Debt Proceeds Exceed VEPC Approved Cap by $4.6 Million, Interest Costs Nearly $8 Million More than Estimated, TIF District Owes State Education Fund $95,363, and City Owes TIF District $259,331

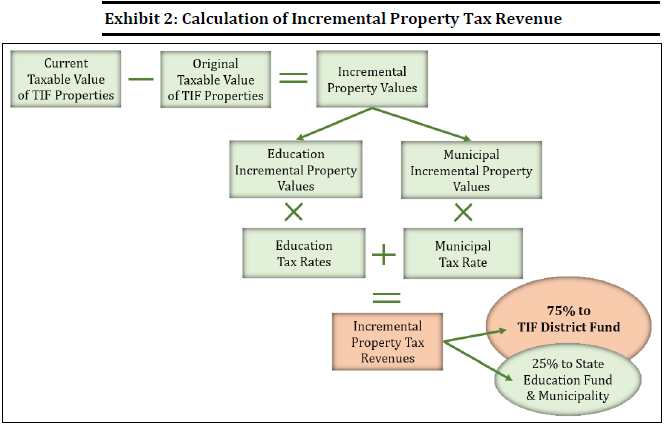

by Timothy McQuiston, Vermont Business Magazine State Auditor Doug Hoffer released a new audit report today of Burlington’s Downtown Tax Increment Financing (TIF) district. TIF districts allow municipalities to designate an area for public infrastructure improvements, incur debt to pay for the work, and use a portion of the area’s property tax revenue growth, which would normally go to the Education Fund and the municipality, to pay back the debt. Since 2017, Burlington has spent nearly $8 million of bond proceeds on improvement projects (such as the reconstruction of portions of Main St. and St. Paul St.) and more than $4 million of tax increment for debt payments and related costs (district administrative and operational costs).

Burlington Mayor Miro Weinberger accepted that the city needed to make some adjustments, which he said they did, but he rejected the conclusion of the city's "missteps" of how the city financed the bond payments and that the city exceeded its regulatory funding cap.

Hoffer has frequently taken issue with the TIF process and implementation, as being too complex. He has also taken issue with using property tax money for development purposes, even as he acknowledges that outcomes have been welcomed by the municipalities.

Hoffer has also just sued Vermont Attorney General Charity Clark, another independently elected constitutional officer, over informal opinions related to the Burlington TIF. Clark responded in a VtDigger article that they do not do such things in any case and that the suit is a literal waste of time and money.

Hoffer said that the legal wrangling over that is now "moot" with the release of this Burlington TIF audit.

Of this audit, he said: “While we were pleased to see that the City adopted some of our earlier recommendations to improve their financial management, the Downtown TIF audit shows once again that even Vermont’s largest municipality struggles with the complexity of the TIF program. The audit found numerous consequential mistakes, and revealed interest payment levels that are considerably higher than what voters had been told to expect.”

Key findings of the audit include:

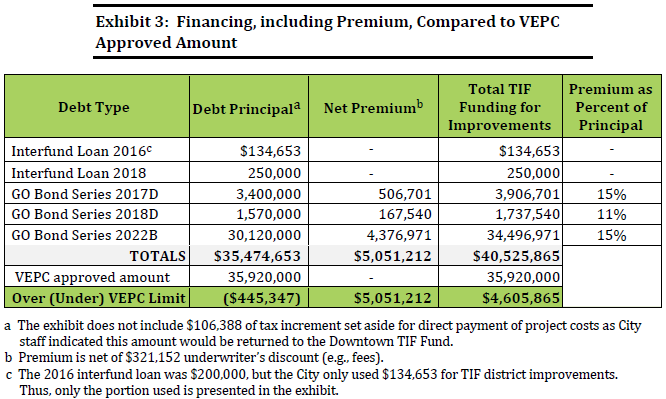

- The City claims it was following customary municipal borrowing practices but received $4,605,865 more from its bond issuances than the amount approved by the Vermont Economic Progress Council (VEPC) for investment in infrastructure improvements in the TIF district. VEPC approval is required to limit risk and cap the City’s use of the Education Fund to support local economic development projects.

- The estimated interest cost for the bond issued by the City in August 2022 is nearly $12 million. The TIF Financing Plan approved by VEPC included $4 million of interest, which is what the municipal voters were told to expect.

- In failing to request VEPC’s approval for these changes to the TIF Financing Plan, the City bypassed a control on limiting increased costs of debt service being borne by the State Education Fund. Because education funding is a state-wide system where all property taxpayers share the burden of school spending, the diversion of additional tax increment to Burlington to cover the increased cost will be made up by taxpayers in non-TIF areas of the State.

- The City failed to consistently contribute a Champlain College development fee into the Downtown TIF Fund, resulting in a total omission of $1,040,000. As a result, VEPC has reduced the percent of education tax increment that the City may keep from 75 percent to 69 percent for the remaining 13 years of the tax increment retention period.

- A series of errors resulted in the City owing $95,363 of TIF funds to the state Education Fund, and the City’s General Fund owing $259,331 to the Downtown TIF Fund.

- From FY2017 to FY2023, the City funded more than $8 million of various improvement projects and used about $4 million of tax increment to pay for debt and administrative and operational costs of the TIF district. Auditors concluded these were eligible uses.

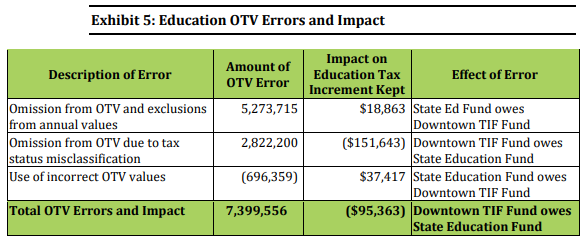

Education Tax Increment Errors

From FY2017 to FY2023 the City kept $5,304,459 education tax increment in the Downtown TIF Fund, but the City made several errors that resulted in retention of incorrect education tax increment. The errors included parcel omissions from the TIF parcel listings, affecting both original taxable value (OTV) and current values, and the use of incorrect OTV for four parcels that are in the TIF district. These errors resulted in the Downtown TIF Fund overpaying $56,280 to the State Education Fund; however, such overpayment was offset by the underpayment of $151,643 to the State Education Funds due to a tax misclassification of a property. Cumulatively, the City kept $95,363 of education tax increment in the Downtown TIF Fund that should have been sent to the State Education Fund. Thus, the Downtown TIF Fund owes this amount to the State Education Fund.

Exhibit 5 shows the impact and effect of the errors on education tax increment.

Parcels Were Omitted from the Education OTV and Excluded from TIF Education Current Values

The City omitted two parcels from the Downtown TIF District parcel listing submitted to VEPC with the 2011 TIF district application and the subsequent OTV certification. Maps of the Downtown TIF District filed with VEPC and the Vermont Department of Taxes Property Valuation and Review (PVR) division consistently showed that these two parcels were within the boundaries of the TIF district, but the parcels weren’t drawn on the maps. This may explain why the required OTV certification process, completed in 2019 by the City, VEPC, and PVR did not identify these omissions. Omission of these parcels resulted in the understatement of OTV by $5,273,715, as well as the omission of their respective current values. This adjustment is required for the education and municipal OTVs and should be effective at the same time as the certified OTV in FY2020.

Because the properties were omitted, the associated incremental value was not captured in the City’s tax increment calculation.

Hoffer said: “As I have said before, the question is not whether we should support municipal infrastructure investments, but rather how to do it at the lowest cost, with the least unnecessary complexity, and resulting in the broadest benefit to communities across Vermont. The substantial interest costs associated with this TIF district demand a serious discussion of alternative methods of financing local projects. As for complexity, even Vermont’s largest municipality struggles to administer its TIFs.

"It can be tempting to gloss over the expensive nature of TIF districts because the projects they finance are so welcome, but taxpayers deserve these projects to be delivered at the lowest price.”

In 2013, the Legislature required the Auditor’s Office to conduct a series of audits of each TIF district in Vermont to prevent errors and mismanagement which could negatively impact the state’s Education Fund. Burlington has two TIF districts. This audit focused only on the Downtown TIF. An audit of the City’s Waterfront TIF was completed in January 2023.

Hoffer said: “One of the key findings of the audit is that the City exceeded the amount of debt proceeds that had been approved by VEPC. These approvals were built into the process for a reason – to ensure projects are not too risky, and to limit the liability of taxpayers statewide who are asked to subsidize TIFs through the Education Fund. These approvals have to mean something both for fairness and accountability.”

Source: 1.16.2024. MONTPELIER, VT – State Auditor