by Timothy McQuiston VermontBiz has asked several financial leaders to offer their expertise on what they see as Vermont’s near future regarding the economy, finance, interest rates and inflation.

This piece was first published in Vermont Business Magazine, shortly before Russia invaded Ukraine (February 24) and before the Federal Reserve Bank raised interest rates on March 16 by 25 basis points (one quarter point or 0.25%).

Some economists had believed this first rate hike in three years (December 2018) could have been as much as 50 basis points. However, the Fed indicated this would be just the start of a series of rate hikes this year intended to slow inflation. Observers are suggesting there will be seven increases.

The last rate cut was a quarter-point at the beginning of the pandemic two years ago (March 15, 2020), which brought rates down to zero. This was the fifth rate cut, and the second in response to the pandemic, since that previous increase.

The Fed action is intended to tamp down inflation by slowing economic growth. It's generally considered by economists to be a blunt tool.

Here’s what our experts are thinking. We are grateful for their insight.

Donald L. Baker, Jr

President

KeyBank, Vermont Market

Two issues that heavily impact the commercial banking business are interest rates and M&A activity.

Regarding interest rates, most forecasts are indicating that The Fed will raise interest rates at least three times in 2022, with some predicting as many as seven rate hikes. I lean toward the lower end of that range, but there is little doubt that they are going up. Higher interest rates will dampen the demand for borrowing, but I don’t believe the impact in 2022 will be as severe as some suspect.

2021 was a record year for global M&A volume and activity should be very strong, again, in 2022. Companies will still be looking to grow by acquisition and private equity firms will remain very active in buying and selling companies. In many industries, current valuation multiples are attractive for owners of companies considering a potential sale. As Vermont is primarily a small business state, we tend to see more of our companies being acquired by larger entities or private equity firms vs. being on the other end of those transactions. In the past, we’ve seen many entrepreneurial Vermont companies with strong brands or high quality products successfully grow to a size where they become attractive to acquirers and sell for high valuations. I expect that trend to continue in 2022.

Robert Miller

CEO

VSECU

There is a lot of discussion about inflation, and for good reason. The reality is that things have become more expensive due to supply chain issues, more consumer demand for goods and services than supply, and labor market shortages. We have already seen mortgage rates go up this year given the expectation that the Federal Reserve Bank will raise interest rates to combat inflation. This will make affordability even more challenging than it is today given the run up in home prices with higher borrowing costs. Inflation has also affected the auto market with limited supply and higher costs, although loan rates have remained very low.

Assuming the Federal Reserve Bank increases interest rates this year, credit card, home equity, and business loans are likely to be affected first. Deposit rates typically take several months to respond until the impact of higher loan rates work through bank and credit union balance sheets. Eventually, all borrowing rates will be higher, but deposit rates should also be higher.

The economy remains strong as there is still a lot of federal stimulus money in the system. We saw deposits grow at another strong pace last year, albeit not the record rate of 2020. We see evidence of growth in consumer spending in our credit and debit card transaction activity. And inquiries for business loans are growing.

The economy is not benefitting everyone the same, though. We continue to help many members in difficult financial situations. There are still too many Vermonters who cannot afford even their basic living needs.

The pandemic remains the wild card. It appears, however, to be less relevant than it was because cases have started to decline again, and the public seems more ready than ever to figure out how to live with COVID. However, it feels like we’ve been in this place before only to be surprised how quickly things can change.

Phil Daniels

Vermont Market President,

TD Bank

Inflation in 2021 was greater than anticipated, up to 40-year highs that repeated again in January. This rapid inflation, along with low supply to meet demand, is driving the Fed to raise interest rates, likely beginning with a 50-basis-point increase in March. Analysts at TD Bank then expect to see further rate hikes even higher than what has been discussed, expanding to a possible additional 75-to-100 basis point increase over the next few quarters.

What this means for businesses is that those that have not yet refinanced existing debt should act now to get into fixed-rate financing or use an interest rate swap to save over the long term. It is also a good time to invest in capital expenditures that could offset some of the other rising costs like wages and energy. The good news is that banks like TD Bank are very well-capitalized and have plenty of credit available to meet these needs.

Betsy Bishop

President

Vermont Chamber of Commerce

While it may feel as though the light at the end of the tunnel is brighter, there is still too much uncertainty surrounding an “end” to the pandemic to truly envision how the economic recovery will unfold. Regardless of timing, we must take long overdue steps to address our workforce shortage. We must create a robust and sustained marketing effort to attract people to move to Vermont for new opportunities, whether that is to find a job, raise a family, or launch a new enterprise.

Over the last two years, businesses have stepped up to ensure the safety and security of their employees, but now they are bearing the burden of increased wages, crippling costs of goods, and supply chain disruptions. These factors combined with rising inflation and interest rates, compound the impact of the pandemic. Combined, these issues will weigh down businesses for years. We rely on businesses to generate jobs and wealth in our communities. Prioritizing recruitment and relocation strategies to attract new workers to fill jobs, as well as making necessary investments in housing and childcare infrastructure, will be crucial to growing our workforce and ensuring we have a sustainable Vermont business community once again.

David S Silverman

President & CEO

Union Bank

Housing/Residential Lending: Demand for housing remains fairly strong and increases in interest rates are only moderating demand slightly. Inventory is scarce throughout our footprint and as a result interest in construction and construction loans is brisk.

Refinances are down. Credit remains widely available despite slightly higher interest rates, and new state funded programs providing assistance to moderate income buyers may become available as a result of proposed legislation.

Labor/Workforce: From all I hear, demand for goods and services remain strong, but being able to hire sufficient numbers of workers to supply the demand remains very difficult. This is across the board in all industries and professions. Hardest hit are travel and tourism service industries such as restaurants and hotels. Ski areas are also impacted significantly. Restaurants in particular are finding it hard to be open seven days per week because of staffing shortages.

Inflation is real and very hard on lower and moderate income people who will struggle this winter to heat their homes and afford gas for their commutes. Some economists think this will moderate later in 2022, but some of these issues stem from labor shortages in the supply chain, not lack of overall supply.

To fight this we expect the Federal Reserve to begin to increase short term rates and stop increasing the money supply. The Fed has quite a balancing act ahead of it, with even odds in my opinion that they will get it right or wrong. With the current pace of economic growth we are experiencing a recession in the short term seems unlikely.

Despite the labor issues the travel and tourism industry faces, they continue to have strong demand for lodging and dining in our resort communities, and we expect this to continue through the winter into summer and fall.

Thomas S. Leavitt

President & CEO

Northfield Savings Bank

Broad-based inflation has settled in as a fact. How long it persists will determine the impact on economic vitality and the confidence of consumers and businesses. With near full employment, Fed moves to raise interest rates are likely to run meeting-by-meeting into the middle of next year. Though that will make borrowing more costly, rates remain in a band of affordability in historical terms.

Northfield Savings Bank is active with our commercial lending and we feel that Vermont enterprise is relatively strong on the whole.

After a couple of years of heightened residential lending activity, we see rising rates as a dampening influence on refinancing. Home purchase and construction financing is driven by the supply of homes for sale and housing starts (the latter being stronger than the former).

Affecting all sectors of the Vermont economy is the gap between robust employment postings and qualified applicants. This will be a deterrent to growth if Vermont is unable to develop and attract new workforce.

One recent development nationally is a mounting reentry to the labor pool by older workers, something that Vermont would benefit from if that participation trend picks up here.

Vermont is fortunate to have strong representation in Washington that has ensured that we gain from small state minimum allocations among the federal programs that have been boosting Vermont businesses and households for nearly two years.

We are grateful to Governor Scott and state leaders and hope to see March bring transition from pandemic to endemic to move beyond the uncertainty that Omicron introduced. NSB has been there for our customers and communities from the declaration of emergency in March 2020, keeping our people, facilities, and programs accessible while also attending to health safety. 2022 and 2023 are likely to be adjustment years for our state and nation.

We are prepared to navigate as we have from the outset of this eventful decade. Through 155 years of serving Vermonters, we have learned how to adapt and transform as times have dictated. We are confident that Vermont is a place of builders, makers, and doers that always see things through. We intend to be here for them.

Darcy U Carter

District Director

SBA, Vermont District Office

US Small Business Administration

Vermont SBA is working on several fronts to support small businesses, some of which are still impacted by the pandemic. We are processing COVID-19 Economic Injury Disaster Loan increases to continue providing pandemic assistance.

As of February 3, the SBA has disbursed $509,508,510 in EIDL funds to 6,571 Vermont small businesses.

We are also seeing an increase in the use of our regular SBA guaranteed loan programs by banks and credit unions.

The 504 program is booming because the rates are still low so it’s very attractive for businesses to lock in that long term, fixed rate.

In other good news, Brattleboro Development Credit Corporation was approved as an SBA microloan intermediary, which will increase lending to microenterprises in Southern Vermont.

Cassie Polhemus

CEO

Vermont Economic Development Authority

The common challenge businesses are facing in this economy is the lack of workforce.

This is especially the case in Vermont where the demographic trends for many years have exacerbated this problem.

And now, with escalating inflation, everything is more expensive. This will not be sustainable without controlling inflation so it does not severely threaten positive trends in employment and business expansion.

However, sharp increases in interest rates to rein in inflation will hamper steady and extended growth.

NBT Bank

On inflation from Chief Investment Officer & Chief Economist Kenneth J. Entenmann: In early February, the Consumer Price Index report showed the year-over-year inflation rate was 7.5%, the most in 40 years and the eighth consecutive month of +5% CPI. Even after excluding food and energy, the core index was up 6%. It was hoped that goods inflation would begin to subside as consumers shifted back to service spending, but consumers are making this shift and the decline in goods inflation is not happening as hoped or predicted—at least not yet. Meanwhile, service prices are soaring. Wage and housing prices typically lag the CPI, and they are rising rapidly. This means the inflation data is likely to get worse before it gets better. So that means it is critically important for businesses to manage your cost structures—both labor and inventory—in this coming year.

On rising interest from rates from Chief Investment Officer & Chief Economist Kenneth J. Entenmann: The Federal Reserve Bank has made its policy projections clear. Tapering will end in March. Fed Funds will increase by 0.25% in March to be followed by quarterly increases through 2022. Even the possibility of balance sheet reduction (Quantitative Tightening) is on the table. Of course, the equity markets don’t like higher interest rates, but this projection was very much the consensus; no surprises here. The equity markets should be more than capable of absorbing Fed Funds at 1%. However, with persistent and pervasive inflation, the fear is the Fed will be forced to take a more aggressive stance. So, what does this mean for business? It means that the time of easy money is over and managing your growth strategy will require close collaboration with your lender.

On commercial lending from Regional President Dan Werme: If we have learned nothing else from the business impacts of the pandemic, we now know more than ever how important it is to have a quality relationship with your banker. As you look to overcome challenges such as inflation and rising rates, the effects of labor shortages and supply chain issues, you will find yourself in a much more comfortable position to identify solutions if you have a banker who understands your business and is capable of identifying options that work for you not only in good times but also these more difficult situations.

John J Dwyer, Jr

President and CEO

New England Federal Credit Union

As the economy improves and the national interest rate environment is impacted, we are certainly going through a transition in the lending market. We are coming out of a relatively long “low-rate” environment which led to record loan production for credit unions, the ability to lower payments for members, and a resulting appreciation in core asset values. I don’t know of many people who truly foresaw the market rate impact that a pandemic would cause in the beginning of 2020: nearly two years of historic loan demand from consumers and businesses across the country. Vermonters and Vermont businesses were no different and have had the opportunity to reduce their payments on various forms of credit in the long term. We, and many other financial institutions, have focused on meeting the needs of thousands who will benefit from these low rates for the term of the loan.

Macroeconomic factors here in the US are now impacting the level of loan rates and will likely continue to do so in 2022. Steps taken by the federal government have strengthened the financial position of many consumers and businesses which, in turn, has mitigated the impact of the pandemic and helped people buy homes, business assets, and other items. We are now seeing a transition to what could be described as a more “normal” rate environment—one which has some higher rates for longer term loans and more slope to the yield curve. Although we haven’t been in a normal environment for some time, we understand that consumers and businesses will have to adjust to rates moving up. For mortgages, the level of refinancing will most assuredly come down and new loans will be for home purchases. That said, many consumers will shift toward some traditional options to gain access to credit or the equity in their homes. We expect a return to auto, home equity, RV, boat, and unsecured lending as the economy improves.

We all realize that coming off these historically low levels will take some adjusting. As changes occur, Vermont consumers and businesses know that their local financial institutions can assist them with their credit needs whether rates are increasing or decreasing.

Kathryn M Austin

President & CEO

Community National Bank

As I expect you will hear from others, both the impacts of and recovery from the pandemic vary among industries.

In general, we have found that our business customers are doing well. The availability of relief programs, both federal and state, assisted Vermont businesses through the pandemic. Vermonters are resilient, and we saw many businesses pivot in response to new demands and the changing marketplace to achieve very good financial results.

Bank balances for both consumers and businesses remain higher than normal still, although we are beginning to see some decline.

Travel, tourism and hospitality businesses have been impacted the most, and their recovery has been the most protracted.

We are experiencing pretty robust commercial loan demand, especially in Central Vermont and Chittenden County.

Real estate lending has slowed a bit, as refinances have slowed. While there’s still a robust real estate market, it is dampened by a lack of inventory.

Everyone feels the effects of inflation and shares concern about the future as it persists.

As we are all hearing, the Fed is expected to raise rates perhaps several times this year in an effort to curb inflation. Those rate hikes will likely slow the economy as commercial rates adjust with changes to short term rates.

Almost universally, our business customers are challenged with recruitment and retention of their workforce. In nearly all industries, there are not enough available and qualified employees to fill their jobs.

Supply chain issues persist but appear to be easing. Pandemic fatigue is felt everywhere, as we all look forward to getting closer to “normal”.

Mike Reynold

CEO

Farm Credit East

When the pandemic began nearly two years ago, it quickly became apparent that farms and food businesses are essential. And while there were significant disruptions at the outset, their ability to keep operating throughout is a testament to their resilience. Federal assistance was important in helping many of them through that uncertain period.

Agriculture, like most sectors of the economy is currently feeling the effects of inflation and supply chain disruptions. As farms prepare for their spring work, many are being impacted by higher costs and availability of inputs. We’re also hearing from our members that availability of labor continues to be a challenge, in part due to the ongoing effects of the pandemic. And the impact of the cost and availability of labor and other inputs is also being felt further down the marketing chain.

We expect some improvement over the course of the year and although there is still uncertainty on many fronts, we’re optimistic about the opportunities for the farms and forest product businesses we serve, and look forward to working with our customers to help them navigate the current business climate.

Linda Rossi

State Director

Vermont Small Business Development Center

VtSBDC’s advising staff provides guidance on financing to small business owners throughout the state, staying up to date on the latest resources and financing opportunities on the federal, state and local levels.

Our advisors have noticed a few specific challenges over the past year.

One is the issue of inflation, especially when it comes to cost of goods sold.

This issue is impacting business owners’ bottom lines with many becoming reluctant to increase their prices, but realizing they have no choice.

There is also a growing concern that the Federal Reserve has indicated possible increases in March and June of 2022. This may make money more expensive, especially Lines of Credit which many small businesses depend upon.

Another pressing question is how to handle the impact of the various Federal, State and local loans and grants on 2021 tax returns. As always, VtSBDC’s goal is to provide small business owners with timely, reliable resources and data to help them make informed decisions.

Joe Carelli

President Vermont

Citizens Bank

From Citizens’ perspective, the economic prognosis for 2022 remains bullish.

Whether in Vermont or New Hampshire, our business customers continue to experience an exceptionally strong demand for their products and services.

In Vermont, we are seeing tourism and manufacturing rebound, while in New Hampshire we are witnessing more companies expanding their footprints, including high-tech manufacturers, metal fabricators, biotech, pharma and other businesses in the life sciences sector. All of those industries have enjoyed high single to mid double-digit growth during the COVID pandemic.

The recovery gained momentum in 2021 on the heels of the vaccine rollout and rising demand for goods, services, and space. And yet, there are still supply chain issues across the board and labor scarcity is the overarching issue that concerns our business customers. In response to the labor shortage, employers are significantly raising the base pay they offer in order to attract talent.

While the recovery is well under way in Vermont and across the United States, persistent inflation has fueled calls to increase interest rates.

January’s consumer inflation rate of 7.5% underscored the increases in the price of basics items that is eating into the paychecks of families in Vermont and across the country.

Short-term interest rates have begun ticking up in anticipation of Federal Reserve action. Given the imminent conclusion of a near-zero rate environment, business customers with variable interest rate exposure would be wise to hedge that risk while also navigating the volatile markets that have been whipsawed by rising geopolitical tension.

For the Vermont business community, supply chain and workforce issues should improve over the next year. As noted, there will be continued pressure on the Fed to end tapering and raise rates to tame inflation. Our forecast for 2022 is strong unless a new vaccine-resistant COVID variant becomes widespread and changes the dynamics.

Scott A Wilson

President & Chief Executive Officer

SeaComm

Rising costs have had an impact on our members, like most Americans, they are feeling it at the pumps and grocery stores. Consumable good prices are eating away at discretionary spending and having overall impact on household budgets.

We do believe as the Federal Reserve begins to raise interest rates incrementally, to stave off out of control inflation, it will have an effect in the short run in relation to borrowing. Everyone has gotten use to these lower interest rates, which has been extremely beneficial when purchasing an auto or home.

As those increases take place during the year, it may give pause to consumers to rethink a new purchase as they have been accustomed to lower rates, which equates to lower payments.

They may purchase an auto or home at a lower price point to alleviate those increase in monthly payments as well.

All of which has an effect on loan demand. Longer term we do believe it will begin to normalize and consumers will get used to the increased rates and adjust accordingly as we near year-end and going into 2023.

Matt Durkee

Senior Vice President and New England President

Community Bank NA

(This is the only piece added after the Fed raised interest rates 25 basis points on March 16, 2022).

The current interest-rate environment is muddy, especially when the effects of the increase in current energy costs remain to be determined. The February inflation rate and energy price increases that were recently reported were prior to the Russian invasion of Ukraine. We were already seeing significant inflation due to various government policies. Now, with the further energy price increases from the war and subsequent banning of the import of Russian oil, inflation appears to be headed for a further increase.

To counteract this inflation, the Federal Reserve just raised rates by a quarter point, which is the first increase in the federal funds rate in three years, with up to six more increases expected. Usually, as interest rates go up, consumers curb their spending, which eventually slows price increases. Right now, it’s unclear how much rates will have to increase to slow demand.

Consumers will also see several types of credit card rates increase. Car loans, primarily due to the competition from both bank and captive lenders, will not see an immediate increase in the rates on new car purchases. When it comes to residential mortgages, long-term fixed mortgage rates have already been on the rise since they are influenced by the economy and inflation.

The average 30-year fixed-rate home mortgage has risen above 4% (up over 1% since October) and is likely to keep rising. The current residential home market remains very strong with little inventory for sale, even with rates up recently. Many homeowners with adjustable-rate mortgages or home equity lines of credit, which are pegged to the prime rate, will also be affected. An adjustable-rate mortgage adjusts annually, while a home equity generally adjusts immediately. Student loan rates are generally fixed, so most borrowers won’t be impacted immediately by a rate hike.

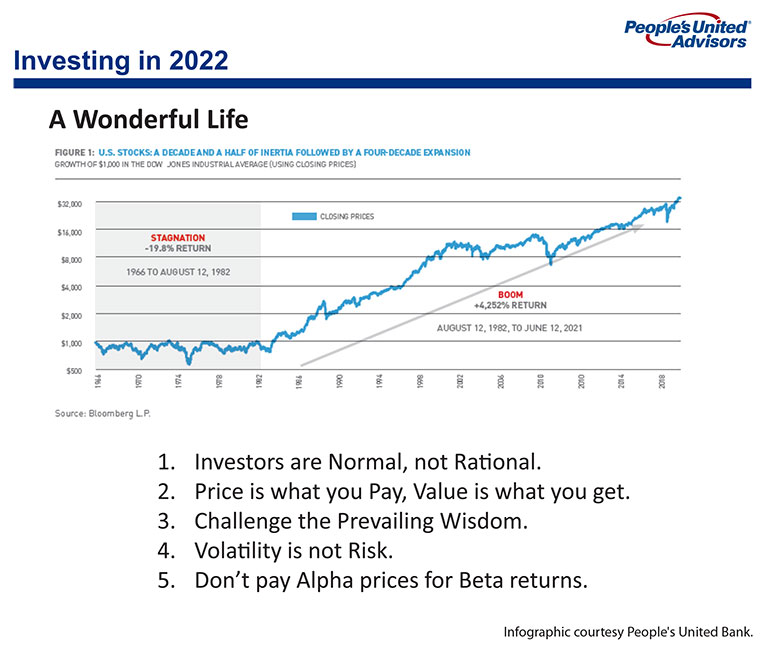

John Traynor

Chief Investment Officer

People’s United Bank

John Traynor holds many investment seminars for People’s during the year all over the Northeast. About a third of them are still remote.

He expects and agrees that the Fed will and should raise interest rates (probably by 50 basis points) when they meet later this month.

The economy has been running too hot for too long, he said, and the Fed has probably waited too long to address the situation.

Like many, he’s more concerned with inflation than the interest rates themselves, but in a very specific way.

Wage inflation is long overdue, he said. He tells corporations, which have been very profitable for a very long time, that they now must start sharing those profits with their employees.

On the other hand, he is concerned about the other side on the cost of goods inflation. Some of this is from the pandemic and some of this is on too much reliance from one supplier, China.

He sees manufacturers taking a somewhat different approach. First, they’ll be looking to diversify their supply chain. In Asia, he sees Vietnam and Indonesia being logical suppliers in addition to China. India also would be a tempting option, but it doesn’t appear that they’re ready yet to handle it.

Traynor also said that manufacturers are telling him that they will shift some of their focus from “just in time” methods to “just in case” with that diverse supply chain.

Vermont, more than any other state in the region, boasts about half of its industry in advanced manufacturing See cover story on OnLogic page 8.

On the investment side, he is seeing growing diversity within stock portfolios. This is important, he believes, regardless of what happens in Ukraine.

Investors are seeking dividend-bearing value stocks versus the aggressive growth stocks that have driven equities to dizzying heights since the Great Recession.

While housing has been a big winner in recent years, he doesn’t see a rise in mortgage rates (about a full point since last summer) as an impediment to real estate. Interest rates tend to be a lagging indicator in any case and he anticipates that home values will remain strong.

Like others of course, he is concerned with the tight workforce.

He said 3 million Americans left the workforce during the pandemic and he’s projecting that only 1 million will return.

There were two driving factors, as he sees it.

First was a quality of life choice born initially from working, ironically, from home during the pandemic

Second was the growth in retirement accounts and the calculation made by many that they could afford to retire comfortably.

But he believes it is that very work-from-home option that could benefit Vermont, where that home could be here and that work could be anywhere.

And it’s that bumping up the remuneration he mentioned earlier that could get workers back on the job.

![]()