A Tale of Misplaced Trust, Unfortunate Decision-making, Lengthy Delays, and Missed Opportunities

VermontBiz Most Vermonters are familiar with the general storyline of the EB-5 fraud committed in the Northeast Kingdom involving Jay Peak, Burke, and AnC Bio Vermont. News reports which were upbeat and promising in the early part of the last decade took a dark turn as details began to emerge of financial improprieties. Three individuals were ultimately convicted of felony offenses related to the fraud, the State’s reputation was bruised by national press coverage, and in July Vermont taxpayers learned they would foot the $16.5 million bill of a global settlement reached between the Vermont Attorney General and a group of EB-5 investors.

This week my office released an audit of the State’s role in the EB-5 fraud. The audit represents the first comprehensive, one-stop accounting of how State government did (or did not) provide oversight of the EB-5 program – specifically the Burke and AnC Bio Vermont projects.

In July 2018, Vermont’s former Attorney General requested that we audit the State’s involvement with the Jay and Burke projects, stating that an audit would address the loss of trust in State government that had resulted from the fraud. Shortly after we began our work, a Federal grand jury issued indictments in the criminal cases against Ariel Quiros, Bill Kelly, and Bill Stenger. After consulting with the Attorney General’s Office, we decided to defer continued work on the audit to avoid interfering with the ongoing investigations and legal proceedings. Once the criminal cases closed and the global settlement agreement was in place, we were free to resume our work.

What did we find?

In short, we found a pattern of misplaced trust, unfortunate decision-making, lengthy delays, and missed opportunities to prevent or minimize fraud. Our findings are highlighted below. We also present two graphic displays of key milestones in the AnC Bio Vermont and Burke frauds in order for Vermonters to understand the process by which State government slowly came to understand the scope of the fraud and act accordingly.

At the highest level, our findings should not be entirely surprising. From its creation, the Vermont Regional Center, the EB-5 office housed in the Agency of Commerce and Community Development (ACCD), had two competing duties – to market and promote EB-5 projects, and also to regulate them. Experts and policymakers have long warned against such arrangements for fear that an agency relied upon to help a project succeed may be reluctant to exercise its regulatory powers. In addition, a marketing office may not have the skill sets needed to properly regulate complex financial arrangements such as EB-5. Unfortunately, this proved all too true at ACCD.

We hope our audit is read with a single aim in mind – learning from the State’s role in the EB-5 saga in order to prevent such a thing from happening again.

(The full report can be found here, and we have compiled a series of court documents and original correspondence between the State and Jay Peak officials here.)

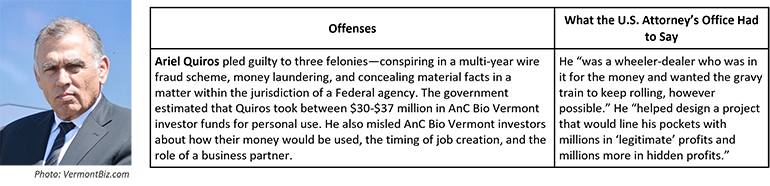

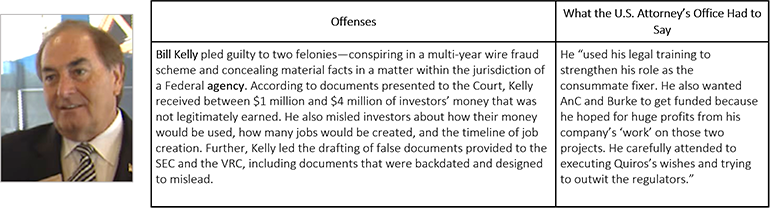

Though our report focuses on the role and actions of State government in the EB-5 fraud, it is important to provide a brief snapshot of the Jay Peak officials who perpetrated it.

Structural Design Flaw From the Outset

- When the EB-5 Regional Center (VRC) was created, the State assigned oversight to ACCD. At that time, USCIS, the federal agency that oversees EB-5, did not require regional centers to monitor the securities aspect of the program, although there was no prohibition on that. While there was no hint of fraud in the early years of the VRC, EB-5 had experienced fraud in other parts of the country. Compare this oversight system to the one established for Vermont’s well-regarded captive insurance program. Like EB-5, the captive insurance program has both marketing and regulatory components. However, unlike EB-5, the State’s captive insurance activities were always administered in partnership by ACCD and BISHCA (DFR’s predecessor). That is, the marketing/promotion functions were kept separate from the regulatory functions. As it turned out, ACCD eventually acknowledged that it did not have the necessary legal authority or tools and turned over regulatory duties to DFR. Had the State started this way, much grief may have been avoided.

- The State’s understanding of its role as administrator of the Regional Center was limited by USCIS’ failure at that time to require explicit oversight of the securities element of EB-5. Nevertheless, ACCD did not even have written policies and procedures defining its oversight responsibilities. Had the State undertaken that task (best practice), it may well have recognized the importance of the securities issue (and risks of fraud) and the need for DFR’s assistance from the beginning.

- In February 2012, a firm that worked closely with Jay Peak, and which in fact had created and promoted the original Jay Peak securities offering materials, terminated their relationship because they no longer had confidence in the accuracy of representations made by Jay Peak or in the financial status of and disclosures of the partnerships.

- In a telephone call the firm told the ACCD Secretary that $13 million was missing from Jay Peak’s bank accounts. The hint of fraud offered an opportunity for ACCD to seek help from DFR. They didn’t.

- Instead, the ACCD Secretary asked Stenger about the allegations. Stenger denied them and offered records in defense. The ACCD Secretary said he was satisfied with the documentation Stenger provided and dropped the matter. With so much at stake, though, due diligence should have included more than a review by a non-auditor of records hand-selected by Stenger. In fact, the U.S. Attorney later determined that the records Stenger provided covered up how the defendants misused investor funds.

- In a telephone call the firm told the ACCD Secretary that $13 million was missing from Jay Peak’s bank accounts. The hint of fraud offered an opportunity for ACCD to seek help from DFR. They didn’t.

- At about the same time (early 2012), DFR heard allegations that Jay Peak was using an unlicensed broker-dealer. Although a seemingly minor technical issue, this was now the second time an EB-5 securities matter was brought to the State’s attention. DFR responded that it was not conducting an investigation but was “gathering information regarding some of their offerings.” At the time, DFR had no direct regulatory role regarding EB-5, and we found no other documents pertaining to this allegation. Note that the lack of records about events that occurred more than a decade ago is not evidence of wrongdoing.

Failure to Require Audits When Concerns First Raised

- Ongoing Monitoring and Project Oversight Poorly Defined and Documented Misleading and Confusing Claims That the State “Audited” EB-5 Projects

- A May 2012 meeting with the former business associated with Jay Peak led ACCD to request that Jay Peak contract for a financial audit. Stenger initially agreed but, four months later, informed the VRC Director that he would not pay for the audit. The State dropped the matter thinking it didn’t have the authority in the MOU to compel the completion of an audit, although there is language that might have supported a legal challenge, and the State could have used other leverage points.

- The various memorandums of understanding (MOU) between the VRC and Jay Peak required Jay Peak to submit quarterly reports, but they did not articulate a clear process for reviewing the financial activities of the projects. But while the MOUs may not have created a legal requirement on the part of the ACCD to perform robust financial oversight, this does not mean that ACCD should not have maintained the level and type of oversight that would prevent or mitigate inappropriate actions on the part of its approved EB-5 projects.

- One of VRC’s few oversight actions was holding quarterly meetings with the projects. However, while there is documentation showing that meetings were held with Stenger, ACCD kept no overall record of when they were held nor what was reviewed at each meeting. Thus, it is impossible to determine how often ACCD officials held quarterly meetings with Jay Peak or what was discussed. This is no small matter of bureaucratic paperwork. Take the AnC Bio project, for example. Since virtually nothing that transpired at meetings between ACCD and Jay Peak officials was documented, and evidence doesn’t even exit that certain quarterly meetings were held at all, Vermonters can’t answer a basic question: why didn’t alarm bells ring for ACCD officials in those meetings in light of Judge Geoffrey Crawford’s biting summary (see quote at right).

- On September 27, 2012, Stenger directed the Governor of Vermont in a video in which the Governor asserted that the State audited its EB-5 projects. ACCD didn’t find out about it until June 2014. (See the direct quote to the right, and the full video below.) This means the promotional video was being shown to potential foreign investors for nearly two years with this misleading and confusing claim about the State’s due diligence.

Misleading and Confusing Claims That the State “Audited” EB-5 Projects

- On September 27, 2012, Stenger directed the Governor of Vermont in a video in which the Governor asserted that the State audited its EB-5 projects. ACCD didn’t find out about it until June 2014. (See the direct quote to the right, and the full video below.) This means the promotional video was being shown to potential foreign investors for nearly two years with this misleading and confusing claim about the State’s due diligence.

- The VRC did not print a retraction on its website to clarify that the State was not performing financial audits of EB-5 projects, but instead merely reviewing and signing off on project-related employment data. The ACCD Secretary stated that he did not think that posting a retraction would be effective, though it could have been done at almost no cost and would have reflected a high level of government accountability. The Secretary also stated that it would be the responsibility of Jay Peak to inform the investors, even though the Governor / State shared responsibility for the problem. In the end, the VRC did not direct Stenger to proactively inform investors or prospective investors that the Governor’s statement was incorrect.

More Missed Chances to Require Project Audits

- At the request of Jay Peak, the State updated MOUs for AnC Bio in October 2012 and for Burke in June 2013. Curiously, ACCD did not add audit provisions even though the State had leverage at the time.

State Oversight Improves When Original Structural Oversight Flaw is Corrected

- Until late December 2014, the VRC was located solely in the Agency of Commerce and Community Development, after which the Department of Financial Regulation (DFR) took over some of the VRC’s responsibilities. At this point, when the marketing/promotion duties were segregated from most regulatory duties, we observed a shift in the State’s efforts. Notably, DFR’s securities and fraud expertise resulted in more rigorous review of Jay Peak’s finances. Timing alone could explain some of the State’s more aggressive communications with Jay Peak (as the fraud grew, political pressure from unpaid contractors, for instance, was weighing on the minds of State officials). Nonetheless, ACCD’s admission that they did not have the necessary securities expertise to properly oversee the increasingly contentious relationship with Jay Peak speaks to the risk created when ACCD was made promoter and regulator.

These are just some examples of instances in which if State officials had made different decisions, events may have played out differently. Had appropriate systems been in place, with properly delineated roles and responsibilities between State agencies, addressing this historic fraud would not have been so dependent upon ad hoc decision-making by individual State officials.

Unfortunately, EB-5 is not the only program for which Vermont’s state government has assigned a state agency duties that present similar conflicts. Farm-based water quality combines both promotion and enforcement in the Agency of Agriculture, Food, and Markets. Economic development grants are frequently promoted, then reviewed and funded, by ACCD. There are likely other situations. While these conflicts do not mean that a fraud on the scale of EB-5 will occur, they represent the types of poor internal controls that make it more likely. We hope Vermont’s Executive and Legislative branches will dedicate themselves to reforming system flaws like these wherever they occur.

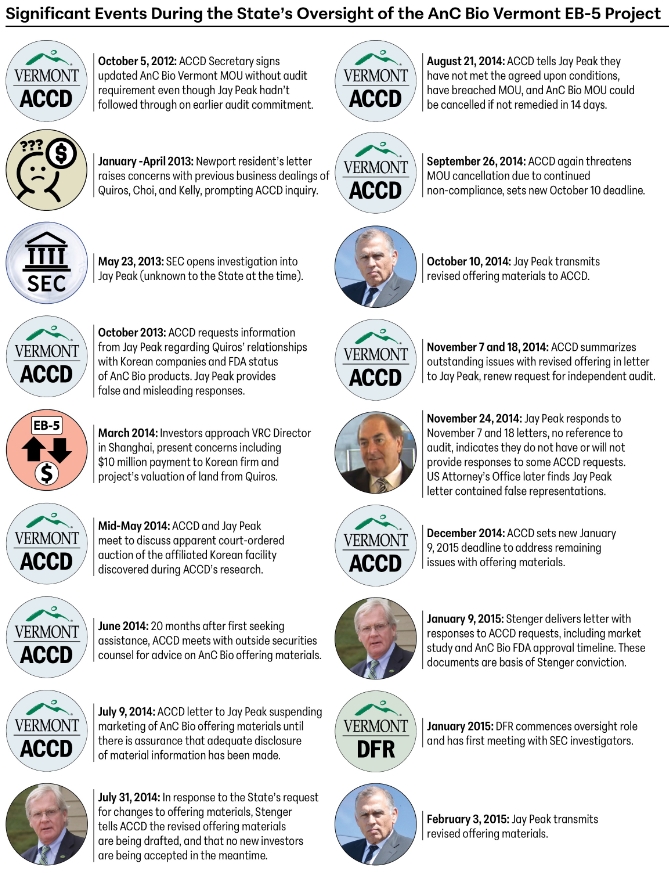

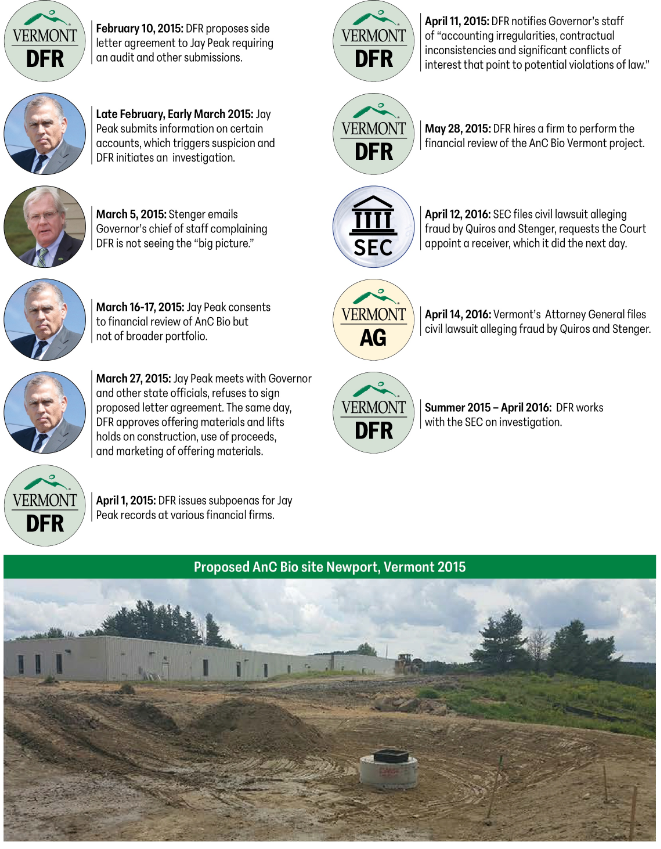

Significant Events During the State’s Oversight of the AnC Bio Vermont EB-5 Project

TIMELINE

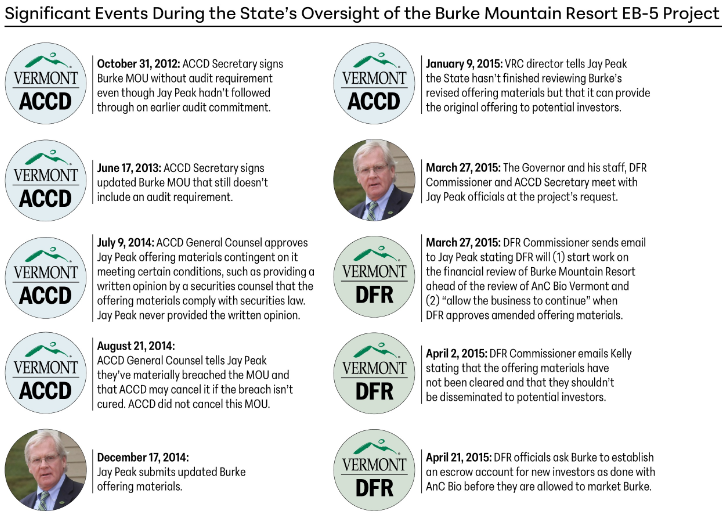

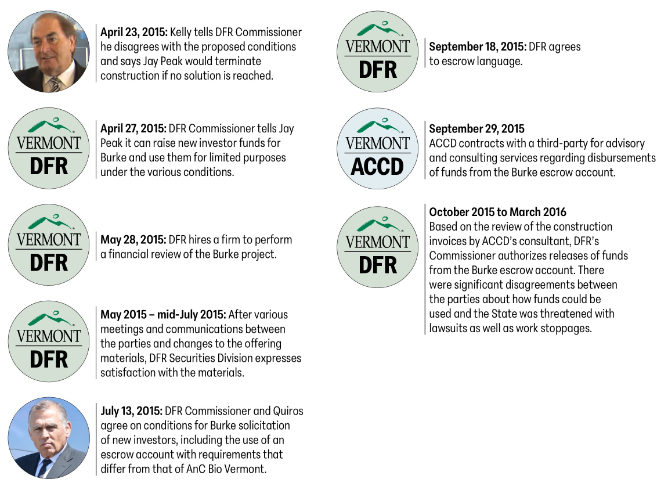

Significant Events During the State’s Oversight of the Burke Mountain Resort EB-5 Project

TIMELINE

To view the full report, please click here.