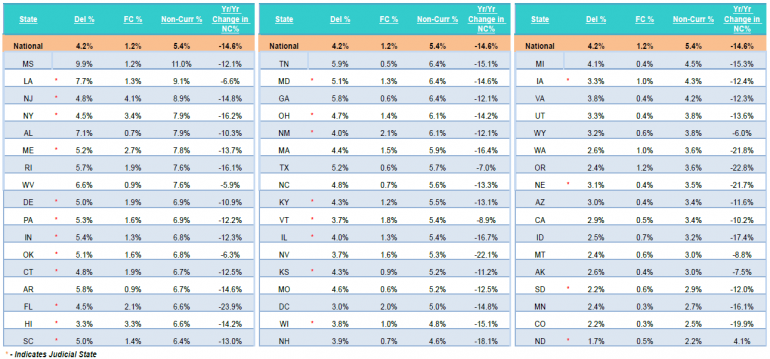

Vermont Business Magazine Rates of bad mortgages in the US have finally fallen below Great Recession levels, but are still historically high, as the volatility in real estate in the run-up to the recession turned out to be a reliable indicator of forthcoming trouble. Vermont has remained in the middle of the pack for non-current mortgages (foreclosures plus delinquent) for the last few years and like other states has seen dramatic reductions in the number of bad mortgages. And like other judicial states, Vermont's progress in cleaning up such mortgages has been somewhat slower than non-judicial states. Vermont's overall non-current rate was 5.4 percent (foreclosures 1.8 percent, delinquent 3.7 percent). This is down 8.9 percent from last year. It is the same rate as the US average.

Vermont Business Magazine Rates of bad mortgages in the US have finally fallen below Great Recession levels, but are still historically high, as the volatility in real estate in the run-up to the recession turned out to be a reliable indicator of forthcoming trouble. Vermont has remained in the middle of the pack for non-current mortgages (foreclosures plus delinquent) for the last few years and like other states has seen dramatic reductions in the number of bad mortgages. And like other judicial states, Vermont's progress in cleaning up such mortgages has been somewhat slower than non-judicial states. Vermont's overall non-current rate was 5.4 percent (foreclosures 1.8 percent, delinquent 3.7 percent). This is down 8.9 percent from last year. It is the same rate as the US average.

The national rate is down 14.6 percent, as the US is still working out problem loans. But at 58,700 April saw the lowest number of foreclosure starts since April 2005. The National delinquency rate is up from a 9-year low in March, but still 10 percent below last year’s level. Prepayment speeds (historically a good indicator of refinance activity) fell in April, despite interest rates being near 3-year lows. Active foreclosure inventory has now dropped below 600,000 for the first time since 2007.

April saw a typical seasonal increase in the national delinquency rate, which was up 3.77 percent from a 9-year low in March, but is still more than 10 percent below last year’s level.

Overall, Q1 refinance volumes were down 5 percent by count and down 23 percent by total loan amount originated, from last year.

Down 27 percent from last year, the inventory of loans in active foreclosure has fallen below 600,000 for the first time since 2007, but still remains 2X historical norms.

Vermont's non-current percent was 7.1 percent in April 2010 (US: 12.17 percent).

Distressed residential real estate transactions accounted for 33 percent of all sales in 2011. As the inventory of distressed properties has dried up nationwide, the overall share of cash sales has been on the decline, falling from 37 percent of all real estate transactions in Q1 2015 to 35 percent in Q1 2016.

This is down from a peak of 45 percent in 2011, but up from a pre-crisis Q1 average of 25 percent between 2005-2007. There is a clear disparity between the high and low ends of the market: cash sales made up approximately 30 percent of transactions on properties in the top 20 percent by value but over 60 percent of sales for those in the lowest 20 percent.