Jeff Carr, far left, and Tom Kavet explain their consensus revenue report to the Emergency Board, as Governor Scott listens. To watch the full presentation, click on image above, which begins at about the 9:20 mark. Governor's Ceremonial Office, State House, January 17, 2023. Screen grab.

by Timothy McQuiston, Vermont Business Magazine Economists for the Legislature and Administration met with Governor Scott and key lawmakers today to present a positive and nervous report on the state of Vermont’s tax revenues. Economists Jeff Carr (Administration) and Tom Kavet (Legislature) said in their consensus revenue reports that tax proceeds are doing well and that they have upgraded their projections for the current fiscal year (2023) and for next year. The General Fund, driven by personal and corporate taxes, should be especially strong.

None of this is much of a surprise. Nor is it a surprise that the economists, and everyone else, are nervous that a recession could be just a little way down the road, as the Federal Reserve Bank keeps raising interest rates.

Carr and Kavet call the eventual decline "the great unwinding," as revenues slow over the next couple years.

The Fed has been raising interest rates aggressively for about the last year in order to stem the tide of inflation, with only modest success, if any. Americans are still sitting on significant wealth, federal stimulus money is still circulating, and a tight workforce has driven up wages, all of which has led to more spending and more tax revenues.

In addition, with the upwards of $3 billion having come to Vermont in many ways, much of that is still playing out and will continue to play out. Earmarks for things like infrastructure projects and affordable housing take time to go through the process.

Along with the personal and corporate incomes taxes, the consumption taxes of sales & use and rooms & meals continue to show strength, indicative of consumer cash and consumer confidence.

These consumption taxes have pushed expectations for the Education Fund up as well, if not quite to the level of the GF.

State tax revenues exceed expectations again

Meanwhile, the sluggish Transportation Fund continues to be sluggish, as the fuel taxes underwhelm and car sales lag. But even the TFund will still do what it’s been doing and stay near the target lines.

As for the national economy, Carr and Kavet noted that the majority of economists believe the economy will fall into recession in the next year and not achieve the "soft landing" the Federal Reserve Bank had hoped for when they started raising interest rates early last year. The Fed had hoped to curb inflation by now by slowing the economy with these interest rate hikes, something that has only marginally happened, which has resulted in them continuing to raise rates.

The Fed also has become more pessimistic recently, Carr said, as inflation persists.

Carr said, "The Fed was late to the party, so to speak. They had this notion that it was transitory, and everything, and it turned out it that became more widespread and more entrenched than they thought it would. They're fighting hard to maintain credibility. Every single time the markets start talking about how they may stop the interest rate increases, they actually went from 3/4 to a half in December. And every time the markets react positively, you get a whole bunch of hawkish talk that we're not done yet, we're not going to give up, and all those kinds of things. And so the point is, 2/3 of the economists that think we're going to have a recession believe the Fed's going to overdo it. And if the Fed overdoes things, it tends to do things when it's tight like it is now. So the prospects of a general economic downturn, even if it turns out to be mild and relatively short, still are more significant than the forecasts that we have because we have a harder soft landing."

In response to how they would even define a recession, Kavet said, "Unemployment would have to be substantially higher than it is now."

Vermont's unemployment rate continues to run near its historic low and the November 2022 rate of 2.5 percent (the most recent available) is fifth lowest in the nation.

"I don't think you're going to get a lot of relief on the recession side," Kavet said, "unless things slow more than they do."

The Vermont Emergency Board (E-Board) is composed of Governor Scott and the chairpersons of the Legislature’s four “money committees” (Senate Appropriations, Jane Kitchel; Senate Finance, Ann Cummings; House Appropriations, Diane Lanpher; and House Ways & Means, Emilie Kornheiser).

The following is a largely verbatim presentation of Kavet’s report.

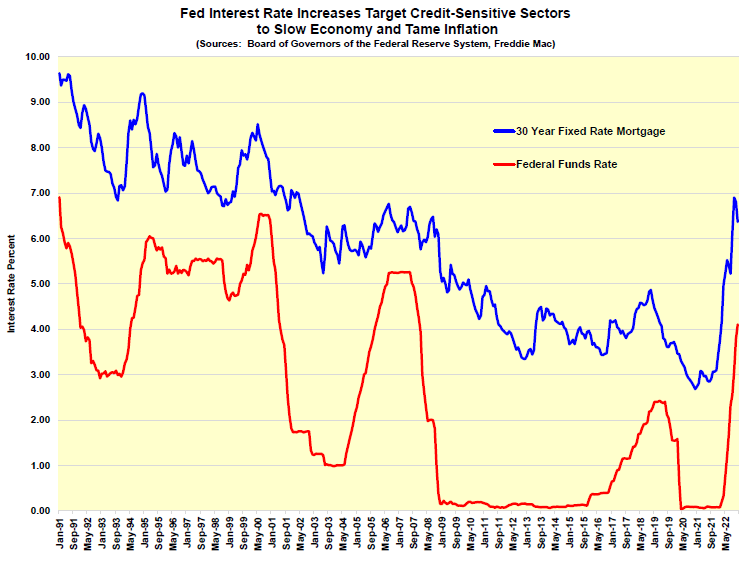

With countervailing currents still contesting the direction of the economy, resilient growth is prevailing to date. The two opposing currents now at play consist of the stimulative effects of unprecedented recent federal spending and, more recently, monetary policy designed to slow the economy in the face of the highest inflation experienced in more than 40 years. Steep interest rate hikes beginning early last year have driven the effective federal funds rate above 4%, pushing 30-year mortgages close to 7%. Thus far, the effects of these rate hikes have been blunted by the massive savings and net worth built up during the past three years, keeping consumers spending, corporate coffers flush and tax revenues rolling in. It has also exacerbated inflation, which will likely cause even further rate hikes, elevating the risk of a deeper downturn in FY24. Despite our baseline forecast for no recession this year, we do anticipate a significant slowing of the economy in FY24.

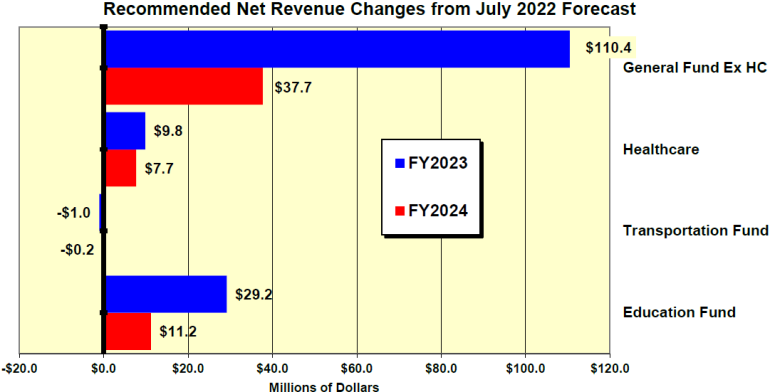

In the meantime, FY23 is expected to be considerably stronger than projected in July, resulting in revenue adjustments in this forecast that are mostly positive – especially in the large Personal and Corporate Income taxes in the General Fund. Lower gasoline prices and continued lower vehicle miles travelled will contribute to a slight negative adjustment in the Transportation Fund. Meanwhile, buoyant consumer spending and higher inflation will boost revenues in the large consumption taxes, benefiting the Education Fund.

Epidemiological Update

• Despite no longer being the dominant influence on the economy, the pandemic is still present and its lingering effects remind us that it remains important to consider in developing State economic and revenue forecasts. The current variant now most prevalent in the Northeastern U.S. is an Omicron subvariant labelled XBB.1.5, which is now responsible for more than 70% of the cases in the region and about 28% of cases in the rest of the nation. It is the most transmissible variant detected to date, but is currently not expected to be as lethal or economically impactful as the original Omicron spike experienced about a year ago.

• There are, however, persistent effects of the pandemic still impacting State revenues, including a greater acceptance and prevalence of remote work, reduced local travel, elevated asset and other prices, reduced life expectancy and continued supply chain issues from global variations in pandemic management (especially Chinese) and related health and economic effects. These have complex and changing State economic impacts, but have thus far reduced the labor force via earlier retirement, illness and death, increased personal income and population via greater in-migration and remote work options, increased revenue flows from high asset prices, wage growth and inflation, and limited revenue from supply bottlenecks in revenue categories such as the Motor Vehicle Purchase and Use tax. To date, it has also reduced State employment in leisure and hospitality businesses, healthcare, education, retail trade and government, while professional and other service sectors have expanded, while construction employment has held steady.

Economic, Fiscal and Monetary Policy Update

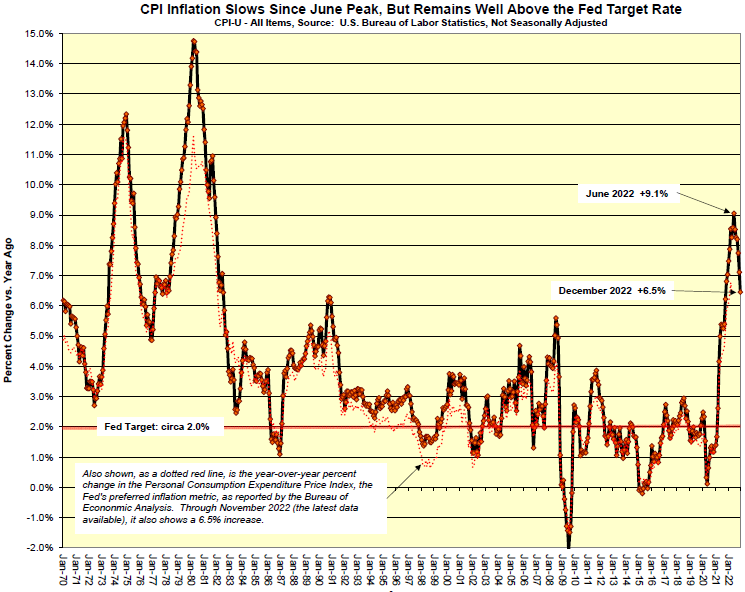

• The current economy, with solid wage gains, low unemployment, robust business profitability, and vast and widespread household wealth growth, would be an economic policy dream - except for an accompanying severe spike in inflation. After averaging only 2.1% annual inflation for the preceding 24 years, in April of 2021, the CPI began to register year-over-year growth that was double, then triple and by April of 2022, was quadruple this rate (8.3%). The Fed initially dismissed the rise as “transitory,” correctly attributing much of the increase in supply-chain problems related to the pandemic, however, as the price increases continued to escalate, they risked becoming persistent and debilitating.

• The Fed reacted with an historically rapid escalation of interest rates and quantitative tightening, in an attempt to slow the economy and lower demand to a point more closely balanced with supply. The main problems with this are that such policy moves are difficult to precisely calibrate to a desired effect, there are complex lags between such policy changes and their desired effects, and the policies are incapable of addressing many of the pandemic-related issues - and military conflicts - causing supply constraints.

• The Fed’s goal is a broad economic slowdown without a full-blown recession – a so-called “soft-landing” - but this is a difficult needle to thread. Many consider it improbable. This skepticism was voiced by former Treasury Secretary, Director of the National Economic Council, Harvard President and Economics Professor, Lawrence Summers, during an interview on Bloomberg’s Wall Street Week in which he warned:

“It’s much harder than many people think to achieve a soft landing, because there are all these mechanisms that kick in. At a certain point, consumers run out of their savings, and then you have a Wile E. Coyote kind of moment where consumption falls off. …Once you get into a negative situation, there’s an avalanche aspect. And I think we have a real risk that that’s going to happen at some point.”

• The revenue categories most susceptible to a Wile E. Coyote-style moment are some of the strongest current performers, notably Corporate and Personal Income taxes. Because they are largely backwards looking, in a downturn, both current liabilities and prior payments for estimated liabilities can evaporate, and result in widespread refunding that amplifies the decline. Consumption and related tax revenues may also decline in tandem, but with far less volatility.

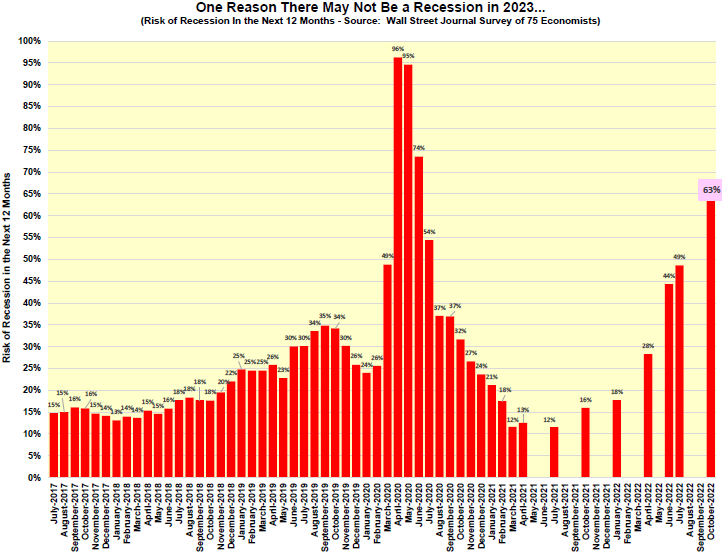

• Other “soft-landing” skeptics include 63% of the 75 economists regularly surveyed by the Wall Street Journal, who consider a recession in 2023 to be likely. Of course. when 63% of economists agree on anything, many will doubt its verisimilitude…

• Headline CPI inflation has slowed steadily since it’s 9.1% peak in June of last year, dropping to 6.5% in December, however, it is still well above the Fed’s 2% target – and the next four percentage points may be harder to achieve. There are several reasons for this: One is that wage gains tend to lag sustained CPI price increases. Salaries are customarily reviewed annually and contract employees may have multi-year contracts. So, unless an employee threatens to quit or is a part of a union pressing for cost-of-living adjustments, any wage increase will be backward looking and attempt to recoup prior purchasing power losses and protect against anticipated future price increases. Thus, considerable upward wage pressures are still likely to be felt for much of 2023, especially if labor markets remain as tight as they are now. Another reason is that many pricing disruptions stem from geo-political events like the Russian invasion of Ukraine and are not influenced by U.S. monetary policy. Last year’s energy price surge was largely influenced by the invasion and it contributed significantly to the peak June CPI reading, but could not have been meaningfully affected by any Fed policy move. Similarly, another pandemic – avian flu, which is decimating U.S. laying hen populations – underlies the single largest increase in any CPI component, eggs (up 75% over pre-pandemic prices through December of 2022) and cannot be affected by Fed policy.

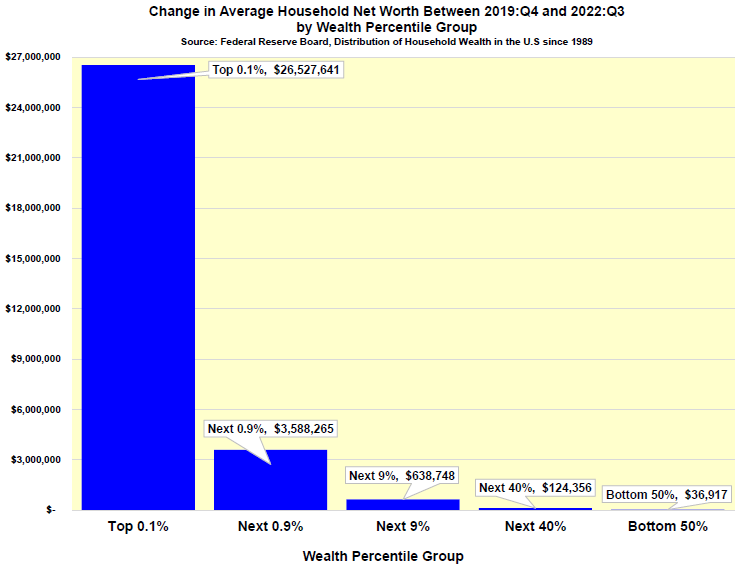

• Offsetting the intentions of the Fed to slow the economy is a massive level of savings and other retained wealth, and continued “on-the-ground” spending from prior federal stimulus programs. Both household and business balance sheets remain healthy as reflected in the net worth statistics presented in the last economic and revenue forecast, and updated with the most recent data (the third quarter of 2022) in the below table.

• These data show a decline in total net worth in recent quarters, but still reflect large gains among all net worth percentile groups. It uses an earlier reference quarter for pre-pandemic comparison since the first quarter of 2020 had some pandemic-related impacts and was lower than the fourth quarter of 2019. For the first time, this dataset includes a breakout that adds the top 0.1% of net worth, showing the outsized gains among the wealthiest households – as well as the large percentage gains in the lowest percentile group – the bottom 50%. While the net worth of the average household in the top 0.1% rose by more than $26 million, +25.4%, the average household net worth of the bottom 50% rose by $36,917, +111.6%, largely due to rapidly increasing home prices.

• This wealth, including liquid assets, such as deposit accounts at banks, is one of the reasons the Fed’s efforts to slow the economy have been blunted and consumer and business spending has remained intact. The depository base for the Vermont Bank Franchise tax, which is a backward-looking 12-month deposit average, implies a gain of more than $6 billion from pre-pandemic levels to the last quarter of 2022, a 46.7% increase. This represents more than 15% of Vermont’s total annual GDP, as estimated in 2023.

• A spate of recent layoffs at tech firms has raised concerns of an impending downturn, but these seem to be mostly the result of over-hiring and postpandemic shifts in consumer demand. Nationally, quit rates have receded from their all-time highs, reached about a year ago, but are still 40% above their 20- year pre-pandemic average. The aggregate number of U.S. layoffs and discharges are up slightly but are also about 30% below 20-year pre-pandemic levels, and job openings still greatly exceed the number of unemployed persons.

• The gap between job openings and the number of unemployed persons is a stark reflection of current labor market tightness. The yawning national and Vermont gaps show little indication of narrowing in the months since the Fed’s interest rate increases began. There are currently three job openings for every unemployed worker in Vermont, well above the U.S. ratio of about two to one.

• Monthly U.S. job growth has continued for 24 consecutive months, adding 4.5 million jobs in the last year and shrinking the U.S. unemployment rate in December to its lowest level since 1969 (3.5%). This is yet another indicator of the strong momentum evident in the economy despite interest rate headwinds. Unfortunately, this is now a “good news” is “bad news” indicator, since without some labor market tightening, the Fed’s inflation target may be impossible to reach. Continued labor market strength may, therefore, lead to even higher and longer lasting rate hikes - and an elevated risk of a more pronounced downturn. Our baseline macroeconomic forecast currently anticipates the unemployment rate rising from 3.7% in 2022 to 4.1% in 2023.

If it goes much above this, a recession is likely to ensue.

• The Vermont unemployment rate remains a few ticks above its all-time low, but (at 2.5%) is still the lowest in New England and fifth lowest in the nation. Employment growth in Vermont, however, has been subaltern. While U.S. payroll employment is now 1.2 million higher than pre-pandemic levels (+0.8%), Vermont employment is still about 13.6 thousand lower (-4.3%). While Vermont lost a much higher percentage of jobs during the pandemic than the nation (-20.8% vs. -14.4%) and NE region (-18.0%), its recovery lags every state in the region. Among New England states, Rhode Island (-1.9%), Connecticut (-1.5%) and Massachusetts (-0.3%) are all still below pre-pandemic employment levels, but are closer to full recovery than Vermont. Maine has the highest recovery rate to date (+0.8%) and New Hampshire (0.0%) is dead even.

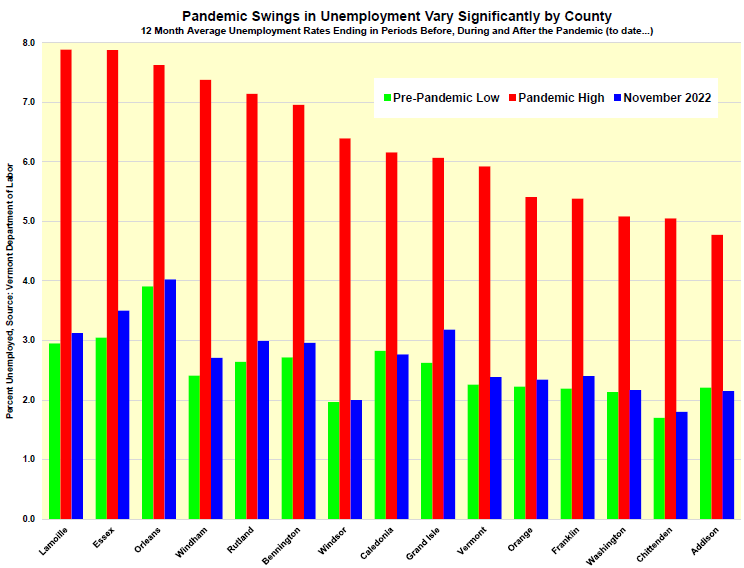

• County level unemployment rates in Vermont are, with some exceptions, following a familiar pattern: lowest in Chittenden County, highest in the Northeast Kingdom, and in between everywhere else. Based on the 12 month average rate ending in November (the latest data available), the highest rate was in Orleans County (4.0%) and the lowest in Chittenden (1.8%). During the pandemic, Lamoille and Essex counties suffered the highest unemployment rates, at 7.9%, but both were well below their prior 35-year record highs of 8.6% and 10.4%, respectively. Windham County was the only county to set a new record high during the pandemic, at 7.4%. These three counties experienced the highest unemployment rate increases, with Windham rising 5.0 percentage points from pre-pandemic levels and Lamoille and Essex rising 4.9 and 4.8 percentage points, respectively. The least affected counties during the pandemic were Addison, where the unemployment rate only rose 2.6 percentage points to 4.8%, and Washington, where the rate rose 3.0 percentage points to 5.1%. Four counties have returned close to their pre-pandemic unemployment rates (Windsor and Washington), or even slightly below (Caledonia and Addison).

• Construction and real estate markets are likely to be among the first and most severely impacted by the Fed’s interest rate hikes, but except for single family housing, the flood of federal money stimulating other capital projects is pushing Vermont construction investment to record levels. New construction starts in the 12 months ending in November topped $1.3 billion, with strength in street, highway and bridge construction, multi-family residential building, and nonresidential amusement/recreation, garage and manufacturing building. In the same period, the number of new single-family housing starts in Vermont declined 23.7% relative to the 12 month period in the prior year. Apartment units, however, more than made up for this decline, pushing total housing starts up by exactly the same percentage (plus, instead of minus), 23.7%.

• Home and other real estate prices will ultimately slow and then decline, but this has yet to show up in the most credible data for this sector from the FHFA. After some of the fastest growth on record over the past 2 years, and 14 straight quarters in which home prices grew month to month in at least 50 states, in the third quarter of 2022 there were price declines in only 7 states, including some of the hottest markets (CA, CO, DC, MN, OR, UT and WA). On a year-over year basis in the third quarter of 2022, there was only one state (DC) in which home price growth was not in double-digits.

• Vermont has experienced its highest year-over-year growth ever in the past three quarters (at 18.0%, 21.0% and 19.0%), and growth since the last cyclical peak is now higher than all New England states except New Hampshire (virtually tied) and Maine.

• Construction employment in Vermont has yet to suffer from growing single-family housing weakness, as there is an enormous backlog of work on already started projects and substantial continuing demand in multi-family housing and other nonresidential building with similar labor input profiles.

State Revenue Update

• Total General Fund revenues in FY23 are now projected to be $120.3M above prior projections, as corporate profits remain resilient and personal income growth defies gravity (and the Fed). Although GFund revenues in FY24 are expected to decline 7.2%, they will still be $45M above prior July 2022 projections. Of note, the projected FY24 decline in the General Fund excluding Healthcare revenues (which were only included in recent years) is 8.9%, the largest annual decline ever – even exceeding the FY2009 decline of 8.1% during the Great Recession.

• It is hard to overstate the significance of the vast federal spending that has been showered on the State since 2020, much of which has been banked, saved, or otherwise retained for current and future spending. As this largesse flows through the economy, it is taxed in a multitude of ways, generating elevated receipts from a plethora of State tax sources. The inflation for which it is also in part responsible has boosted tax revenues as well. It is critical, however, to recognize that this inflation will also impact future State expenditures over the coming years in equal measure. Thus, what appears to be a revenue windfall now, will soon be an expenditure waterfall affecting almost everything the State buys to provide essential public services. While this has already been experienced in capital project budget overruns, it will spread more widely to labor and service costs, eventually affecting every line item in the budget. It has been decades since inflation has been as significant an issue as it will soon be for a wide range of budgetary and planning functions.

• Personal income taxes are more than $50 million ahead of targets for the first half of FY23 and even though the year-end totals are still expected to be lower than FY22 , this represents a $75 million upgrade to the July estimates. The strength in PI was spread fairly evenly among the five components, with estimated payments close to expectations and all other components ahead by about $10M each. There were a few anomalous events in the first half of the year that would reduce the positive PI variance vs. targets by about $10M, but any way you slice it, the momentum in the economy is driving a great deal more taxable income than had been anticipated. Although downside risks are palpable, as noted throughout this update, we now expect a relatively strong spring filing season. As rising interest rates finally bite and the economy slows, PI revenues in FY24 could drop by 10% or more.

• There are many sources of recent Personal Income tax revenue strength. Although full tax year 2021 data are not yet available, preliminary data suggests very strong growth in capital gains due to soaring valuations across all asset classes, substantial business pass-through income and bonus payments in tandem with record business profitability, inflationary impacts on wages and salaries, and disproportionately lower refunding due to widespread and accelerating income growth. There is also mounting evidence that pandemicrelated remote work in Vermont is yielding longer lasting gains, with both elevated in-migration and higher income among first-time filers. Per the below table, although the number of first-time filers has not significantly changed in the last six years, the number of filers with adjusted gross income (AGI) in excess of $100,000 has grown by 71%. First-time filers include both residents and non-residents, but income subject to Vermont taxation has more than doubled since 2019, adding nearly $21M to total PI receipts.

• Preliminary data also suggest that capital gains were also a source of important PI revenue growth in tax year 2021 – increasing by more than 50%. Most of these gains (85%) were derived from stocks and bonds, but an increasing share (and likely to grow) have been from real estate (11%), with depreciable personal property accounting for the balance (4%). As noted in the prior July forecasting document, very little in the way of capital gains from crypto-currency speculation are being reported. However, with massive losses in 2022, crypto holders may turn to their government nemesis for relief by applying these losses against other capital gains to reduce tax liabilities. Despite large market swings (-20% high to low) and an average annual decline of only about 4%, the stock market still had plenty of potential capital gains liabilities that may have been realized during selling in 2022.

• Corporate profit growth has slowed, but is still positive at very high levels, and State revenues reflect this strength. To date, they are more than $10M ahead of target. Refunding has yet to accelerate and payments in the pipeline look strong, arguing for a continued solid second half of the fiscal year. After that, as the economy slows in late 2023 and 2024, profits could boomerang, fueling both reduced liabilities and elevated refunding. Although corporate income receipts are notoriously volatile, the expected FY24 decline of 18% would be the third steepest in the past 25 years.

• Sales and Use taxes are running about 3% ahead of expectations through the first six months of the fiscal year (+9.4M) – mostly as a result of higher than expected inflation. This is likely to continue through much of the remainder of FY23, with some demand reduction as consumer spending slows, offset by higher nominal prices. Relative to the prior July projections, this should generate about an additional $25 million in FY23 Education Fund Revenues. Revenues in FY24 will slow further, as should inflation, resulting in a 2-3% decline in Sales and Use receipts.

• Interest income in both the GFund and Efund have dramatically risen to record levels as higher interest rates and large State cash balances have provided opportunities for more profitable investment options by the Treasurer’s Office. Rarely generating more than about $4M a year, and averaging about $1.7M per year over the past 15 years, year to date income in this fiscal year is already more than $10M. This is likely to persist through at least the balance of the fiscal year, amidst even higher interest rates and continued large State cash balances.

• Bank Franchise tax revenues have also accelerated, despite growing credit reductions that now exceed $4M per year, as the depository base at Vermont banks has grown by more than $6.2 billion over pre-pandemic levels eleven quarters ago. This will push Bank Franchise receipts in FY23 to more than $18M, more than 50% above FY20 levels, and sustain this revenue flow well into FY24.

• Transportation Fund revenues for the first six months of FY23 have been very close to target (-0.7%) and recommended FY23 and FY24 forecast adjustments are similarly minor, -$1.0M and -$0.2M, respectively. The TFund is expected to have the lowest growth rates of any major fund over the next five years, as motor fuel demand continues to recede, energy prices abate following the Russian invasion spike, and the many fees supporting the Fund are fixed. Motor Vehicle Purchase and Use revenues offer the strongest prospect for growth, as limited supplies have created pent-up demand and steep price increases (+27.7% since December of 2019) have yielded more revenue per sale. Rising interest rates, however, will blunt financed sales in FY24, which account for 85% of new vehicle sales and 53% of used vehicle sales, slowing expected growth to less than 2%.

• The U.S. and Vermont macroeconomic forecasts upon which the revenue forecasts in this update are based are summarized in Tables A and B, and represent a consensus JFO and Administration forecast developed using internal JFO and Administration State economic models with input from Moody’s Analytics December 2022 projections and other major forecasting entities, including the Federal Reserve, EIA, CBO, IMF, The Conference Board and other private forecasting firms with whom we interact.

1.17.2023. Kavet, Rockler & Associates, LLC, Williamstown (www.kavetrockler.com) and Economic & Policy Resources (www.epreconomics.com), Williston.