Table Courtesy Kavet, Rockler & Associates.

by Timothy McQuiston, Vermont Business Magazine The state’s economists, Jeff Carr for the Scott Administration and Tom Kavet for the Legislature, presented a stunning but expected consensus revenue report to lawmakers and the governor on Thursday. Along with upgrading the annual tax revenue estimate by over $40 million, they forecasted growth in this and next fiscal years to be greater than they’ve been in more than 30 years.

The economists met for their annual update before the Emergency Board, which is comprised of the chairs of the four money committees of the Legislature and Governor Scott, who chair the E-Board.

Of course, this is largely due to $10.1 billion in federal pandemic recovery and stimulus funds. They also suggest that except for the extremely tight labor market and supply chain problems (profoundly with automobiles), the economy would be cooking along at an even greater rate.

Other good news includes positive net migration and significant broadband expansion enhancements: “This could be one of the most transformational changes affecting the long-term Vermont economy in decades," Kavet said (see his report HERE).

On the other hand, workforce problems could get even worse, which even before the pandemic was a binder on the state economy: “Some negative pandemic effects are also likely to persist, including earlier retirement ages for older workers, and the resultant reduction in the available labor force.”

And of course there is inflation: “Inflationary pressures will remain well into 2022 and 2023, as the pandemic affects global manufacturing, transportation, and consumer preferences. While markets will eventually adjust – they cannot turn on a dime – and prices will reflect supply/demand imbalances.”

And then there is the double-edged sword of home values during the pandemic: “Growth in Vermont was 17.7%, the highest in more than 30 years. This will affect Grand List valuations and Education Fund tax rates in the coming years.”

Housing affordability was already a problem for many Vermonters. But the surge in prices will lead to greater equity and, presumably, increase demand for new home construction.

Carr said the macroeconomic forces (see his report HERE) now driving the economy are likely unsustainable: “While the relatively upbeat economic and State revenue collections environment appear to be relatively secure for the next 12 to 18 months, that near-term positive character of the economy and State revenues will face stiff challenges as we move towards the period including fiscal year 2024 and beyond.

“As a result, this forecast update expects that the current environment and strong forward momentum to the economy and revenues will likely not be sustained much beyond fiscal year 2023.

“This forecast update expects that the economy and State revenues to run into significant headwinds in the out-years of the forecast period resulting in significant lost ground relative to the consensus revenue forecast approved by the Vermont Emergency Board in July of 2021.”

Graphs Courtesy EPR

Kavet Report

Two unprecedented forces continue to shape the State economic and revenue outlook: The mercurial path of the pandemic and the torrent of federal fiscal spending and related monetary policies to offset its effects. It bears repeating that both are without historical precedent and remain highly unpredictable.

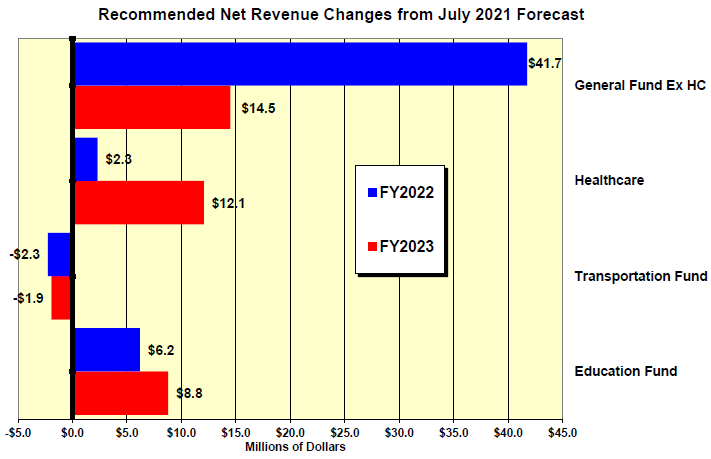

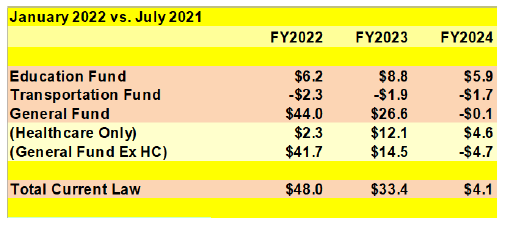

What we do know is that FY22 revenues have benefitted greatly from a portion of the more than $10 billion in Federal spending now coursing through the State economy. It is showing up in taxes of all kinds, but especially in income and consumption taxes, which are the largest sources of State revenue. Most of these flows are at or slightly above prior July 2021 expectations, with aggregate recommended forecast adjustments across all funds of about 1.7% in FY22 and 1.2% in FY23. The most significant upgrade is to this year’s G-Fund, which should receive an additional $41.7M, about 2.4% above prior estimates, due mostly to strength in Personal and Corporate income taxes and a faster recovery in Meals & Rooms receipts.

State Revenue Update

• If the pandemic recedes to “manageable” levels, extraordinary demand and improving labor markets could generate State nominal dollar GDP growth of nearly 9% in FY22 and 6% in FY23 - the highest two-year growth in more than 30 years.

• There will be significantly higher and more persistent inflation in both this fiscal year and next. Some sectors will likely experience much higher or much lower rates, as supply chain bottlenecks develop and resolve and supply and demand extremes also emerge as consumers shift purchasing preferences.

• The CPI spiked to its highest level in 40 years in December, at 7% year-over year growth, and could top this rate in the first quarter of 2022, before receding.

• Inflationary pressures will remain well into 2022 and 2023, as the pandemic affects global manufacturing, transportation, and consumer preferences. While markets will eventually adjust – they cannot turn on a dime – and prices will reflect supply/demand imbalances.

• Some of the acceleration in price growth has been due to rapid and extreme swings in demand during various phases of the pandemic. such as during the early phase of the pandemic, when consumers reduced expenditures on many items (such as services) and shifted it to others (such as goods), creating extraordinary market disruptions. At one point in time, the sudden reduction in motor fuel demand resulted in negative future prices for crude oil. When demand roared back this year, prices spiked, but are now drifting lower amidst Omicron fears.

• A great deal of what happens to rates of inflation over the next several years will also be psychological and behavioral. When people believe something will be in short supply, they often turn a potential shortage into a real one by quickly elevating demand via hoarding. This happens among both households and businesses and can create wild price swings until markets can respond and behavior shifts. Some of the recent port congestion was exacerbated by early seasonal product ordering and the absence of warehouse space to hold these goods.

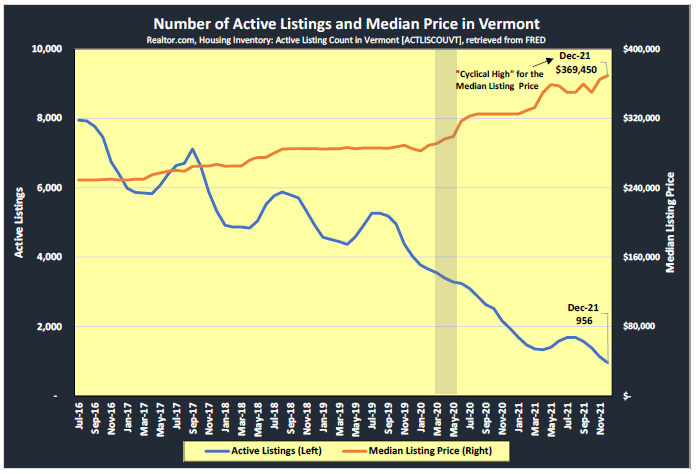

• State real estate markets are in the midst of their third major cyclical upswing in the past 40 years, with home price gains in double digits likely throughout FY22 and FY23. With interest rates still relatively low, plentiful capital and income, and a decade of underinvestment in new housing, all the ingredients are in place for extraordinary price growth until supply catches up or incomes falter – probably not for several years.

• Unlike any other previous state or NE regional real estate cycle, there will be several nonresidential commercial building categories that will not share in the upswing. Office, retail and, especially, hotel/motel valuations and new construction demand will be subdued by lingering pandemic effects.

• There will be more single-family residential building (both primary residence and second homes), however, especially renovations and expansions, and commercial warehouse construction. Regional shifts away from the most densely populated urban areas to suburbs and more rural areas with good broadband and recreational amenities are also likely to be a feature of this cycle – potentially benefitting Vermont.

• Massive infrastructure spending will result in more nonbuilding construction, especially roads, highways, bridges, electric infrastructure, broadband development, airports, public transit, climate-related investments to buildings (efficiency upgrades) and electric grid enhancements.

• Price bubbles are likely to develop as supply/demand imbalances occur and assets are repriced – such as is now occurring with housing. Home valuations increased by double-digit rates in the most recent quarter (2021Q3) for every U.S. state except ND, LA and DC. Growth in Vermont was 17.7%, the highest in more than 30 years. This will affect Grand List valuations and Education Fund tax rates in the coming years.

• Labor markets are gradually healing, with average U.S. monthly job growth of about 500,000 per month. At this rate, total U.S. payroll employment should regain pre-pandemic levels in late 2022.

• The latest U.S. unemployment rate dipped to 3.9% in December, with Vermont’s at 2.6% in November (the latest available), the fourth lowest in the nation and lowest in New England. • Job openings currently exceed the number of unemployed individuals, indicating both job mismatches and a large number of workers who have still not rejoined the labor force.

• The combination of strong demand for goods and services and fewer workers in the labor force has pushed wages significantly higher, driven the quit rate to record highs and dropped layoff rates to record lows. Worker absences due to illness are also on the rise, as the Omicron variant spreads throughout the nation.

• Many of the most severe economic impacts from the pandemic have been evident in, or caused by, labor force disruptions. Millions were out of work for extended periods, re-revaluated their jobs and places of work, and made changes. Early retirements among older workers, most vulnerable to COVID risks, may permanently reduce labor force participation rates.

• Some beneficial pandemic effects for Vermont are likely to persist in the next two fiscal years and possibly beyond, with positive net migration population effects from continued remote work options at many national and regional firms. Between July of 2020 and July of 2021, the Census Bureau estimates net migration to the State totaled 4,864 persons. In a typical year, between 20,000 and 30,000 people move into Vermont, and a comparable number leave the State. Births between mid-2020 and mid-2021 were exceptionally low, at 5,057 and deaths totaled 6,884, leaving a net total population gain of 3,075. Revisions to Vermont population estimates over the last decade are still being made in light of the 2020 Census, which showed about 19,000 more Vermonters in 2020 than had been previously estimated. Most of this is likely to be due to net migration, since data on natural changes are less prone to revision.

• Huge federal broadband investments will enable remote work in more Vermont locations and likely create the infrastructure necessary to sustain and possibly expand these migratory gains. This could be one of the most transformational changes affecting the long-term Vermont economy in decades.

• Some negative pandemic effects are also likely to persist, including earlier retirement ages for older workers, and the resultant reduction in the available labor force.

State Revenue Update

• Total Revenues through the first half of FY22 (General, Transportation and partial Education Funds) are about 2.6% above targets (about $34M on a base of more than $1.3B). Accordingly, the revenue adjustments recommended herein are relatively small, totaling about 1.7% in FY22 and 1.2% in FY23 across all three major funds. Revenue changes in the Transportation Fund and Education Fund in both fiscal years are plus or minus about 1%, with General Fund changes between 1.4% and 2.4%.

• Recommended revenue comparisons relative to the July 2021 forecast are outlined in the below table:

Table Courtesy Kavet, Rockler & Associates.

• The revenue strength in the first 6 months of the fiscal year was concentrated in Personal Income, Corporate Income and Meals & Rooms receipts. With corporate profits at record levels, demand strong and prices rising, income tax liabilities have risen accordingly. Tourism travel continues to be heavily tilted towards on-line short-term rentals, but increasing numbers of visitors are venturing out and spending freely. With an aversion to air travel still evident and 50 million people within a five-hour drive from Vermont, tourism visitation has exceeded expectations, and through the first six months of the fiscal year is 50% above the same period in FY21 and 5% above the same (pre-pandemic) period in FY20.

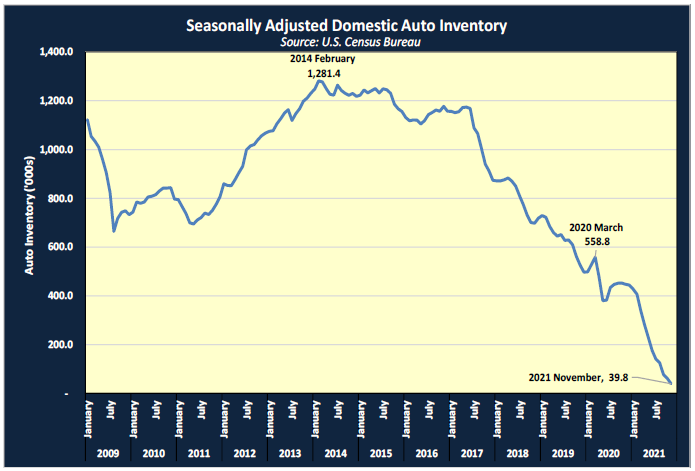

• There is strong evidence that several revenue sources that have been at or slightly below FY22 targets would be higher, but for shortages of taxable supply. Empty car lots at dealers, a shortage of homes for sale, and long delays in ordering many items has reduced taxable receipts in MVP&U, S&U and PTT taxes. Recent data on national automobile inventories show a mere 39,800 vehicles in dealer inventory, the lowest level ever recorded since the data series began in 1993. Normal inventory levels are well over 1 million.

• Inflationary price increases will generally result in higher State tax receipts, except with taxes based on physical volumes, such as a large portion of the

transportation fuel taxes.

• FY22 Sales & Use tax receipts to date are very close to targets that assumed strong sustained growth. E-commerce continues to be a significant source of Sales & Use tax growth, after accelerating during the first year of the pandemic. The surge in Sales and Use tax receipts during the past three quarters implies a phenomenal increase in annualized taxable spending of more than $1.7B – a clear beneficiary of the Federal transfer and other pandemic-related payments.

• Cannabis tax revenues are included in this forecast for the first time. The tax consists of an excise tax shown as a new row in General Fund Tables 1 and 1A, and a Sales tax which is included in the Education Fund Sales & Use tax in Table 3. It is expected to yield at least $3.9M in GF revenues starting in FY23, with growth to $8.5M in FY24 and $11.1 in FY25. In addition to this, the Education Fund sales tax revenues from Cannabis should yield at least another $2.4M in FY23, $5.2M in FY24 and $6.8M in FY25. There is considerable uncertainty regarding revenue yields from Cannabis, as comparable state experience is highly variable and demand during the pandemic has soared, but may not be permanent.

• The U.S. and Vermont macroeconomic forecasts upon which the revenue forecasts in this update are based are summarized in Tables A and B on the following two pages, and represent a consensus JFO and Administration forecast developed using internal JFO and Administration State economic models with input from Moody’s Analytics December 2021 projections and other major forecasting entities, including the Federal Reserve, EIA, CBO, IMF, The Conference Board and other private forecasting firms with whom we interact.

Sources: Jeff Carr, Economic and Police Resources, Williston. Tom Kavet, Kavet, Rockler & Associates, Williamstown. 1.13.2022 Montpelier.