Emergency Board January 16, 2026.

by Timothy McQuiston, Vermont business Magazine The Vermont economy remains relatively healthy, even as the national economy presents uncertainty, but the state tax revenue gravy train is running out of steam and the surpluses elected leaders have counted on to plug holes, as with the property tax, likely will not be available for much longer. While overall revenues have been resilient, revenues from the healthcare segment and from corporate income taxes are weakening. That was the message of the state economists and their consensus revenue update, which they presented last Friday (January 16).

The January 2026 economic review and revenue forecast update was prepared for the Vermont Emergency Board by Jeff Carr of Economic & Policy Resources, on behalf of the Scott Administration, and by Tom Kavet of Kavet, Rockler & Associates, on behalf of the Legislative Joint Fiscal Office. They summarized national and state economic conditions, revenue collections through the first half of FY2026, and recommended forecast adjustments relative to the July 2025 baseline.

Carr said in his report: "Against the backdrop of continued federal foreign, fiscal, immigration, and trade policy uncertainty, the latest staff recommended consensus revenue forecast update for fiscal years 2026, 2027, and 2028 (and including fiscal planning revenue estimates for fiscal years 2029, 2030, and 2031) calls for essentially “holding the line” for the forecast update period."

Kavet said their prior projects were very close to actual and, overall, the fiscal year (which began July 1, 2025) has been "uneventful." He said, "There is a lot of uncertainty still, so there is a lot of risk, but there's upside risk and downside risk, even though a lot of the numbers are big. But the change from the last forecast is quite modest."

Carr added that much of the action is in the healthcare related revenues, whereas in recent years the focus has been on the personal income tax.

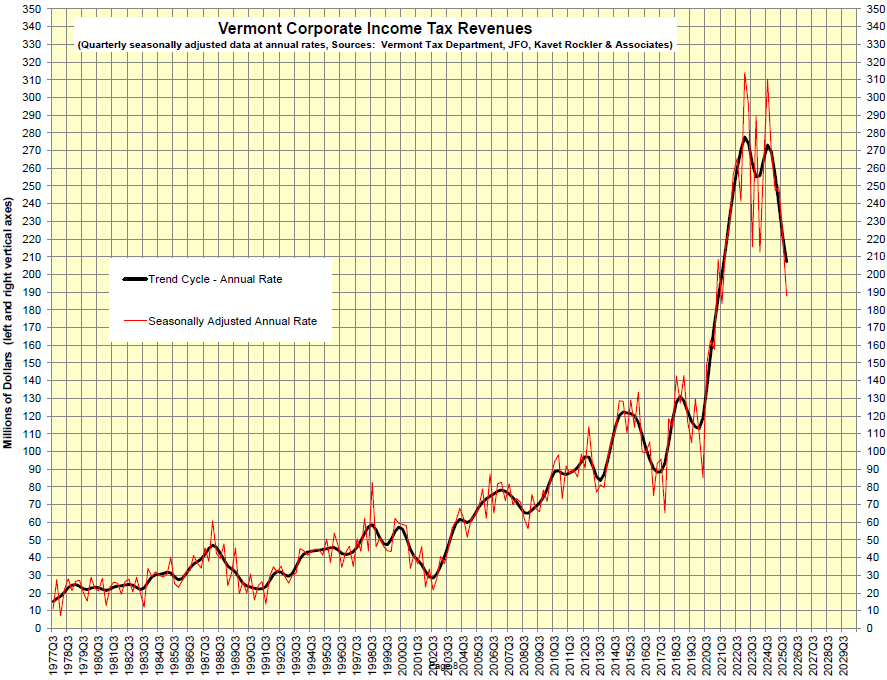

Kavet added that, "In the standard General Fund categories, the category that gave us the most concern was the Corporate Income Tax. We did a pretty deep dive... You can see how volatile Corporate is. We got a lot of refunding, even more than we expected, in November and December."

They could not find a definitive reason for this as corporate profits are at record levels. Still, they slightly downgraded Corporate while Personal Income they anticipate increasing by a small amount going forward.

Meanwhile, Kavet said in his report that interest income (which has been a significant revenue source since the COVID-19 pandemic with the infusion of federal funds) has been retreating very close to expectations, as state unrestricted cash reserves shrink in accord with required federal spending deadlines. Slightly lower interest rate assumptions will shave earnings by about $0.5M per year over most of the forecast period but are still expected to bring in about $42M in FY26 and $28M per year in FY27 and beyond.

• Lottery revenue has been the weakest component of the E-Fund, lagging targets by more than 10% through the first half of the year, despite two national jackpots in excess of $1 billion. Lottery ticket purchasers are often on the lower leg of the K-shaped economy and have had less disposable income of late with which to spend on games. The Liquor and Lottery Department also reported a year-end FY25 net negative deficit of $654,969 which they retired via a reduced transfer in September. Even with an expected bounce-back in the second half of this fiscal year, Lottery revenues are expected to be about $2 million below prior July estimates in FY26 and throughout the forecast period.

• Strong December collections pushed total Transportation Fund revenues slightly above target (+0.2%) for the first half of FY26, after trailing in each of the preceding five months.

The E-Board members are Chair Governor Phil Scott and legislative leaders from the four money committees Senator Andrew Perchlik (Appropriations); Senator Ann Cummings (Finance); Representative Robing Scheau (Appropriations); and Representative Emilie Kornheiser (Ways & Means).

Clockwise from top: Governor Scott, Representative Scheau, Senator Perchlik, Tom Kavet, Jeff Carr, Senator Cummings and Representative Kornheiser. Screen grab.

Core conclusion. The U.S. economy slowed from 2.8% growth in 2024 to roughly 2.0% in 2025, with much of the resilience driven by extraordinary, concentrated investment in artificial intelligence (AI) infrastructure and related technologies; absent that investment, growth would have been weaker and more broadly negative risks would dominate.

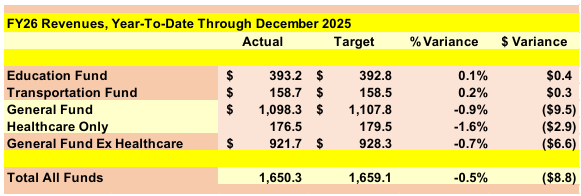

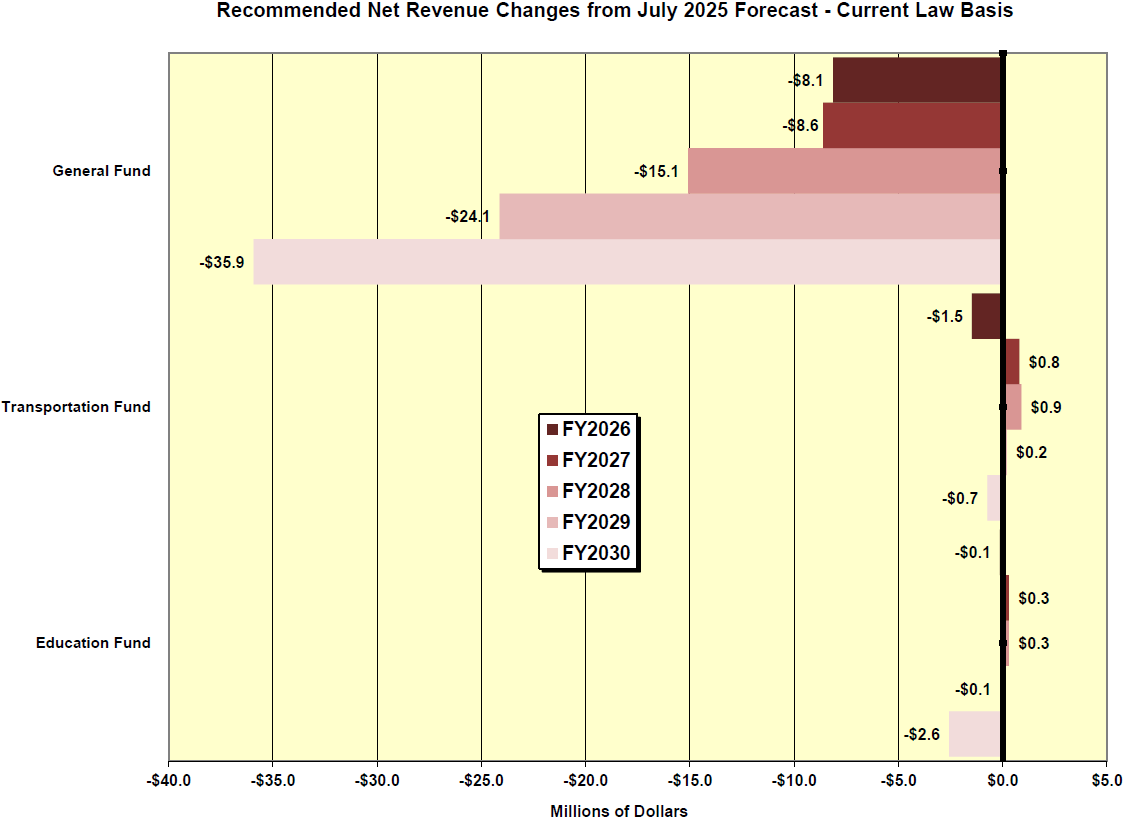

Revenue impact. Despite macroeconomic headwinds and policy uncertainty, Vermont’s aggregate revenues through the first half of FY2026 were very close to prior targets, prompting only modest downward adjustments to the multi‑year forecast: recommended net changes from the July 2025 forecast are small in percentage terms (about -0.3% in FY26 and -0.2% in FY27 across all funds), though the General Fund shows larger nominal reductions driven largely by healthcare tax changes.

Primary risks. The forecast highlights three dominant cross‑currents shaping the outlook: (1) AI investment euphoria that has produced outsized equity gains and concentrated growth; (2) deglobalization policies—especially tariffs—and restrictive immigration measures that raise inflation and reduce labor supply; and (3) expanding fiscal and monetary stimulus that could temporarily support growth but increase long‑term debt and market risks.

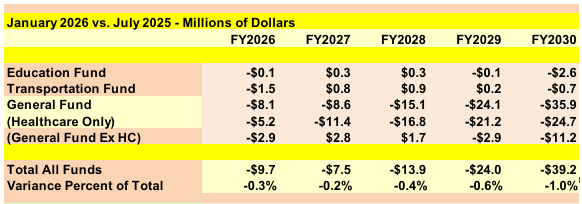

Kavet wrote in his report that "with the macroeconomic outlook also relatively close to that of the prior July update, the revenue changes herein are among the lowest ever recommended in a regular revenue update. The lone exception is the Healthcare Fund, which will suffer from tax rate reductions in the Hospital Provider Tax due to the recently enacted 2025 Reconciliation Act (H.R.1). These progressive rate reductions will reduce revenues in the total Healthcare Fund by as much as 7% by FY30, relative to baseline July estimates. This will cause actual year over year declines in total Hospital Provider revenue of between 4.3% and 8.1% during the period between FY28 and FY31and declines in total Healthcare revenues of between 1.4% and 3.4% during this same period. This will ultimately feed through to the General Fund, of course, lowering revenues accordingly."

Economic Review and Drivers

AI investment and concentration of gains. A massive wave of AI‑related capital spending—data centers, energy infrastructure, hardware and software—accounted for a very large share of 2025 GDP growth and has driven a stock market boom that concentrated wealth among the top decile and especially the top 1% of households. That concentration has produced strong consumption among the wealthy while leaving middle‑ and lower‑income households with weaker wage growth and rising costs from tariffs, producing a K‑shaped economic pattern.

Deglobalization and tariffs. The report documents how recent tariff policies have raised input costs, reversed disinflation trends, and created hiring and investment uncertainty. Tariffs have already reduced manufacturing employment and job openings, and their full price effects on consumers are expected to materialize over time as businesses pass costs along, eroding discretionary spending for many households.

Immigration and labor supply. Restrictive immigration policies have materially reduced net foreign immigration—from about 2 million in 2024 to 1 million in 2025 and projected to fall further—subtracting roughly 0.5 percentage point from real GDP growth and tightening labor markets in sectors that rely heavily on immigrant labor, including healthcare, construction, and transportation.

Monetary and fiscal policy interactions. The forecast anticipates more expansionary policy in 2026—Fed rate cuts, an end to quantitative tightening, mortgage purchases to lower long‑term rates, and deficit spending from federal reconciliation measures and proposed “tariff dividend” payments. While these measures could support near‑term growth, they also raise long‑term debt service costs and crowd out private investment, increasing vulnerability to bond market stress if investor confidence weakens.

Macro outlook and vulnerabilities. The report stresses that the narrowness of the AI investment tailwind makes the economy vulnerable to downside shocks. The short useful life of some AI infrastructure and the leverage used to finance it could produce large losses if returns disappoint, creating a bubble‑like risk similar to past technology cycles.

Vermont Revenue Performance and Forecast Changes

Year‑to‑date collections. Through December 2025 (first half of FY26), Vermont’s total collections across the Education, Transportation, and General Funds were within about 1% of targets, with the Education Fund up slightly, the Transportation Fund essentially on target, and the General Fund modestly below target driven by large corporate refunds and healthcare tax changes.

Notable variances by source.

- Corporate income tax experienced significant volatility: large refunding in November and December produced a year‑to‑date shortfall of roughly $24.9 million (about -24.7% relative to target), prompting a downward revision to FY26 corporate estimates by about $16.5 million; however, the report treats much of this volatility as episodic rather than structural.

- Personal income tax receipts were ahead of target by about $17.1 million (+2.8%), reflecting both underlying growth and some large tax‑year events that could produce upside in final filings.

- Sales and use taxes and major consumption taxes were close to expectations, with Sales & Use at +0.4% and Motor Vehicle Purchase & Use at +3.2% through December; Meals & Rooms trailed slightly (-1.1%) and lottery receipts were notably weak (more than 10% below target).

- Transportation Fund collections were slightly above target (+0.2%) after a strong December, with fuel taxes and fees near expectations and motor vehicle taxes up modestly.

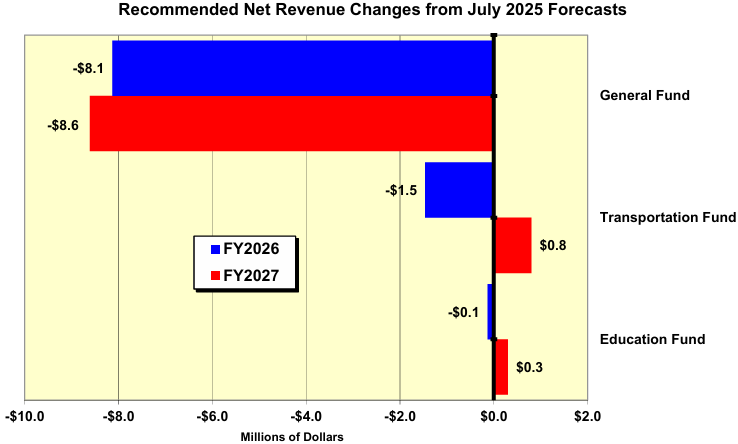

Forecast adjustments. The consensus JFO and Administration recommendation reduces total General Fund revenues modestly across the forecast horizon, with larger nominal declines in the Healthcare Fund component due to federal changes (notably reductions in the Hospital Provider Tax under the 2025 reconciliation legislation). The table of recommended net revenue changes shows General Fund reductions of roughly $8.1 million in FY26 and $8.6 million in FY27, with cumulative and larger declines projected in later years as healthcare tax rate reductions phase in.

Magnitude and context. Even with these adjustments, the report emphasizes that the January update represents one of the smallest regular forecast revisions in recent memory, reflecting that aggregate collections and the macro outlook remain broadly consistent with July expectations; the most significant structural concern is the multi‑year reduction in healthcare‑related revenues tied to federal law changes.

Risks, Uncertainties, and Sectoral Notes

Corporate revenue volatility. Corporate tax receipts remain the most volatile revenue source, subject to episodic refunds and large single‑entity payments. The report’s analysis of recent large refunds did not find a clear pattern tied to macro conditions, suggesting much of the shortfall may be idiosyncratic, though the potential for future volatility remains elevated given corporate profit dynamics and tax timing issues.

Inflation measurement issues. The government shutdown disrupted key economic data releases (notably October CPI), introducing methodological distortions—particularly in shelter cost estimates that rely on rolling averages—likely understating inflation in late 2025 and complicating near‑term policy interpretation.

Housing and home prices. Home price growth decelerated in 2025 relative to pandemic peaks; Vermont’s year‑over‑year home price growth was about 3.0% in the third quarter of 2025 after much larger gains earlier in the cycle. The report expects that continued Fed rate cuts in 2026 could increase inventory and flatten or reduce prices in many markets, with home price growth likely to be flat or modestly negative for an extended period in some areas.

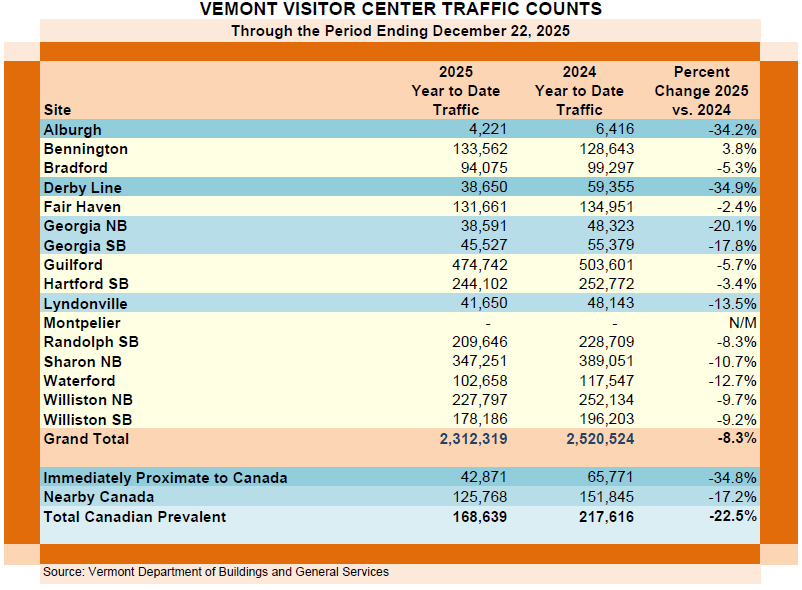

Tourism and Meals & Rooms. Tourism indicators were mixed: Meals & Rooms tax receipts were slightly below target, and visitor center traffic near the Canadian border fell sharply due to reduced Canadian visitation tied to political and trade tensions, contributing to weaker tourism‑related revenues.

Aggregate Meals and Rooms tax revenues have been just shy of targets (-1.1%) to date. The share of this revenue source going to the E-Fund is down a bit more (-2.3%) than the G-Fund share (-0.5%), since the E-Fund receives 100% of the Short-Term Rental Surcharge, which has been running slightly behind overall M&R growth.

Visitor Center traffic overall was down -8.3% overall and Canadian border crossings overall were down -22.5%.

Labor market softening. National employment growth slowed after tariff announcements, with job growth averaging fewer than 12,000 jobs per month since April 2025 and unemployment edging higher; Vermont’s unemployment remained low relative to the U.S. but the state is not immune to national softening trends.

Long‑term fiscal risks. The report flags the rapid growth in federal debt—more than $38 trillion at end of 2025—and the potential for higher long‑term interest rates and bond market stress if investor confidence erodes. Political threats to central bank independence are also noted as a risk that could raise borrowing costs and complicate monetary policy effectiveness.

Policy Implications and Recommendations

Conservative forecasting posture. Given the concentrated nature of the AI investment tailwind and the episodic volatility in corporate receipts, the report recommends modest, cautious adjustments rather than large structural changes to Vermont’s fiscal plans, while explicitly calling out the need to monitor healthcare revenue declines tied to federal law changes.

Prepare for volatility. Policymakers are advised to recognize the potential for large, unpredictable swings in corporate tax receipts and to avoid relying on one‑time or highly volatile revenue sources for ongoing expenditures; contingency planning and reserve management are emphasized.

Monitor data disruptions. The methodological distortions from the government shutdown warrant careful interpretation of inflation and labor market indicators; the report suggests that policymakers should be cautious in drawing firm conclusions from short‑run data until series are fully restored and revised.

Targeted attention to tourism and border effects. The decline in Canadian visitation and its localized revenue impacts suggest the need for targeted monitoring of tourism‑dependent regions and potential policy responses if cross‑border travel remains depressed.

Long‑term fiscal discipline. The combination of rising federal deficits, potential crowding out of private investment, and the risk of higher long‑term rates argues for prudent state fiscal management and attention to structural budget risks over the medium term.

Source: 1.16.2026. JFO Revenue Forecast Update

To support vital journalism, access our archives and get unique features like our award-winning profiles, Book of Lists & Business-to-Business Directory, subscribe HERE!