Full labor information is not available for the month of October and it is not clear if and when it might be available. But with the federal government reopened, certain data is now available. See national report below.

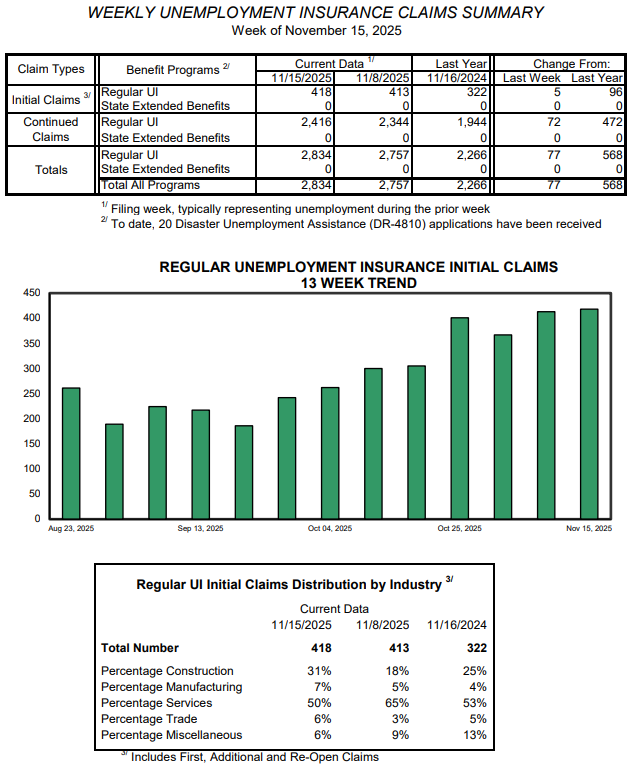

by Timothy McQuiston, Vermont Business Magazine Vermont weekly unemployment claims for the week ending November 15, 2025, increased by a small amount, as claims have more than doubled over the last two months. New claims were 418, up 5 claims from the week before and up 96 from last year at this time. Claims were 186 in late September. Claims, which tend to be lowest in the summer, were 181 at the end of September 2024.

Meanwhile, the government shutdown, the longest in history, is over. The stock market rallied Friday after a rocky week on sketchy AI-related company results but with renewed hope of a Federal Reserve Board interest rate cut in early December. This looks likely as economic reports show uncertainty. See below.

In Vermont for the weekly labor UI claims report, manufacturing accounted for 7% of the total, down 2 points from the previous week. Manufacturing overall has become a smaller part of the Vermont economy over the last 25 years and that trend appears to be continuing. The Service industry, which typically accounts for the most claims, last week was 50% of the total, down 15 points. Construction was 31%, up 13 points as much of the industry scales back with the cold weather.

For the week, Vermont total unemployment insurance claims were 2,834 (up 77 for the week and up 568 from this time last year).

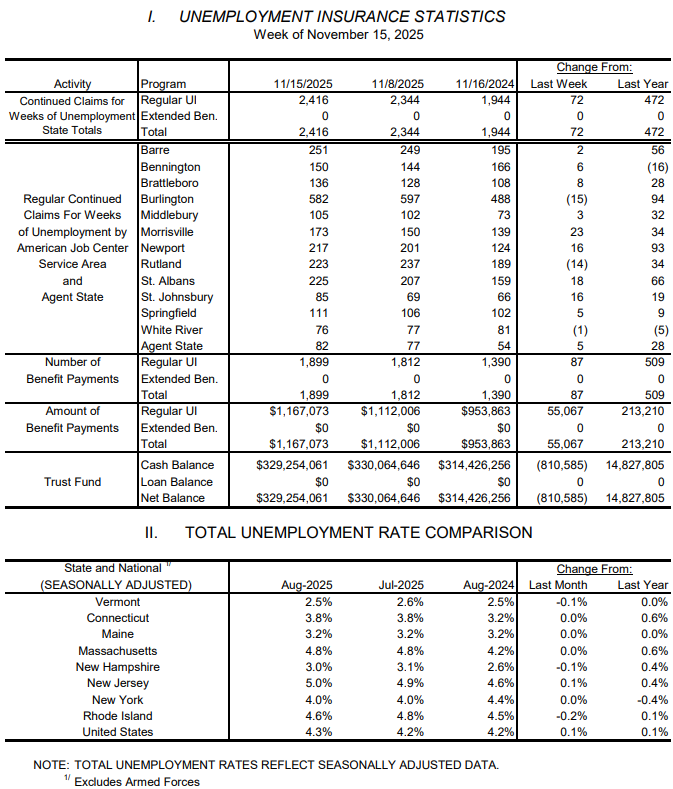

The Vermont Unemployment Trust Fund is well capitalized. As of the most recent data, there was $329.3 million in the Trust Fund, down about $800,000 (as claims are paid out on one side, employers are contributing to the fund on the other). The pre-pandemic Trust Fund balance on March 1, 2020, was $506.2 million.

National Employment & Economy

According to Kory Kantenga, Ph.D., Head of Economics, Americas @ LinkedIn:

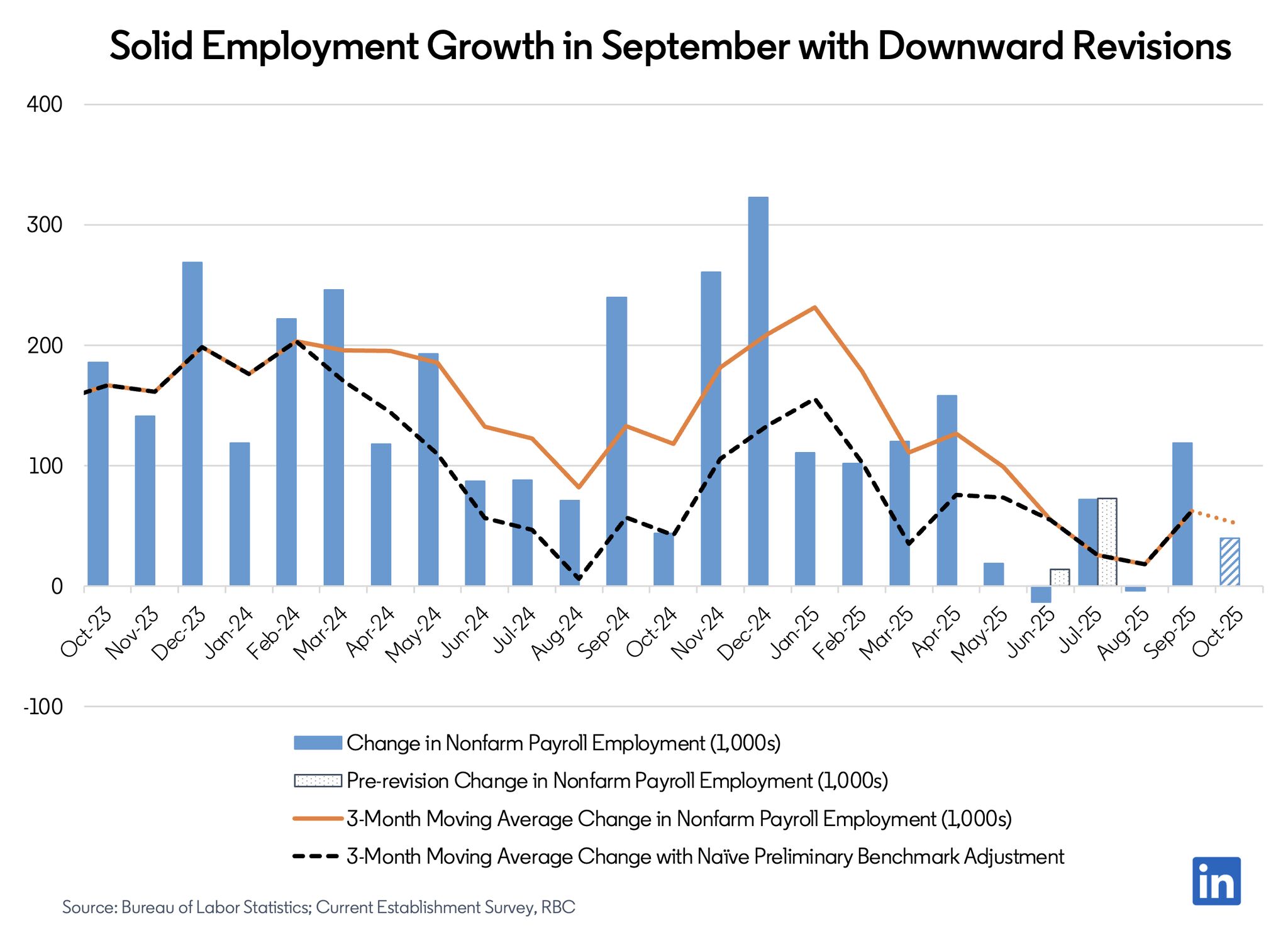

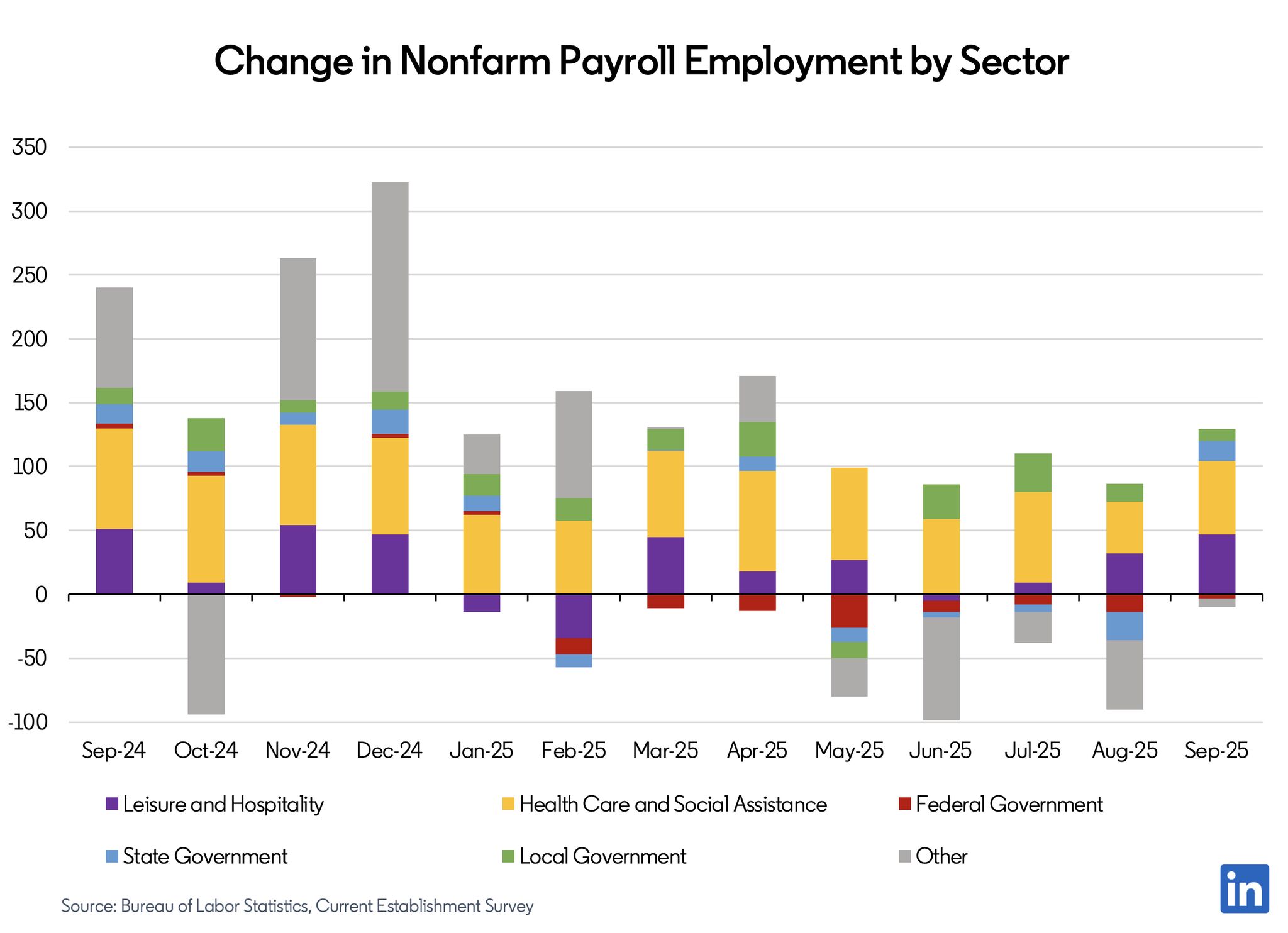

"We received September’s job report On November 20, 2025, which was pre-empted by the government shutdown in early October. Though old news at this point, today’s report provides meaningful information on trends seen throughout the year. The most surprising part of the report is how well it aligns with prior trends (e.g., skewed payroll, unemployment uptick, muted labor supply growth) after a summer slowdown. Outside of Healthcare and Social Assistance, Leisure and Hospitality, and Local Government, nonfarm payroll employment has shrunk by 151K jobs this year, including 94K Federal Government jobs. As job growth remains heavily skewed, the labor market remains fragile."

1. Nonfarm payrolls increased by +119K in September, well above consensus estimates with revisions in July (+7K) and August (–26K). Today’s revisions mean that employment contracted in both June and August –– the first negative payroll changes recorded since December 2020. The higher than usual response rate (due to the shutdown) may mean fewer revisions in December, however, we have no information about who responded to determine that. Outside of Healthcare and Social Assistance, Leisure and Hospitality, and Local Government, nonfarm payroll employment has shrunk by 151K jobs, including 94K Federal Government jobs.

2. Unemployment ticked up to 4.4% which is higher than expected. The unemployment increased due to a combination of more quits and permanent job loss. The household survey indicated also that employment increased by +251K from August to September for an average decline of –28K a month this year.

3. The labor force participation rate increased slightly and the employment-to-population ratio remained flat for 25-54 years. The change in average hourly earnings decelerated to an annualized rate of 3% from 5% in August. Nothing in September’s report indicates a change to the trend of flat labor supply growth and a lack of wage-based inflationary pressure.

4. Employment at Temp Agencies declined by –16K, continuing its slide since the start of the summer.

"The next jobs report will be published on December 16 and include a read on payrolls in October, however, household data was not collected so no data on the unemployment rate, labor force participation, or earnings will be available for October 2025 going forward. May the best imputation win!"

Stock Markets

Meanwhile, it appears the Fed's concern over a rise in inflation is outweighed by a weakening economy, which led them to cut interest rates by 25 basis points September 17, 2025. Analysts are now anticipating that the Fed will respond to the overall economic news by cutting rates by another 25 basis points at its meeting December 9-10, as it weighs the economic weakness and employment (rate cut) versus inflation (no rate cut).

The current annual U.S. inflation rate is 3.0%, based on the 12-month increase in the Consumer Price Index (CPI) through September 2025. This marks a slight rise from August's 2.9% rate, lower than what many economists had forecast, but higher than the Fed's goal of 2%.

Wall Street has lobbied for a rate cut as it should stimulate economic activity and lower costs for businesses and consumers. It also makes stocks a more appealing investment vehicle if interest rates are low for other types of investments tied to high interest rates, like certificates of deposit (CDs) and money markets. As those rates fall, the "wall of cash" might come washing back to equities, or not. As of now, the markets are betting on a rate cut.

The Dow, S&P 500 and NASDAQ were up about 1% Friday after losing ground most of the week. The three indices were still down about 2% for the week and have fallen below late-September levels. AI and bitcoin both suffered.

Lower interest rates should also lower mortgage rates. These rates are not directly tied to the Fed rates and have come down more slowly than expected. There is also hope that if interest rates fall rents may also fall as overhead cost pressure declines on landlords and housing development and competition increases. Mortgage rates already have fallen.

As of late November 2025, the average 30-year fixed mortgage rate is hovering around 6.26%. Rates have seen a slight increase in recent weeks but remain significantly lower than the 2024 peak of 7.22%. In 2025, they peaked at 7.08% in May, as refinancing surged.

To support vital journalism, access our archives and get unique features like our award-winning profiles, Book of Lists & Business-to-Business Directory, subscribe HERE!