(Economists Tom Kavet, of Kavet, Rockler & Associates, LLC Economic and Public Policy Consulting in Williamstown, on behalf of the Legislature, and Jeff Carr, of Economic & Policy Resources in Williston, on behalf of the Administration, presented their consensus revenue forecast to the state Emergency Board on Thursday, July 28, 2022. This is a regular, semi-annual report to the E-Board, comprised of the chairs of the financial committees of the Legislature and Governor Scott.

They are expecting historic tax revenues to continue to grow through the next two fiscal years, though easing back by FY24.

Personal and corporate taxes, along with rooms & meals and the sales tax, will lead the way, as they have over the last two years.

Downside risks include a tight labor market, housing costs, inflation, supply chain issues, the Russian invasion of Ukraine, the ongoing pandemic and the frankly uncertain effects of the Fed action to increase interest rates.

On the other hand, there is no expectation of a spike in the unemployment rate nor in a housing collapse. Americans have an enormous amount of stored-up wealth and pent-up demand.

The following remarks were taken from Kavet’s report.)

by Tom Kavet

With one foot still on the gas and the other now slamming on the brakes, federal fiscal and monetary policies are generating opposing forces that will both confuse and control the economic environment affecting the State economy and revenue flows in the coming years. While direct pandemic health effects have receded from prominence, their legacy of vast federal spending, shifting consumer preferences, supply chain disruptions and reduced labor force participation continue to resonate loudly. With viral mutations continuing and geo-political instability from war in Europe added to the mix, the outlook continues to be extremely volatile and unpredictable.

Despite all the current risk, FY22 revenues soared on the flows of the more than $10 billion in Federal spending which have been swelling through the State economy since early in the pandemic. They have lifted taxes of all kinds, but especially income and consumption taxes, which are the largest sources of State revenue. Stunning FY22 gains in Personal Income and Corporate revenues added nearly $300M in revenues above already impressive FY21 levels, as total General Fund revenue topped $2B.

While downside risks abound, even with dramatically slowing economic growth in FY23 and FY24, revenues could remain at historically high levels. Given the heightened level of uncertainty, interim quarterly revenue updates should be considered if external conditions appreciably worsen in FY23.

Economic, Fiscal and Monetary Policy Update

• With inflation surging and more deeply embedded with each passing month, the Fed is moving with escalating force to slow the economy and thereby reduce demand to levels that can be met by supply – a so-called cyclical “soft-landing.” The problem is, however, that the tools with which the Fed has to slow demand:

1) Work in disparate, inefficient and unfair ways throughout the economy;

2) Have uncertain and long lags between policy implementation and intended results;

3) Do nothing to alleviate supply issues affecting inflation that are largely related to the pandemic; and 4) May be delayed in effect and/or offset in part by massive prior Federal fiscal policies designed to mitigate the impacts of the pandemic that are still extant and flowing through the economy. This lattermost condition could ultimately cause the Fed to hike rates much longer and/or more aggressively, posing the greatest risk of recession. This risk, and its connection to the primacy of containing inflation at all costs, was underscored in the below testimony by Fed Chair Powell.

Fed Chairman Jerome Powell, in testimony to Congress, June 29, 2022: “Is there a risk we would go too far? Certainly there’s a risk. The bigger mistake to make—let’s put it that way—would be to fail to restore price stability.”

The current macro-economic forecast underlying these revenue projections assumes a “soft-landing” to be possible, with a marked slowing in economic growth in both FY23 and FY24. Odds of a recession however, remain extremely high and are growing. A Wall Street Journal panel of academic, business and financial economists currently put the chance of a recession in the next 12 months at 49%, similar to a level reached in early 2008 at the onset of the Great Recession (chart on page 27). If conditions continue to worsen, quarterly interim economic and revenue adjustments may be prudent in FY23.

In the meantime, the effects of prior fiscal and monetary pandemic stimulus policies continue to affect the economy. While new deficit spending has not been initiated since the January forecast, vast stores of saved and unspent stimulus remain, representing potential future purchases and demand. Soaring asset prices and reduced debt has also strengthened household and business balance sheets as net worth swelled to record levels over the past two years. This wealth along with high cash and cash equivalent holdings give the economy a cushion against initial recessionary impacts, but are also a part of the reason the Fed may need to tighten even harder to slow demand.

Of note, the greatest average household growth in net worth during the past two pandemic-affected years has been the bottom 50th percentile of wealth (+107.6%) and the top 1% (+43.5%). In the former group, net worth grew from just under $30,000 in the first quarter of 2020 to more than $60,000 in the first quarter of 2020 and grew from 1.8% of total net worth to 2.8% - still well below its peak of 4.3% in 1992. Over the same period, average household net worth for the top 1% grew from $24.3 million to $34.9 million, and increased its share of total net worth from 29.7% to 31.8%.

• Labor markets remain extremely tight, as job openings continue to exceed the number of unemployed persons, quit rates remain high and layoffs, low. U.S. payroll employment growth remains solid, with 372,000 jobs added in June. While total U.S. employment is still shy of its pre-pandemic peak in February of 2020 by 0.3%, total private employment in June topped its pre-pandemic level for the first time. No New England state has yet to reach pre-pandemic employment levels. Vermont continues to trail all other NE states with payroll employment still more than 5% below its January/February 2020 peak. • The U.S. unemployment rate held steady at 3.6% in June, while Vermont dropped to 2.2% - the fifth lowest rate in the nation and one of its lowest levels ever. The only period in Vermont history with a lower unemployment rate was in March-May of 2019.

• Much of the extreme acceleration in inflation has been due to spiking energy and food prices related to the Russian invasion of Ukraine. The Russian blockade of Ukrainian grain exports and disruptions to agricultural production have impacted food prices across the globe and the coordinated sanctions applied against Russia by many nations has caused chaos in energy markets – especially in Europe. Coinciding with strong post-pandemic fuel demand, fragile gasoline and diesel refinery production, and concentrated supply ownership, both oil and natural gas prices have soared. While new supply may eventually come on line to replace some Russian supply and demand could subside during a recessionary period, the conflict creates considerable additional uncertainty to any economic forecast.

• Some of the acceleration in price growth has been due to rapid and extreme swings in demand during various phases of the pandemic. As shown in the charts on pages 11-12, there was a seismic shift in consumer demand for goods and a comparable reduction in demand for services during the early phases of the pandemic, creating extraordinary market disruptions. Prices for shipping and commodity inputs to goods production rose by multiples of 2x-6x, fluctuating wildly as supply chains struggled to meet demand. Now, as demand for goods subsides, many retailers have been left with bloated inventories, while spiking demand for leisure and hospitality services is leaving this sector hard pressed to find workers, even with hefty wage and price increases.

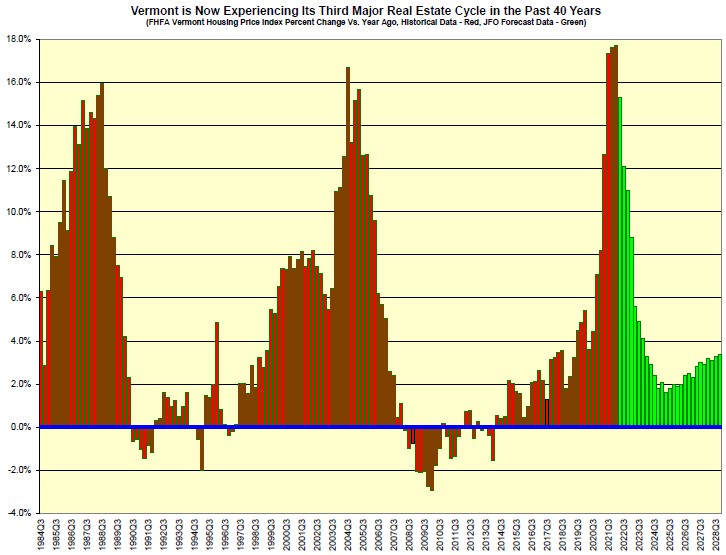

• State real estate markets have seen record price appreciation during the last three consecutive quarters, topping 17% year-over year growth in each quarter (see page 35). As interest rates rise, prices should moderate, but the absence of excess supply will temper price declines and provide a shorter recovery period. If prices do not moderate soon, further double-digit price increases will result in a significantly steeper and longer downturn. How the pandemic ultimately affects the persistence of elevated in-migration and second home ownership could reshape and extend the current real estate cycle.

State Revenue Update

• Total revenues across all three funds in FY22 soared to more than $3 billion, 8.1% above expectations. Largely on the strength of colossal gains in both personal and corporate income tax receipts, the General Fund was up 12.2%. The Transportation Fund was the only fund to finish the year below target, missing by 2.8%, as high fuel prices and severely limited vehicle production reduced revenues. The Education Fund finished slightly above target (+1.3%), as Sales & Use tax strength offset weakness in allocated MVP&U and Lottery receipts.

• Personal Income tax receipts posted phenomenal growth in FY22, representing most of the above-target revenue experienced in the General Fund. While we are still analyzing tax year 2021 data – some of which will not be available until November of this year – it appears that despite a great deal of income from higher AGI groups, there were gains across the board. With asset prices surging throughout many investment classes, taxable gains will likely be a big part of this. One source of taxable gains that may be missing are what the IRS refers to as “virtual currencies,” better known as crypto-currencies (see next page). As equity markets and many other asset prices decline in tax year 2022, FY23 PI revenues will be affected. Elevated refunding activity is also likely in both FY23 and FY24, as the economy slows and lagging estimated payments overshoot liabilities.

• Corporate income tax revenue closed FY22 at an astonishing $223.3 million, 67.3% above FY22 levels and about 25% above expectations. The surge in revenues was widespread and reflected the pricing power of many corporate entities in an inflationary environment. U.S. corporate profits have now grown 51% over the past 7 quarters, though year-over-year growth has slowed from 45% in the second quarter of 2021 to 13% in the first quarter of this year. As the economy slows, profit growth will be much harder to come by and high estimated payments will likely begin to boomerang in FY23 and FY24 with sharp increases in refunding. Despite expected revenue declines in both years, Corporate income will still be more than 20% above FY21 levels in FY24. • Meals & Rooms tax revenue in FY22 bounced back to levels that were 4.4% higher than projected prior to the pandemic (as forecast in January of 2020). This full recovery has been fueled by subsiding fears of pandemic risk, enormous pent-up demand for travel and ample financial capacity to spend. With continued air travel disruptions and easy driving distances to Vermont from major metropolitan areas, tourism visitation flourished last year. Unless interrupted by a new and more deadly variant, tourism spending should continue to support solid future growth throughout the forecast period.

• Strong growth in Insurance Premiums and Captive Insurance receipts propelled total Insurance revenues to a record $65.7 million in FY22, 8.7% above FY21. Despite growing competition from other states and countries, Vermont has managed to maintain a leadership role in the captive industry for more than 40 years, providing more than $25 million to the General Fund in FY22.

• Source General Fund Property Transfer tax revenues rose to a record $77.7 million in FY22, about 4.5% above expectations. Despite limited properties for sale, huge price increases in the last year supported the strong PTT revenue showing. With interest rates rising over the next two years, property transactions will slow and prices are likely to moderate, resulting in declining revenues in both FY23 and FY24. The current absence of overbuilding, however, should support resumed growth towards the end of the 5-year forecast horizon. PTT revenues allocated to the Available General Fund are less than a third of the Source revenue, but still contribute about $20 million per year to the Fund.

• Cannabis tax revenues are expected have a somewhat slower revenue phase in during FY23 and FY24 and are now subject to an erratic allocation scheme that zeroes out all allocations to the Available General Fund in FY24-26, only to have it resume in FY27. It will still generate a smaller flow to the Education Fund via the Sales & Use tax in each year of the 5-year forecast period.

• Inflationary price increases will generally result in higher State tax receipts, except with taxes based on physical volumes, such as a large portion of the transportation fuel taxes, almost all fee-based revenue sources (the largest of which are Motor Vehicle Fees and General Fund Fees), or those with tax rates indexed to inflation, such as the Personal Income tax. Elevated inflation across the entire 5-year forecast horizon adds significantly to the nominal dollar tax revenue levels reported.

• The Transportation Fund will have an unusual year in FY23, as the Motor Fuel Assessment tax algorithms will garner additional revenue from high recent fuel prices, which are lagged in a way that will benefit at least the first half of FY23 and push total Gasoline revenues up 8.8% for the year. If fuel prices recede, as gasoline futures contracts now suggest, FY24 will experience an opposite effect, causing Gas tax revenue to fall 2.8%.

• The U.S. and Vermont macroeconomic forecasts upon which the revenue forecasts in this update are based are summarized in Tables A and B in the full report (SEE HERE), and represent a consensus JFO and Administration forecast developed using internal JFO and Administration State economic models with input from Moody’s Analytics June 2022 projections and other major forecasting entities, including the Federal Reserve, EIA, CBO, IMF, The Conference Board and other private forecasting firms with whom we interact.