Consensus Vermont tax revenue projections.

by Timothy McQuiston, Vermont Business Magazine

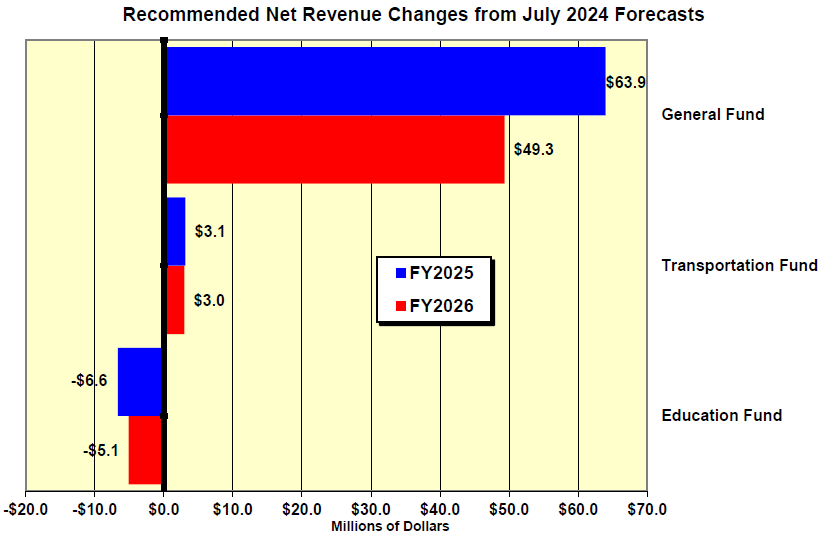

State economists Jeff Carr, for the Scott Administration, and Tom Kavet, for the Legislature, presented their consensus tax revenue report on January 22. Revenues in FY25 to date (which began July 1, 2024) have been close to expectations, with a few large Corporate revenue events and broader strength in Personal Income flows that have lifted General Fund revenues about 6.0% above targets or $63.9 million.

The caveats to these forecasts mostly have to do with Trump Administration policies regarding tariffs and immigration, along with ongoing concerns on the federal budget deficit and inflation concerns. The Fed declined to cut rates in January 29 after three cuts late last year, calling it a "pause."

The Education Fund has been slightly below target (-2.1%), due to weakness in the two large consumption taxes (Sales & Use and Meals & Rooms) that feed into the Education Fund, both of which had expanded taxes that appear to be underperforming, along with disappointing Lottery receipts. Through the first six months of FY25, the Transportation Fund is about 2.7% above targets, led by strong Motor Vehicle Purchase & Use tax revenue and no other major T-Fund revenue component that is below expectations.

FY2026 General Fund revenues are expected to exceed the July forecast by $49.3 million, while the Transportation fund will see minimal growth of $3 million (versus $3.1 million in FY25) and the Education Fund is expected to be $6.6 million below targets in FY25 and $5.1 below in FY26.

Most of the General Fund upgrade derives from the re-estimation of Personal Income revenues. PI receipts are currently about $22M over target to date and represent about half of the net General Fund upgrade - mostly in the Estimated payments component.

Inflated asset prices are also a contributing factor in recent and expected future PersonaI Income revenue strength. With almost every class of asset experiencing extraordinary value growth (home ownership, stock market, etc), large capital gains liabilities are elevating tax payments, but also exacerbating revenue volatility.

However, the latest state tax revenue report for December 2024 (released February 3, 2025), showed that all three major indices missed their targets by a small amount. The General Fund was off 1.15%, with the vital personal income tax missing by 2.03%; the Transportation Fund was off by 0.68% and the Education Fund was off by 3.18%.

Despite two years of sustained high real interest rates, the economy has not significantly slowed, and "roared" through 2024 with recent US unemployment at 4.1% (December 2024), real GDP growth at 2.8%, inflation down to 2.4% (PCI basis), sturdy productivity gains, 48 consecutive months of job growth and the stock market posting multiple record highs.

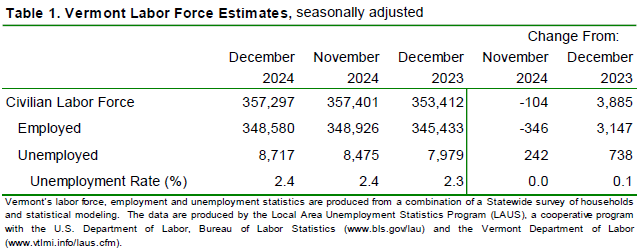

In Vermont, the seasonally adjusted statewide unemployment rate for December 2024 was 2.4 percent. This reflects no change from the prior month’s revised estimate. Vermont has the second lowest rate in the nation behind South Dakota (1.9%). Nevada again has the highest rate (5.7%).

This “stellar” economic performance has boosted State revenues slightly above expectations, except for a few underperforming new taxes, and kept total first half FY25 revenues across all three major funds 3.7% above July estimates.

While FY26 will also benefit from this inertia, some of the proposed economic policies of the incoming White House administration could slow growth in FY27 and beyond. The tariffs against China (10%), Mexico (25%) and Canada (25%) went into effect February 4, 2025. Mexican and Canadian tariffs were paused for a month following an agreement with the US on stationing 10,000 troops along the Mexican border, and more illegal drug interdiction in Canada.

Canada, a key trading partner with Vermont and many northern states, has already retaliated with its own tariffs and the province of Ontario has taken US alcoholic beverages off its shelves.

The stock market fell Friday and in early trading Monday, which was softened by the Mexican news.

While it is too early to know exactly what these policies will have, the coming July economic and revenue update will have more specific quantitative information as these are clarified and implemented.

The aggregate economy entering 2025 is exceptional – and significantly better than forecast a year ago or even six months ago. Inflation was finally tame enough through August to warrant three Fed interest rate cuts totaling 100 basis points from September through December, providing fuel for stock market euphoria, if not huge or immediate reductions in most borrowing costs.

Expected future rate cuts this year, however, may be among the first casualties of the new administration’s oft-broadcast economic policies, with concerns about their effects on inflation. While we are still expecting two (instead of four) rate cuts later this year, the Fed is now “on hold” and some are even discussing the possibility of rate hikes.

The Trump Administration economic policies of greatest potential negative impact are widespread tariffs, mass deportations, reductions in immigration, and expanding deficits. All of these could exacerbate inflationary pressures. Given Republican majorities in both the House and Senate (though thin), each of these policies are expected to be implemented to some degree over the next four years, but policy details and implementation timing are both uncertain.

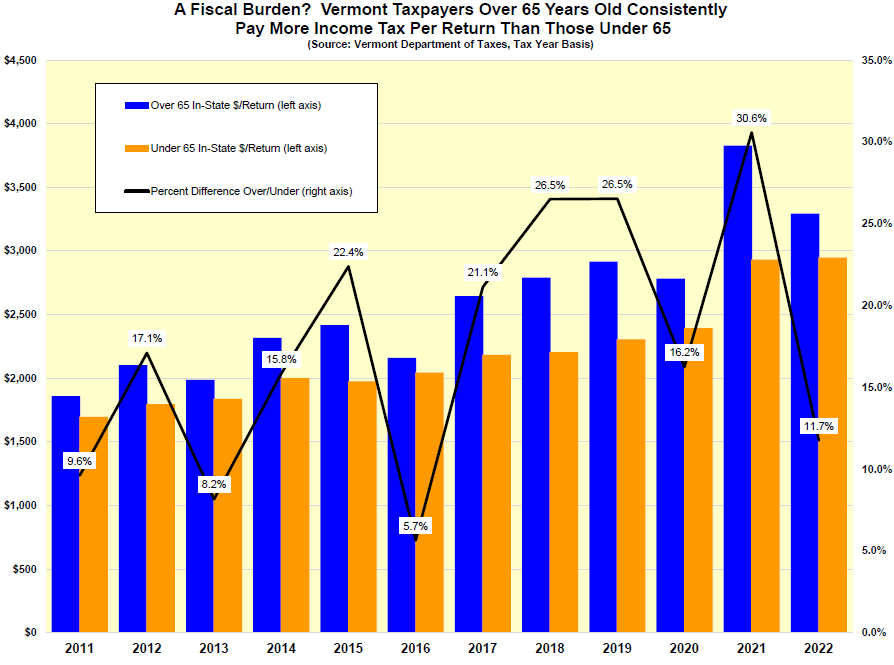

Meanwhile in Vermont, growth in older age cohorts in the State are sometimes cited as a future fiscal threat, since they are beyond working age and presumably would not be earning taxable income. In fact, per the chart below the preceding page, Vermonters over age 65 consistently pay more income tax per return than those under age 65 and rarely have children enrolled in K-12 education – the State’s largest single fiscal expense.

Source: 2.3.2025. Kavet, Rockler & Associates LLC. Williamstown, Vermont. Kavet, Rockler & Associates – Economic and public policy consulting

To support vital journalism, access our archives and get unique features like our award-winning profiles, Book of Lists & Business-to-Business Directory, subscribe HERE!