Now on its way to the governor’s desk, the pension bill did not receive a single ‘no’ vote as it worked its way through the House and Senate

Vermont Business Magazine The Vermont-NEA teachers union said today that by giving a final, unanimous nod to the framework for strengthening public worker pensions, lawmakers today reaffirmed their commitment to ensuring that teachers, state workers, and troopers have financial security after a career serving Vermonters. The Senate passed the bill 28-0 and the House passed it 144-0.

Governor Scott on Tuesday reiterated his frustration with the legislation that it did not contain an option for new hires to choose a "defined contribution" retirement plan, instead of just the existing, traditional plan.

The DC plan would be along the lines of a 401(k)-style investment plan typical in private employment. In answer to questions of why he would insist on it, the governor noted that the current plan is running up an unfunded obligation into the billions, but the current bill would pay down only part of that. The DC could save the state more money while giving new employees a more flexible retirement plan. Instead of "why" do it, Scott answered, "What's the harm? Put it in place, pretty simple."

On April 19, Scott said, "I’ve talked about the need for true structural reform to right the ship, because this is a massive $5.7 billion liability. And without structural reform it will only get worse." He said of the legislative proposal, "though it makes some positive steps, doesn’t go far enough and simply kicks the can down the road. I’m concerned that we’re putting a more than $200 million Band-Aid on this without fixing the underlying problems."

The pension plan, as passed by both bodies and sent to Governor Scott (S.286 – An act relating to amending various public pension and other postemployment benefits), according to the JFO: "is expected to reduce Vermont’s long-term unfunded retirement liabilities for state employees and teachers by approximately $2 billion by prefunding other post-employment benefits, modifying the pension benefit structure, and making additional State and employee contributions into the retirement systems."

“The message from the legislature couldn’t be clearer,” said Don Tinney, a high school English teacher who serves as the elected president of Vermont-NEA. “The governor can – and should – add his signature to this bill that was the product of more than a year of open, robust debate.”

The measure was crafted by the legislature’s Pension Task Force over the course of 17 open meetings and two public hearings. The task force included lawmakers, a member of the governor’s administration, a representative of the treasurer’s office, and six union members, including teachers Molly Stoner of Dummerston, Kate McCann of Montpelier, and Andrew Emrich of Waterbury.

“The unanimous support this bill got as it made its way through the legislature has been an honor to witness – as a member of the Pension Task Force and as an employee in Vermont’s public schools,” said Stoner, a fourth-grade teacher. “The complexity of the work and dedication of all involved has been inspiring; my hat is off to our legislators who work so hard on our behalf, to my courageous colleagues in education, state offices, and our troopers to the committed members of the Pension Task Force, and to all Vermonters willing to listening intently across aisles to find solutions to complex problems.”

Added McCann, a math teacher, “I want to extend my heartfelt gratitude for my fellow union members, the taskforce members, legislators from all parties, the Treasurer's office and Joint Fiscal Office for the courageous conversations and steadfast commitment that has led to a pension bill that preserves the defined benefit system for teachers, troopers, and state employees for decades to come.”

And Emrich, a kindergarten teacher, said, “After nearly seven months of collaborative and effective work with the Pension Task Force, we have almost come to the end without a single objection to one of the most significant bills of the past decade. I am extremely thankful for the dedicated work done by the legislative leaders, the passion and support shown from educators across our entire state, and an outcome that helps to provide a secure and dignified retirement for state employees, troopers, and Vermont's educators.”

After a technical review by legislative staff, the bill we be sent to the governor. He will then have the opportunity to sign it, veto it, or let it become law without his signature.

Joint Fiscal Office Summary

This legislation implements the final recommendations of the Pension Benefits, Design, and Funding Task Force created by the Legislature in Act 75 (2021). Based on preliminary actuarial estimates, the bill is expected to reduce Vermont’s long-term unfunded retirement liabilities for state employees and teachers by approximately $2 billion by prefunding other post-employment benefits, modifying the pension benefit structure, and making additional State and employee contributions into the retirement systems.

This bill contains a $200 million one-time General Fund appropriation in FY 2022 to the pension systems to pay down unfunded liabilities – $75 million to the Vermont State Employees’ Retirement System (VSERS) and $125 million to the Vermont State Teachers’ Retirement System (VSTRS). The bill also contains a $13.3 million one-time Education Fund appropriation in FY 2022 to the Retired Teachers’ Health and Medical Benefits Fund to begin prefunding health care benefits for retired teachers.

Overview of Legislation

Pension Provisions

S.286 includes the following pension-related provisions, which are proposed to take effect for the VSERS and VSTRS retirement systems beginning in FY 2023 (unless noted otherwise):

- • No changes to the benefits of current retirees, beneficiaries, or terminated vested members.

• State makes a one-time $200 million payment toward unfunded pension liabilities. The payment would be made in FY 2022 from reserved general funds and allocated $75 million to VSERS and $125 million to VSTRS. This payment is expected to immediately reduce the unfunded liabilities and improve the funded ratios. It is also expected to save interest costs and reduce the actuarially determined employer contributions (ADEC) in the future, with relative savings beginning in FY 2024 at approximately $19.5 million in total across both systems.

- • Higher employee contribution rates for active members of both systems, phased in over a 3- to 5- year period. By full phase-in, the higher contribution rates are expected to yield approximately $14 million (VSERS in FY 2027) and $10.3 million (VSTRS in FY 2025) of revenue, which would reduce the respective employer normal costs (which are paid through the ADEC) by a commensurate amount.

- • Modifications to the Cost-of-Living-Adjustment (COLA) formula for all employee groups, plus changes to other terms of the pension benefit for VSERS Groups C and D. The proposed changes are expected to yield approximately $58 million of unfunded liability reduction and $8.7 million of relative ADEC savings for VSERS, and $35 million of unfunded liability reduction and $4.8 million of relative ADEC savings for VSTRS.

- • Creation of a new VSERS pension group for certain Department of Corrections employees and other state employees who staff facilities for offenders, justice-involved youth, or patients in the care of the State. Per the Task Force recommendations, the Group G proposal is designed to be cost-neutral to the employer, with the cost to fund the enhanced benefit paid by active members of the group.

- • State commits to ongoing additional payments toward the unfunded liability. Beginning in FY 2024, an additional payment above the actuarially recommended amount would be included in the annual appropriation requests for the pension systems. The additional payment would increase to a maximum of $15 million per system by FY 2026 and remain in place until the respective systems reach 90 percent funded. This provision effectively reinvests a portion of the expected future cost savings from the $200 million one-time payment and pension modifications into further paying down the accrued unfunded pension liabilities.

Other Post-Employment Benefits (OPEB)

Sections 15, 24, and 25 contain language to prefund health care benefits (OPEB) for retired State employees and teachers. Currently, benefits for today’s retirees are funded on a pay-as-you-go basis with minimal prefunding. By prefunding, the State will realize a reduction of its unfunded liabilities by approximately $891.3 million for VSERS and $836.8 million for VSTRS due to the ability to discount liabilities using the 7.0% rate of return adopted by the Vermont Pension Investment Commission (VPIC) for the pension investments rather than the lower 2.2% rate that must be used in the absence of prefunding per government accounting rules. Prefunding will result in long-term savings from the ability to take advantage of compound investment gains over time to fund future benefits, but it will require higher expenses in the near term. In FY 2023, $15.1 million is needed from the Education Fund to begin funding the OPEB normal cost, and approximately $15 million of General Fund is needed across both systems to transition to prefunding. Other provisions of the bill, however, such as the proposed increases to employee contribution rates, COLA modifications, and the impact of one-time State contributions, are expected to result in future recurring savings in pension costs that will offset a substantial portion of the added fiscal impact from prefunding OPEB. Additionally, Section 26 proposes to repeal the July 1, 2023 sunset for the annual charge for teacher health care paid by Local Education Agencies per 16 V.S.A. § 1944d. This language continues the practice of LEAs making annual contributions toward OPEB costs for teachers hired after July 1, 2015.

Year-End Surplus Construct

Beginning with the close of FY 2023, Section 29 amends the existing statutory construct in 32 V.S.A. § 308c(a)(3) that dedicates 50 percent of unreserved and undesignated year-end General Fund surpluses to the Vermont State Employees’ Postemployment Benefits Trust Fund (VSERS OPEB). The bill would instead direct any such surpluses equally to the VSERS and VSTRS pension systems, with the VSTRS share dedicated to a newly created account to support future changes to retirement benefits when the VSTRS system is in a stronger financial position. It is not possible to accurately estimate the fiscal impact of this provision since the amount of unreserved and undesignated surpluses are subject to other spending decisions and actual end-of- year revenue collections which vary from year to year.

Other Provisions

Sections 16, 17, 18, and 27 propose clarifying amendments to several provisions enacted in Act 75 (2021) pertaining to the required frequency of experience studies and asset and liability studies for the three statewide pension systems. Act 75 stipulated that the Vermont Pension Investment Commission (VPIC) shall perform asset and liability studies on a three-year basis beginning on July 1, 2022. Act 75 further stipulated that the three Retirement Boards perform experience studies at least once every three years after the effective date of

the Act–the prior requirement was at least once every five years. The language in these sections clarifies, where appropriate, that the three-year cycle is defined as three fiscal years of actuarial data, not the three-year anniversary of the completion date of the most recent studies. The language also provides the VPIC and Retirement Boards with the option to delay the upcoming studies by a year in order to include FY 2023 data

in the studies. The most recent experience studies were based on the FY 2019 valuations. Without this change,

the next experience studies would cover data for the three fiscal years from FY 2020 through FY 2022 and omit many impacts from the proposed changes contained in this bill that take effect in FY 2023. The Vermont Municipal Employees’ Retirement System (VMERS) is outside the scope of the remainder of the bill, but this specific change is also proposed to apply to that system for the administrative convenience of having all three pension systems complete experience studies and review actuarial assumptions on the same schedule.

Modifications to the State Employees’ Retirement System (VSERS)

Proposed Pension Benefit Changes

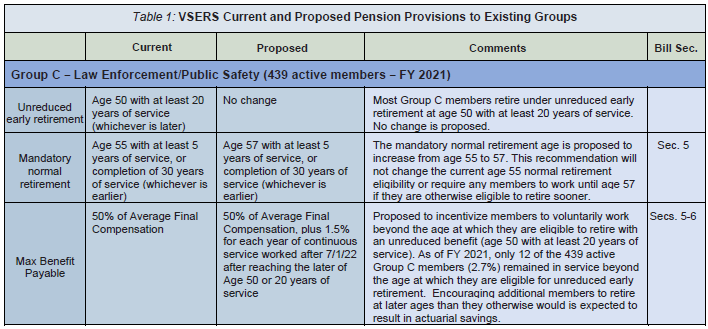

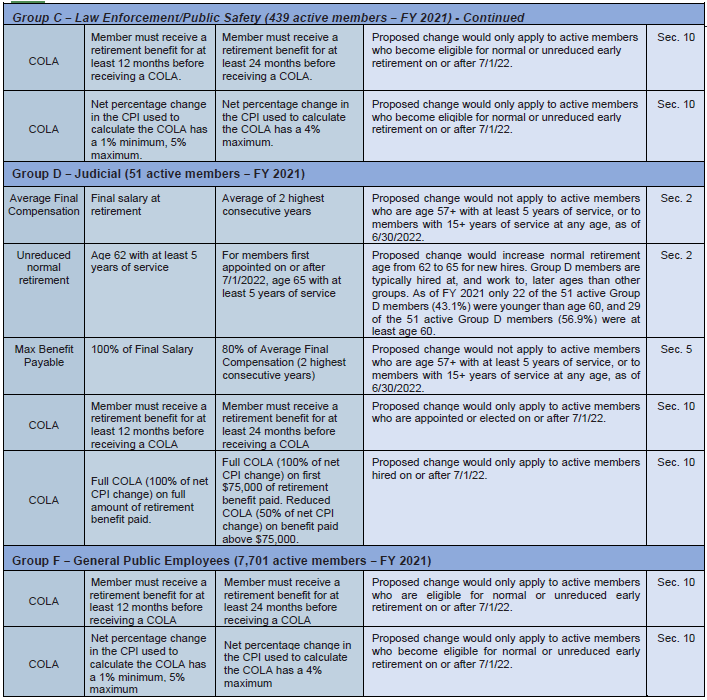

S.286 proposes numerous modifications to the pension benefit structure for VSERS active members (see Table 1). No proposed changes would impact current retirees, beneficiaries, or terminated vested members. Certain proposed changes would not apply to active members who are at or approaching eligibility for normal or unreduced retirement as of the effective date of the changes (July 1, 2022).

- Preliminary actuarial analysis commissioned for the Pension Task Force expects these proposed changes will reduce the State’s actuarially determined employer contribution (ADEC) by approximately $8.7 million and the VSERS unfunded liability by approximately $58 million. These impacts come primarily from the proposed changes to the COLA benefit, which are expected to lead to a change in the long-term actuarial assumptions used to calculate the normal cost and accrued liabilities. Reductions in the ADEC accrue to the funds of State government in proportion to those funds’ shares of the active payroll – approximately 40% typically falls to the General Fund, with the rest charged to federal and special funds.

Proposed Employee Contribution Rates

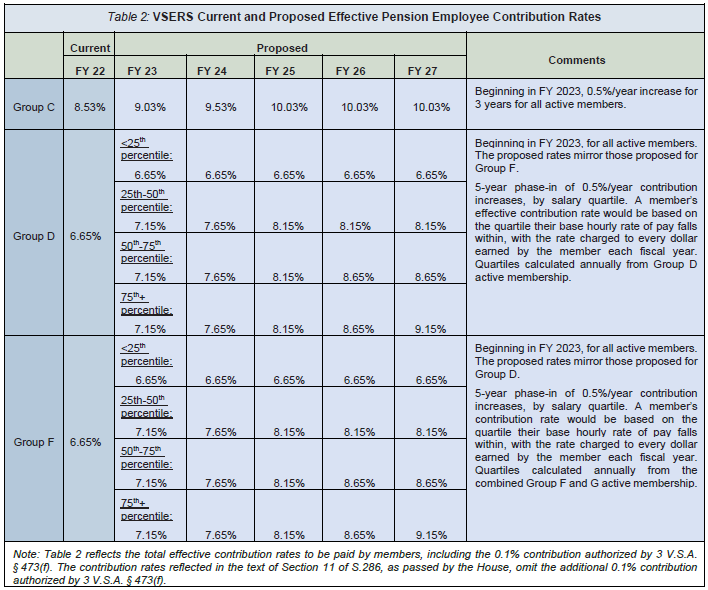

Section 11 proposes numerous modifications to the member contribution rates paid by active employees, beginning in FY 2023 (see Table 2 on the following page). Employee contributions are made on a pre-tax basis and revenue is credited toward the normal cost of the member’s future pension benefits (not toward the unfunded liability). Additional revenue raised through employee contributions reduces employer pension expenses (the ADEC) by paying a greater share of the total normal cost that would otherwise fall to the employer to pay.

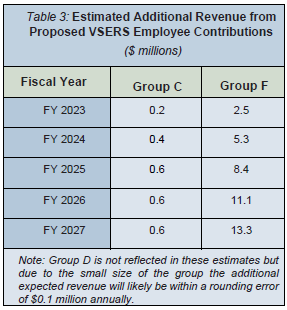

Preliminary actuarial analysis commissioned for the Pension Task Force expects these proposed changes will generate approximately $2.8 million of revenue in FY 2023, growing to approximately $14 million by FY 2027 when the proposed rates are fully phased in across all groups (see Table 3). Actual amounts may fluctuate from estimates, however, due to timing factors and fluctuations in the census and payroll characteristics of the active workforce.

Preliminary actuarial analysis commissioned for the Pension Task Force expects these proposed changes will generate approximately $2.8 million of revenue in FY 2023, growing to approximately $14 million by FY 2027 when the proposed rates are fully phased in across all groups (see Table 3). Actual amounts may fluctuate from estimates, however, due to timing factors and fluctuations in the census and payroll characteristics of the active workforce.

After full phase-in of the proposed rate structure (expected to occur in FY 2025 for Group C, and FY 2027 for Groups D and F), overall payroll growth is expected to increase at a long-term annual growth rate of 3.5%. Revenue from employee contributions, in turn, would expect to increase at a similar pace with the size of the overall payroll when all else is equal.

Note that actuarial estimates are based on the assumptions in place at the time of the analysis. Actual fiscal impacts are subject to change from preliminary actuarial estimates due to differences in timing, pension plan experience, future changes to long term assumptions, membership census, and demographic behavior. Estimates are preliminary and subject to revision from additional actuarial analysis.

4.29.2022. Montpelier. Vermont-NEA. JFO. 4.28.2022