 was 8.55% at the end of the first quarter compared to 8.84% at December 31, 2019 and 8.06% at March 31, 2019.

The Company repurchased 263,507 shares of common stock during the first quarter of 2020 at a weighted average price of $30.25 excluding commissions. The Company suspended repurchases during the quarter and does not expect to repurchase additional shares at this time. - On March 23, 2020, the Company announced a second quarter dividend of $0.27 per share, payable on June 15, 2020 to shareholders of record as of June 1, 2020.

Other Events

- On April 1, 2020, the Company completed the acquisition of Alliance Benefit Group of Illinois, Inc. (“ABG”) based in Peoria, Illinois.

- ABG provides retirement plan solutions for over 600 qualified retirement plans with over 40,000 plan participants and accumulated assets of $3.5 billion.

- ABG brings 70 new team members to EPIC Retirement Plan Services (“EPIC RPS”).

- ABG further diversifies the EPIC RPS customer base and supports its mission of “Helping America Retire.”

Corporate Overview

NBT Bancorp Inc. is a financial holding company headquartered in Norwich, NY, with total assets of $9.95 billion at March 31, 2020. The Company primarily operates through NBT Bank, N.A., a full-service community bank, and through two financial services companies. NBT Bank, N.A. has 146 banking locations in New York, Pennsylvania, Vermont, Massachusetts, New Hampshire and Maine, and is currently entering Connecticut. EPIC Retirement Plan Services, based in Rochester, NY, is a full-service 401(k) plan recordkeeping firm. NBT Insurance Agency, LLC, based in Norwich, NY, is a full-service insurance agency. More information about NBT and its divisions is available online at: www.nbtbancorp.com, www.nbtbank.com, www.epicrps.com and www.nbtinsurance.com.

Source: NORWICH, NY (April 29, 2020) – NBT Bancorp Inc