The Emergency Board: Governor Philip B. Scott, Chair; Senator Ann Cummings; Senator Jane Kitchel; Representative Diane Lanpher; and Representative Emilie Kornheiser, listen to Economists Tom Kavet and Jeff Carr present their consensus revenue report for fiscal years 2024 and 2025 Thursday afternoon at the State House. Screen shot.

by Timothy McQuiston, Vermont Business Magazine State economists still remain somewhat bullish on the Vermont tax revenue outlook despite what they anticipate to be a slowing of the US and state economies in the next few years and a quieting of the personal income tax, which has been robust the previous few years.

Jeff Carr for the Scott Administration (Economic & Policy Resources of Williston) and Tom Kavet for the Legislature (Kavet & Rockler of Williamstown) offered their revenue projections and economic analysis Thursday afternoon at the governor’s Ceremonial Office at the State House in Montpelier.

They present a consensus revenue forecast each January to the Emergency Board. The EBoard is comprised of the chairs of the four legislature money committees and the governor, as EBoard chair. The projections take into account current and future economic conditions, as they see it, and set tax revenue targets for the next two fiscal years. This helps the elected officials prepare their budgets. The revenue report is then revisited in July to update as needed.

Along with overall positive results, if less robust than previous years, the economists told the EBoard that they anticipate a “new normal” once the largesse of federal money plays out. There is still much on the books for infrastructure projects waiting to be constructed.

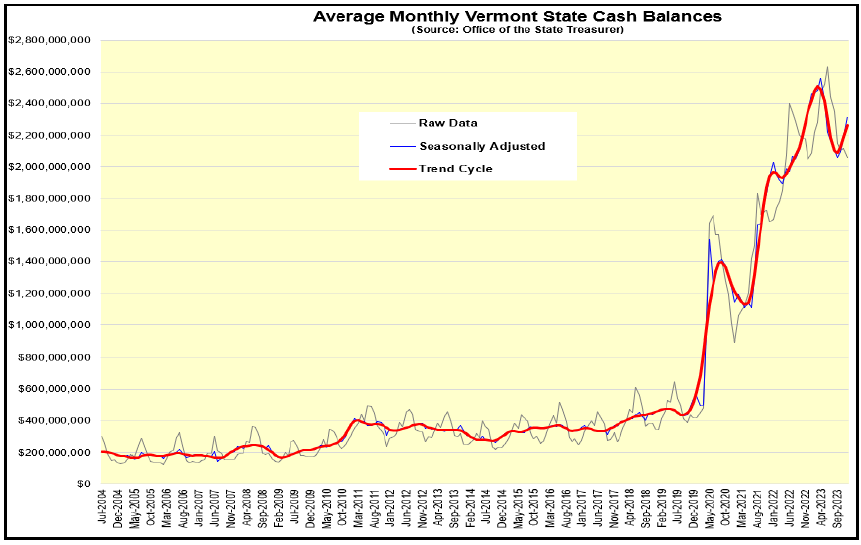

In addition to those projects, which should buoy the economy over the next few years, the state is sitting on an unprecedented amount of cash, as the result of that money-in-waiting, and because of those robust revenue numbers coming out of the COVID-19 pandemic. The state has nearly $3 billion in cash-on-hand, about 10 times its pre-pandemic, usual amount.

Much of that windfall, of course, was fueled by federal stimulus funds. It does allow State Treasurer Michael Pieciak to disperse a portion of that money ($50 million at the moment) in low-interest loans for development projects, most of which is going to the Vermont Housing Finance Agency. The VHFA is one of several housing organizations attempting to increase the state’s tight housing stock to make it more available and affordable.

Still, to achieve a positive new normal, it will require “skill and luck” in order to “stick the (soft) landing.”

Points of Interest

- The General Fund & Education Fund (non-property tax) are ahead of projections while the Transportation Fund, which has lagged for a number of years, has been adjusted downwards.

- The TFund has suffered from slow vehicle sales, EV purchases combined with higher fuel milage (though EV sales appear to be getting a pushback at the moment), and perhaps even because of lack of enforcement of registration and inspection requirements coming out of the COVID-19 pandemic.

- Net interest has become the state’s fourth largest GF revenue source as a huge increase in cash-on-hand has been met with higher interest rates. Those rates will, and therefore the return will lessen going forward (also in conjunction with the principal being spent), but it will still be higher than before COVID. For instance, in FY 2021 the net return was $900,000, FY24 it is $72.2 million and even out to 2029 it’s projected to be $19.9 million.

- Interest rates will remain “higher longer” not as high as they were recently but higher than the near zero rates from before and during the early part of COVID.

- While inflation has come down it remains higher than before COVID. Still, Carr doubts the Fed will raise interest rates to try and beat it down further. Kavet noted that one can understand consumer angst because inflation hit staples like energy and food hardest, while discretionary items like TVs and clothing have actually dropped in price in many cases.

- Personal wealth will remain high as housing values tend not to go down even if the economy slows. Also, stock values have rebounded the last few months.

- Homes values are still going up in places like Vermont, New Hampshire and Maine as people from urban areas come in a buy a second or third home for themselves.

- Listings for home sales is 75%-80% lower across the state now than five years ago. People can’t afford to move; there is no motivation to move because they’re sitting on low-interest home; there is no place to move for a lack of inventory and a lack of a place that is enough lower in price to turn a significant profit.

- There are also fewer people per unit than there used to be, which also exacerbates housing “deficiency.”

- In the past the has been an over-building in response to a housing shortage because of the lag time in building process and the need has lessened by the time the new units come online.

- The value of the federal money has lessened with higher interest rates and higher inflation, so the state will not be getting as big a bang for its buck in infrastructure projects.

- Vermont ranks low in foreign-born workers. Even other New England states have higher rates. Such workers also tend to be younger and a higher percentage enter the workforce. It will be difficult to grow the local labor force without them because of birth rates and the low rate of domestic migration.

- The Vermont Labor Force has bounced back but not all the way back to pre-COVID levels. Only Vermont and Rhode Island have not recovered all their labor force of the New England states, but Vermont is now close to 90 percent.

- One year ago, two-thirds of economists believed the US would in in recession by now. Now only one-third do.

- Jeff Carr: “There is no recession in this forecast.”

Jeff Carr said in his statement, in part: “Despite a litany of uncertainties and the ever-increasing toll that “higher for longer” interest rates have begun to take on the economy, this latest staff recommended consensus revenue forecast update calls for modest overall changes in state revenues—reflecting the still resilient performance of the economy, recent and impressive progress in bringing down inflation, and a level of unemployment in both U.S. sand state labor markets that remain near historic lows.”

Tom Kavet said in his statement: “In the teeth of the highest interest rates in more than two decades, calendar year 2023 exhibited surprising economic resilience. Job markets remained steadfast with unemployment below 4% for the entire year, extending a streak that started in February of 2022 and is now the longest such run in 53 years. Inflation receded from 2022 highs of more than 9% to between 3.0% and 3.7% in the second half of 2023, while the stock market set new records at the end of the year in the belief that the runway for the Fed’s hopeful “soft landing” is in sight. To be sure, many sectors of the economy have been downshifting, and revenues are still expected to decline in FY24, but if the Fed can lower interest rates sooner and faster than previously expected without inflation resuming, there may be less economic pain than anticipated.”

Reflecting the economy’s durability, total revenues for the three major funds forecast herein closed the first half of FY24 slightly above July projections (+1.7% and +$25.2M). The GFund was above targets by about 3%, as was the EFund at about 1%, while the TFund was about 6% below expectations. Accordingly, relatively minor adjustments to the three funds are recommended in this update, per the below chart.

“Despite widespread pessimism about the state of the economy, GDP growth has been stellar, unemployment is close to record lows (and for a near-record number of consecutive months), all while inflation has been receding,” Kavet said. “The next 12-18 months, however, will be a period of maximum stress, as the lagged effects of the steep monetary tightening hit the economy and accrued savings from the pandemic continue to dwindle. Although our baseline forecast still does not assume a recession will occur during this period, the economy will slow substantially, along with State revenues. The “soft landing” runway may be in sight, but sticking the landing still carries considerable downside risks and will require both skill and luck to achieve.”

Jeff Carr Presentation

Updated Staff Consensus Forecast Update Recommendations for Fiscal Year 2024 and 2026 along with Consensus Fiscal Planning Revenue Estimates for Fiscal Year 2027 through Fiscal Year 2029.

Despite a litany of uncertainties and the ever-increasing toll that “higher for longer” interest rates have begun to take on the economy, this latest staff recommended consensus revenue forecast update calls for modest overall changes in state revenues—reflecting the still resilient performance of the economy, recent and impressive progress in bringing down inflation, and a level of unemployment in both U.S. sand state labor markets that remain near historic lows.

- Total state G-Fund, E-Fund and T-Fund (including TIB) revenues overall across the first half of fiscal year 2024 also displayed some resiliency against the backdrop of the flooding event in mid-July, finishing the month of December at +$27.0 million (or +1.8%) ahead of cumulative consensus expectations of $1.522 billion (As a federal aid minimum state allocation recipient).

- That generally positive revenue for the first half of fiscal year 2024 was a reflection of generally upbeat receipts in the Personal Income Tax (at +$18.6 million or +3.6% on cumulative consensus first half expectations of $523.9 million), strong receipts in Net Interest revenues (at a combined +$22.2 million or +154.9% in combined G-Fund and E-Fund Net Interest revenues through December above last fiscal year’s first half combined G-Fund and E-Fund “Net Interest" revenue total) and resiliency in first half Sales and Use Tax receipts activity (at +$5.6 million or +1.9% versus cumulative consensus expectations of $302.6 million).

- This occurred despite the sluggish performance by the Corporate Income Tax over the first half (at -$7.7 million or -7.3% below cumulative consensus expectations of $105.3 million over the July to December timeframe)—against the significantly elevated level of receipts that were forecasted last July.

- First half receipts also were below consensus expectations for the T-Fund’s Motor Vehicle Purchase and Use Tax (at a combined -$4.0 million or -5.5% on combined first half consensus expectations of $73.3 million)—reflecting high borrowing costs, the still scarce amount of supply of vehicles, and the negative impact of the labor unrest in the U.S. auto sector during the first half. That more sluggish rate of vehicle acquisition spilled over into receipts activity in the T-Fund’s Motor Vehicle Fees category (at -$3.1 million or -7.2% on consensus expectations of $43.0 million–which remained sluggish in the aftermath of the pandemic.

Over the near-term time horizon, current law forecast includes a small consensus revenue forecast upgrade for State revenues over the fiscal year 2024 through 2026 timeframe—totaling $56.6 million or 0.9% on $6.4 billion is expected G-Fund revenues over the fiscal year 2024 through 2026 (see Table 1).

- The forecast changes reflect technical updates and refinements in estimating the amount of revenues flowing from the G-Fund’s Net Interest component and an updated forecast for the Corporate Income Tax.

- The updated consensus forecast for the Personal Income Tax over the fiscal year 2024-26 time frame includes the final two years of an unusual three-year, consecutive year-over-year decline in net receipts—reflecting the unusual post-pandemic economic circumstances and updated consensus expectations for a slowing in the national and state economies over the next 12 to 18 months.

- The G-Fund consensus forecast upgrade also gets a small assist from upgraded consensus expectations of just under +$6.0 million for G-Fund Health Care revenues.

- For the T-Fund, the consensus forecast update changes reflect the recent sluggishness of T-Fund revenues against the backdrop of the various Fee changes passed during the 2023 Session of the Vermont General Assembly (at -$18.9 million or -2.0% of $934.9 million over the fiscal year 2024-26 period).

- The updated consensus forecast for the E-Fund includes the combination of the resilient performance of the E-Fund’s Sales and Use Tax component, the strong recent performance of the Lottery Transfer component (with its recent record jackpots), and the E-Fund’s portion of the significantly higher Net Interest revenues associated with higher interest rates and the State’s more aggressive cash management practices.

▪ For the outyear fiscal planning period years for fiscal years 2027 through 2028, the forecast upgrade amounts are expected to be significantly smaller in dollar value. Those out-year forecast changes also reflect the first two years beyond the outyear impacts of the unprecedented levels of largely deficit-financed federal COVID pandemic assistance and infrastructure spending, and the initial phase of the transition of State revenue collections back to relying on the fundamentals of the Vermont economy.

- For T-Fund TIB revenue sources, the staff recommended consensus forecast recommends a revenue forecast downgrade based on the sensitivity of these TIB revenue sources to declining fuel consumption and upcoming changes in energy-fuel prices.

▪ On a fiscal year to fiscal year basis, staff recommends that this updated January 2024 consensus revenue forecast for expected revenues “Available to the General Fund” of +$29.3 million for fiscal year 2024, +$10.2 million for fiscal year 2025, and +$17.1 million in expected revenues for fiscal year 2026.

- For the years beyond fiscal year 2026 (covering the additional fiscal policy planning time frame of fiscal years 2027 and 2028), the staff recommends an increase of +$9.2 million for fiscal year 2027 and a +$10.5 million consensus forecast upgrade of revenues “Available to the General Fund” for fiscal year 2028.

- For fiscal year 2029, as the final year of the fiscal planning period added to this forecast, staff recommends a consensus forecast of $2,443.1 million.

▪ For expected revenues “Available to the Education Fund,” staff recommends an increase of +$9.7 million in fiscal year 2024, a +$9.3 million consensus forecast upgrade for fiscal year 2025, and a +$6.8 million staff recommended forecast upgrade for expected E-Fund revenues for fiscal year 2026.

- For the years beyond fiscal year 2026 (covering the additional fiscal policy planning time frame of fiscal years 2027 and 2028), the staff recommends revenues “Available to the Education Fund” of +$4.4 million in fiscal year 2027 and +$2.6 million for fiscal year 2028.

- For fiscal year 2029, as the final year of the fiscal planning period added to this forecast, staff recommends a consensus forecast of $852.4 million.

▪ For the T-Fund, staff recommends a -$5.1 million forecast downgrade in revenues ”Available to the Transportation Fund” for fiscal year 2024, another -$6.4 million forecast downgrade for fiscal year 2025, and -$7.4 million forecast downgrade for fiscal year 2026—which are a reflection of the more sluggish than anticipated performance by T-Fund revenues overall over the first half of fiscal year 2024 and the continued “higher for longer” level of interest rates and associated increase in financing costs that have negatively impacted vehicle purchase and leasing activity despite the Fee increases passed during the 2023 session of the Vermont General Assembly.

- For the additional planning out-years covering the 2027-2028 period, staff recommends consensus forecast upgrades of “Available to the T-Fund” revenues of -$7.2 million for fiscal year 2027 and a staff recommended forecast downgrade of “Available to the T-Fund” revenues of -$6.1 million for fiscal year 2028.

- For fiscal year 2029, as the final year of the fiscal planning period added to this forecast, staff recommends a consensus forecast of “Available to the T-Fund” revenues of $334.1million on a current law basis—well below the previously forecasted trend for T-Fund revenues during the out-year fiscal planning period.

▪ All of the above itemized forecasted numbers are current law numbers and include expectations of current law Health Care Revenues that are allocated to the GFund— including the sunset of the Home Health Care Provider Tax that went into effect on July 1, 2023.

- Excluding Health Care revenues from the above staff recommended change numbers results a staff recommended forecast upgrade of +$28.8 million in fiscal year 2024, a +$8.2 million forecast upgrade in fiscal year 2025, and a staff recommended +$13.7 million forecast upgrade for fiscal year 2026 versus consensus expectations last July.

- For the out-years of the fiscal years 2027 through 2028, the updated staff recommended consensus forecast expectations call for a +$5.0 million increase for fiscal year 2027 and a +$6.7 million increase in the consensus revenue forecast for fiscal year 2028.

- For fiscal year 2029 as the final year of the fiscal planning period, this staff recommended forecast calls for a total of $355.7 million in G-Fund Health Care Revenues “Available to the General Fund” during that fiscal year.

▪ The staff recommended forecast for revenues T-Fund TIB revenues includes a combined TIB fund forecast upgrade of +$0.4 million for fiscal year 2024, a staff recommended forecast downgrade of -$0.6 million for fiscal year 2025, and a staff recommended forecast downgrade of -$0.7 million for fiscal year 2026.

- For the fiscal planning period for fiscal years 2027 through 2028, staff recommends forecast downgrades of -$0.9 million for fiscal year 2027 and -$1.0 million for fiscal year 2028 relative to the July 2023 revenue forecast.

- For fiscal year 2029, as the final year of the fiscal planning period added to this forecast update, staff recommends a $17.3 million consensus forecast.

- All of the T-Fund TIB consensus forecast recommendations are on a current law basis and reflect consensus expectations for the changing energy price situation, fuel consumption and commercial vehicle trips for Diesel Tax TIB.

▪ The updated July 2023 staff recommended consensus revenue forecast includes both an updated consensus economic forecast (see the section on the updated consensus economic forecast below) for the period and extends from the current 2024 calendar year through calendar year 2029 as developed during December of calenda year 2023 (or at the mid-point of fiscal year 2024).

- This staff recommended consensus revenue forecast update includes all of the best available information regarding the still on-going economic and fiscal legacy effects of the COVID pandemic as they currently are understood and still are evolving, the state’s recovery from the flooding event last July (and the second flooding event in mid-December, which turned out to be somewhat less impactful on the level and month-to-month profile of revenue receipts than was initially expected), and the on-going transition of the economy back to its underlying fundamentals—again, likely as part an emerging ”new normal” in this regard, and accounts for all tax and fee changes as passed by the 2023 Vermont General Assembly.

▪ The staff recommended consensus forecast update also includes full consideration of the underlying trends and the actual collections data through the first half of fiscal year 2024 (see Table 2)—with emphasis on recent trends in underlying Personal Income Tax , Corporate Income Tax, and state consumption tax receipts activity, and with technical adjustments to and continuing refinements that are always made to refine forecasting the forecasting methodologies employed for GFund and E-Fund Net Interest revenues.

- The updated Net Interest revenue forecast for the G-Fund and E-Fund also reflects expectations for “higher for longer” levels of interest rates the State’s stepped-up cash management practices associated with its historically high cash bank balances that remain “on hand” (See the chart from the Federal Reserve Staff on the current and the expected future level of the U.S. Federal Funds Interest Rate and the seasonally-adjusted path of Average Monthly Vermont State Cash Balances following Table 2).

- That includes the expectation that the State will spend down at least part of the unprecedented level of federal funds received over the last several years— a significant portion of which remain in the spending pipeline—along with the generally increasing interest-earning cash balances at banks as overall revenue receipts have continued to grow with the economy over time.

▪ Within the above-described economic-revenue environment, the updated staff recommended consensus forecast updates for the fiscal year 2024 through 2026 timeframe for G-Fund, T-Fund, E-Fund, and T-Fund TIB revenues includes the following dollar levels (See Table 2):

- For the G-Fund overall on a current law basis, the staff recommends an updated consensus forecast of $2,131.4 million in “Available to the G-Fund” revenues for fiscal year 2024, an updated staff recommended consensus forecast of $2,113.5 million in “Available to the G-Fund” revenues for fiscal year 2025, and a staff recommended $2,191.0 million in “Available to the GFund” revenues for fiscal year 2026.

- For the fiscal planning out-years covering the fiscal year 2027-2029 period, this consensus revenue forecast update recommends “Available to the G-Fund” revenue amounts of $2,272.3 million for fiscal year 2027, $2,360.2 million for fiscal year 2028, and a forecast of $2,443.1 million for fiscal year 2029.

▪ With respect to the G-Fund’s Health Care revenues portion of the “Available to the G-Fund” on a current law basis, the staff recommends an updated consensus forecast of $322.0 million in fiscal year 2024, an updated consensus forecast of $332.0 million for fiscal year 2025, and an updated consensus G-Fund Health Care revenue forecast of $337.5 million for fiscal year 2026 (see Table Above).

- The staff also recommends an updated forecast of $343.3 million for Health Care revenues “Available to the General Fund” for the fiscal year 2027, an updated forecast of $349.4 million for fiscal year 2028, and a consensus forecast of $355.7 million for fiscal year 2029—or for the three-year fiscal planning period associated with the consensus forecast update.

▪ For the T-Fund, staff recommends an updated consensus forecast of “Available to the T-Fund” revenues of $299.4 million for fiscal year 2024, and an updated staff recommended consensus forecast of $315.7 million in “Available to the T-Fund” revenues for fiscal year 2025, and a staff recommended $319.8 million “Available to the T-Fund” revenues total for fiscal year 2026 on a current law basis.

- For the fiscal planning out-years covering the 2027-2029 fiscal year period, staff recommends a consensus forecast of “Available to the T-Fund” revenues of $324.9 million for fiscal year 2027, a staff recommended forecast of “Available to the T-Fund” revenues of $330.2 million for fiscal year 2028, and a staff recommended forecast of “Available to the T-Fund” revenues of $334.1 million for fiscal year 2029, on a current law basis.

▪ For the T-Fund TIB revenues overall, staff recommends an updated staff recommended consensus forecast of $19.2 million for fiscal year 2024, and an updated staff recommended consensus forecast of $18.2 million in fiscal year 2025, and a revised staff recommended consensus forecast update of $17.3 million in TFund TIB revenues for fiscal year 2026 on a current law basis.

- For the fiscal planning out-years covering the three-year 2027-2029 fiscal year period, staff recommends a consensus forecast of T-Fund TIB revenues of $17.2 million for fiscal year 2027, a staff recommended forecast of T-Fund TIB revenues of $17.2 million for fiscal year 2028, and a forecast of T-Fund TIB revenues of $17.3 million for fiscal year 2029, on a current law basis.

▪ For the E-Fund, staff recommends an updated consensus forecast of $745.9 million in “Available to the E-Fund” revenues for fiscal year 2024, an updated $758.8 million for fiscal year 2025, and an updated staff recommended consensus forecast of $778.6 million in “Available to the E-Fund” revenues for fiscal year 2026, on a current law basis.

- For the fiscal planning out-years covering the 2027-2029 fiscal year period, staff recommends a consensus forecast of “Available to the E-Fund” revenues of $801.9 million for fiscal year 2027, a staff recommended forecast of “Available to the E-Fund” revenues of $827.7 million for fiscal year 2028, and a staff recommended forecast of $852.4 million for fiscal year 2029.