Senator Bill Doyle (R-Washington) has released partial results of his Town Meeting Day survey. Because of interest in the tax-related questions, which the Legislature will be gearing up for as they make the long, hard drive toward adjournment in May, Doyle tabulated those four of the 14 questions. He said that the results were not surprising among the 5,300 ballots he has counted so far (he expects to have the full results from all 7,500 returned ballots for all the questions in about two weeks). Town Meeting goers decisively opposed the payroll tax to reduce the cost of Medicaid; weren't too sure over the carbon tax; had a strong, but-split, opinion on the sugary drink tax, and supported a one-day sales tax holiday.

Senator Doyle began conducting his poll of Town Meeting participants in 1969. See tax-related results below.

For the sales tax holiday, Doyle said there would be some support among lawmakers because retailers and consumers have always looked forward to it.

It's a "pro-business program," Senator Doyle said, "The business people love it."

Governor Shumlin and most of his predecessors have not loved it, however, because it reduces state sales tax revenues. The sales tax holiday in 2010 cost the state about $2.2 million. While the holiday brought many shoppers off the Internet and into their local stores, the tax losses were from consumers who already shopped locally but simply put off their purchases until the sales tax holiday.

While Vermont's tax holidays were conducted under the auspices of Republican Governor Jim Douglas and tend to be more popular in the "Red" states in the Southeast, the conservative Tax Foundation has long opposed the plan, saying on its Web site:

"Political gimmicks like sales tax holidays distract policymakers and taxpayers from genuine, permanent tax relief. If a state must offer a “holiday” from its tax system, it is a sign that the state’s tax system is uncompetitive. If policymakers want to save money for consumers, then they should cut the sales tax rate year-round."

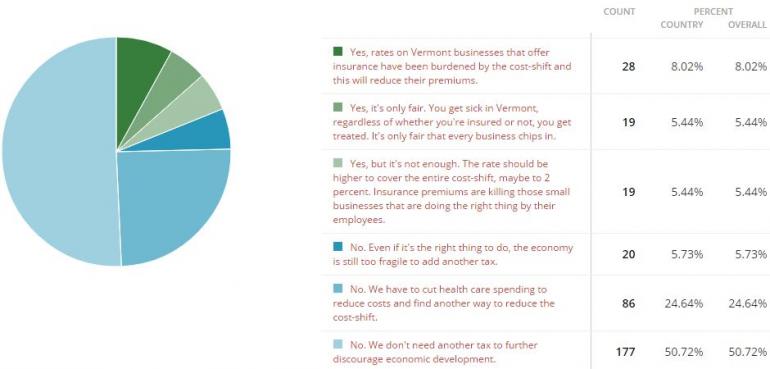

Doyle believes there will be some interest in the sales tax holiday this legislative session, but that there would be a long way to go at this point. (SEE DESCRIPTION OF LAST SALES TAX HOLIDAY BELOW ALONG WITH A TABLE OF NATIONAL INTEREST AND RELATED vermontbiz.com POLL RESULTS. The vermontbiz.com poll showed slightly higher support for the sugar tax).

Doyle Poll (Tax-related questions only, so far)

| Should Vermont have a payroll tax to reduce the cost of Medicaid? |

YES 23 |

NO 53 |

NOT SURE 22 |

| Would a carbon tax benefit Vermont's environment? | 31 | 42 | 25 |

| Should sugary drinks be taxed in order to reduce obesity? | 45 | 48 | 6 |

| Should Vermont have a one-day sales tax holiday? | 55 | 23 | 11 |

VermontBiz.com Quick Poll

|

The last time the sales tax holiday was in effect was in 2009 and 2010, when the Douglas Administration sought to at least put a smile on the face of consumers as the Great Recession lingered. Here were the parameters set by the Vermont Department of Taxes back then:

Sales of items of tangible personal property costing $2,000.00 or less that would otherwise be subject to sales and use tax will be exempt from sales tax and local option sales tax on the Sales Tax Holiday. The items must be purchased for personal use.

What is Exempt on the Sales Tax Holiday?

Who is Eligible for the Sales Tax Holiday?

Individuals purchasing qualifying items for their personal use are exempt from sales tax and local option sales taxes on the Sales Tax Holiday.

Who is not Eligible for the Sales Tax Holiday?

Businesses and business entities such as sole proprietorships, partnerships and corporations are not eligible for the exemption. Purchases charged to business accounts and purchases made using business credit cards or business checks are not eligible for the Sales Tax Holiday.

Vendor Participation

All Vermont businesses making sales of tangible personal property on August 22, 2009 and March 6, 2010 are required to participate in the Sales Tax Holidays. Out-of-state retailers registered to collect sales and use tax in the state of Vermont must participate in the Sales Tax Holidays.

Items which are not included in the Sales Tax Holiday

The following are not considered tangible personal property and are therefore not exempt from Sales Tax on the Sales Tax Holiday.

• Amusement charges including season passes for ski resorts.

• Charges for telecommunication services including prepaid telephone cards.

• Charges for cable television services.

• Digital downloads of music, movies and books.

Multiple Items on One Invoice

A customer can purchase multiple items on one invoice if the selling price of each item is $2,000.00 or less and still receive the exemption. Separate invoices do not need to be prepared. Separately stated delivery charges are not included when determining if an item exceeds the threshold.

Example: A customer purchases a kayak for $1,500.00, a tent for $400.00 and a backpack for $300.00. The delivery charge is $50.00. The invoice total is $2,250.00, however, each item is priced below the threshold and therefore the entire invoice including the delivery charge is exempt from sales tax.

Items Costing More than $2,000.00

The selling prices of items which exceed $2,000.00 are not reduced by the exemption amount.

Example: An item is priced at $2,500.00. The item is fully taxable. The $2,500.00 selling price is not reduced by the $2,000.00 exemption amount.

Bundled Transactions

A bundled sale of several items offered for sale at a single price will qualify for the exemption if the total price of the package is $2,000.00 or less.

Example: A computer package including a processor, monitor, keyboard and mouse with a sales price of $1,800.00 would be exempt because the sales price of the package is less than the $2,000.00 threshold. The same package with a selling price of $2,500.00 would not be exempt.

Splitting of items normally sold together

Items which are normally sold together cannot be split and priced separately in order to obtain the exemption on the Sales Tax Holiday.

Use Tax

Purchases exempt from Vermont sales tax are also exempt from use tax. Therefore, eligible items purchased from out of state retailers on the Vermont Sales Tax Holiday are exempt from Vermont use tax.

Coupons and Discounts

Discounts given by the vendor that reduce the selling price of the item can be used to determine if an item falls below the threshold for the Sales Tax Holiday. Coupons are treated as a discount if the coupon reduces the selling price and the vendor is not reimbursed by a third party. If a discount is applied to an entire order which includes both exempt items and taxable items, the vendor must allocate the discount between the selling price of the exempt item and the selling price of the taxable item.

Exchanges and Returns

The procedures for handling exchanges and returns during the Sales Tax Holiday are as follows:

• When a customer purchases an item of eligible property on the Sales Tax Holiday, but later exchanges the item for a similar eligible item, no sales tax is due even if the exchange is made after the Sales Tax Holiday ends.

• When a customer purchases an item of eligible property on the Sales Tax Holiday, but after the Sales Tax Holiday has ended the customer returns the item and receives credit on the purchase of a different item, the sales tax is due on the sale of the replacement item.

• If a customer purchases an eligible item prior to the Sales Tax Holiday and then returns the item on the Sales Tax Holiday and receives credit towards the purchase of a different eligible item, no sales tax is due if the sale of the new item takes place on the Sales Tax Holiday.

Rain checks for Eligible Items

A rain check allows a customer to purchase an item at a certain price at a later time because the item is out of stock. Eligible property purchased on the Sales Tax Holiday with a rain check will qualify for the exemption. Eligible property purchased after the Sales Tax Holiday with a rain check will not qualify for the exemption.

Layaways

Sales of eligible property sold under a layaway sale will qualify for the exemption on the Sales Tax Holiday if:

• The final payment for the layaway sale is made on the Sales Tax Holiday and the customer takes possession of the item on the Sales Tax Holiday;

OR

• The customer selects an item and the vendor accepts the item on the Sales Tax Holiday for immediate delivery upon full payment. The delivery can be made after the Sales Tax Holiday.

Order Date and Back Orders of Eligible Items

Items sold for $2,000.00 or less which are ordered on the Sales Tax Holiday are eligible for the exemption as long as the customer pays for the item in full on the Sales Tax Holiday. Delivery can take place after the Sales Tax Holiday. Back ordered items must be paid for in full on the Sales Tax Holiday to be exempt.

Rentals of Tangible Personal Property

Rentals of tangible personal property qualify for the exemption if the rental occurs on the Sales Tax Holiday.

Gift Certificates

The sale of a gift certificate is not taxable. Qualifying items purchased on the Sales Tax Holiday with a gift certificate are exempt from Sales Tax. Items purchased after the Sales Tax Holiday using a gift certificate are taxable even if the gift certificate was purchased on the Sales Tax Holiday.

Different time zones

The time zone of the vendor’s location determines the authorized time period for the Sales Tax Holiday.

Responsibilities of Vendors

It is the responsibility of the vendor to verify that purchases made on the Sales Tax Holiday qualify to be exempted from sales tax. If a vendor is doubtful that a particular purchase qualifies, the vendor should

collect the tax at the time of the sale. The customer has the option to later request a refund of the tax paid. (See Taxes collected in error.)

Taxes collected in error

Sales tax which is erroneously collected by a vendor on the Sales Tax Holiday should be refunded to the customer by the vendor. Erroneously collected sales tax that is not refunded should be remitted to the Vermont Department of Taxes. Customers who are charged sales tax in error on eligible items can receive a refund of the sales tax paid by:

• Bringing their receipt showing the sales tax paid to the vendor in order to obtain a refund.

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||