by Timothy McQuiston, Vermont Business Magazine Vermont Auditor of Accounts today released his audit of Barre’s tax increment financing (TIF) districts. The audit found some glitches, as in the city slightly overpaid the state through a miscalculation and didn’t account for all properties within the district. These were fairly minor issues and did not result in much pushback from the city.

TIFs have been used mostly in the Northeastern part of the state. The most noticeable is Winooski, which has transformed its downtown commercial district. Burlington has used it for its waterfront and for the CityPlace redevelopment of the downtown mall, which is still very much a work in progress.

Usually the audit will find minor problems with a TIF and the municipality will seek to resolve them. The one notable exception to this was the TIF in St Albans in which the auditor in 2019 blasted the city’s use of the TIF. But nothing really came of it.

The complex TIFs allow approved cities and towns to retain some tax funds for a fixed period of time that would otherwise go to the state Education Fund. The Legislature has been reluctant over the years to expand the program because of those revenue implications. The last few administrations have encouraged them because of the economic development opportunities they offer.

The auditor does not have enforcement powers. It is required by law to conduct these TIF audits and offer recommendations as issues arise.

As for the Barre audit, the report states that as of FY2020, Barre has utilized $2.2 million in general obligation bonds for eligible TIF improvements and related costs. VEPC conditionally approved Barre’s FY2019 substantial request which increased the amount of improvements and related costs to be financed with TIF debt by more than $1 million, from $7,031,575 to $8,093,941. Barre has until March 31, 2024, to incur additional debt and must file updated information with VEPC when it is ready to complete the remaining TIF projects.

Barre was authorized to retain 75 percent of education and municipal tax increment. Since issuance of its first debt, Barre retained $689,469 of tax increment and accumulated $46,654 in interest earnings. Barre inadvertently made some errors in handling the list of properties and base values within their TIF district, which resulted in a calculation error.

This ultimately led to Barre retaining too little of tax increment and paying too much to the Education Fund.

Barre will need to increase tax increment retained in the TIF District Fund by $36,790 and receive a $20,962 credit on its the State Education Fund liability to rectify the FY2016 – FY2020 errors. Barre used $725,203 to repay outstanding TIF district debt and $6,867 to pay for TIF district related costs.

As of FY2020 year end, the TIF District Fund had $40,842 available for future use.

The report below is presented verbatim from the audit.

The full audit can be found HERE.

Barre City TIF Audit

Municipalities with a tax increment financing (TIF) district incur debt to finance infrastructure improvements and earmark a portion of incremental education and municipal property tax revenues from the district to repay the debt.

The Vermont Economic Progress Council (VEPC) approved Barre City’s TIF district on December 13, 2012, authorizing the use of incremental property tax revenue to finance $6,836,575 of infrastructure improvements plus $4,050,981 of financing costs. According to Barre's projections, the City expects to divert $4,438,000 from the Education Fund during its 20-year tax increment retention period. It is expected that it will take about 12 years after the retention period for the Education Fund to recover the diverted funds.

Our audit objectives were to determine 1) whether the City of Barre obtained required authorizations to issue its TIF district debt and used such debt to finance eligible improvement projects and related costs and 2) whether the City of Barre retained the appropriate amount of education and municipal tax increment in the TIF district fund and remitted the balance to the taxing authorities, as required for FY2018 – FY2020, and how the City used its tax increment.

Through FY2020, Barre issued $2,200,000 of bonds for public improvements as authorized by VEPC and approved by municipal voters and has fully utilized this debt to finance eligible TIF district improvements such as parking reconfiguration, streetscapes, storm water controls, land acquisition, environmental assessment, demolition, remediation and other allowable costs.

Due to some errors in properties included in the tax increment calculations from FY2016 – FY2019, the City retained too little education and municipal tax increment in its TIF district fund and overpaid the State Education Fund. The errors included an inadvertent omission of a property from the calculation of tax increment. To rectify the effect of the FY2016 – FY2019 errors, Barre will need to transfer $36,790 of additional tax increment to the TIF District Fund and seek reimbursement of $20,962 from the State Education Fund.

The City TIF used its tax increment to repay TIF district debt and cover some eligible related costs. The corrected balance of tax increment funds available for payment of debt service, related costs, or direct project costs in the future was $40,842 as of the end of FY2020.

We make several recommendations, including establishing and implementing annual TIF-related reconciliation procedures.

Tax increment financing (TIF) is a tool that municipalities can use to finance public infrastructure, such as streets, sidewalks, and storm water management systems. In Vermont, establishing a TIF district allows a municipality to designate an area for improvement, incur debt to finance public infrastructure, and retain a portion of growth in property tax revenues, called incremental property tax revenue. Incremental property tax revenues are used to repay the debt, and they include municipal property taxes (municipal tax increment) and statewide education property taxes (education tax increment). Thus, a portion of state education property tax revenue is retained by the municipality for authorized purposes rather than remitted to the State’s Education Fund.1

The City of Barre (Barre) Downtown TIF District (Barre TIF District) was approved by the Vermont Economic Progress Council (VEPC) on December 13, 2012 to use incremental property tax revenue to finance $6,836,575 of infrastructure debt plus $4,050,981 of financing costs. Through fiscal year (FY)2 2020, Barre issued $2,200,000 of bonds for public improvements. Barre is authorized to issue debt until March 31,20243 and to retain 75 percent of education tax increment through FY2034. Barre is required to allocate 75 percent of municipal tax increment for repayment of TIF district debt for the same period.

This audit is the first by the State Auditor’s Office (SAO) of the Barre TIF District, as required by 32 V.S.A. §5404a(l)(2).

This audit’s objectives were to determine:

1. Whether City of Barre obtained required authorizations to issue its TIF district debt and used such debt to finance eligible improvement projects and related costs; and

2. Whether the City of Barre retained the appropriate amount of education and municipal tax increment in the TIF district fund and remitted the balance to the taxing authorities, as required for FY2018 – FY2020, and how the City used its tax increment.4

Background

The purpose of a TIF district is to fund public infrastructure and stimulate economic development. A municipality designates a geographical area where it wants to encourage private sector development, and where the municipality thinks public infrastructure improvements are needed for that development. The municipality incurs debt to finance the needed public infrastructure improvements in the TIF which, in theory, stimulates private investment that would not otherwise have occurred in the designated TIF area.

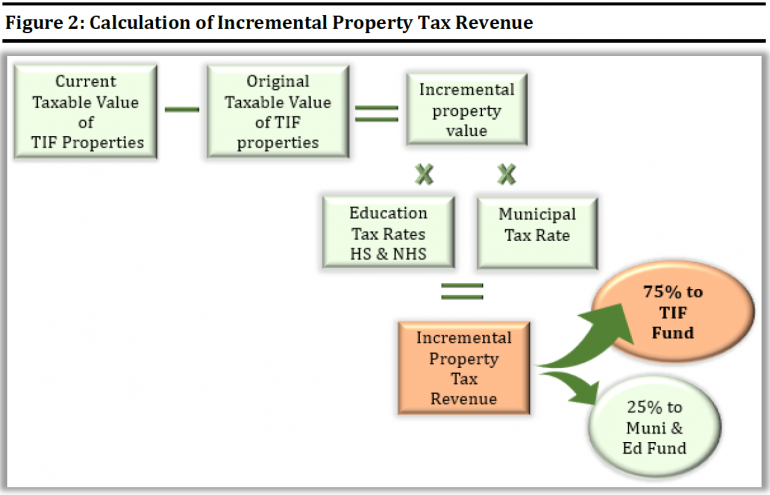

The combination of both public and private investment is expected to increase property values, generating property tax revenue. The expected growth in property tax revenues (i.e., incremental property tax revenue) in the designated area is used to pay debt incurred to finance the cost of improvements. The tax increment, comprised of education and municipal increment, is retained by the municipality for a maximum period of 20 years beginning the year in which the first debt obligation is incurred. Taxing authorities, like the municipality and the State (i.e., the Education Fund), continue to receive property tax revenue on the original taxable value (OTV) of the properties during this time.5 Figure 1 below shows the basic TIF model, including the anticipated tax increment.

TIF District Authorization and Oversight

The Vermont Legislature designated VEPC as the State body responsible for approving a TIF district after it is created and approved by a municipal legislative body.6

Since 2006, a municipality desiring to use incremental education property tax to finance TIF district improvements must file an application with VEPC. The application must contain both a district plan that has received prior approval from the municipal legislative body and a district finance plan. The district finance plan, which includes plans for debt financing, must be approved by VEPC before the municipality seeks a public vote to pledge the credit of the municipality (i.e., issue debt). Prior to seeking VEPC approval, a municipality must have held public hearings and established a tax increment financing district.

According to statute, VEPC conducts oversight and non-compliance enforcement of all districts. On May 6, 2015, VEPC adopted rules as required by statute to address issues related to creating, implementing, administering, and operating TIF districts.

TIF District Adopted Rules (TIF Rules) address VEPC’s oversight and monitoring of the TIF districts’ compliance with rule and statute, and enforcement of any aspects of non-compliance and resolution. 7

TIF District Debt and Tax Increment

After VEPC approves the use of incremental education property tax to finance TIF district improvements, the municipality must seek voter approval to incur debt to build public infrastructure improvements and pay for related costs. A municipality may issue debt for up to ten years from the creation date of the district if the first debt is issued before the fifth anniversary of the district creation date.8

The term “improvements” means the installation, new construction, or reconstruction of infrastructure that will serve a public purpose and fulfill the purpose of the district.TIF Rule 704, improvements may include, but are not limited to: transportation (e.g., public roads, parking lots, garages, streetscapes, and sidewalks), land and property acquisition, 9 According to TIF Rule 704, improvements may include, but are not limited to: transportation (e.g., public roads, parking lots, garages, streetscapes, and sidewalks), land and property acquisition, property demolition, site preparation, and utilities, such as wastewater, storm water, water dispersal and collection systems.

Related costs are defined as expenses incurred and paid by the municipality, exclusive of the actual cost of constructing and financing improvements, that are directly related to the creation and implementation of the TIF district.10 Per TIF Rule 705, examples of related costs include: 1) professional services incurred during preparation of a district plan, district finance plan, district application, or substantial change request; 2) costs of providing public notification about, and obtaining public approval for, a district plan, district finance plan, application or filing with VEPC; and 3) consulting, design, architects, engineering and other similar professional services costs directly related to the implementation and construction of eligible TIF district improvements.11

Tax increment may be used to pay TIF district debt and to directly pay for improvements and related costs. Municipalities with TIF districts approved by VEPC are authorized to retain 75 percent of the state education tax increment and are required to allocate at least the same proportion of municipal tax increment for repayment of TIF district financing.12 Education tax increment may be generated on Homestead (HS) and Non-Homestead (NHS) properties.13

Figure 2 illustrates the calculation of incremental property tax revenue. See below.

Some TIF Districts may distinguish its education OTV from its municipal OTV, in which case the calculation of education and municipal tax increments will be performed on two separate baseline values. Generally, the differences in the education and municipal OTVs are caused by local property tax agreements, where local voters have a discretion to provide additional property tax benefits to some property owners. Such agreements result in a property’s value set at its full assessed value for the purposes of the state education property tax and at a locally approved reduced value for the purposes of the municipal property tax.

TIF Districts and Statewide Education Funding

Municipalities, acting as agents of the State, collect state education property taxes. Rather than remit the taxes to the state Education Fund, municipalities pay local schools the education property tax liability determined by the Agency of Education (AOE). As a result, payments from municipalities to local schools are in effect payments to the Education Fund.

Municipalities are statutorily required to provide the Vermont Department of Taxes (VDT) with grand list data.14 VDT uses this data to determine the taxable education property value (EPV) and provides the EPV for each municipality to AOE. For municipalities with TIF districts, EPV excludes 75 percent15 of the incremental education property value of the TIF district, as allowed. The School Finance division of AOE uses EPV to calculate the amount of education property taxes each municipality owes its local school district and informs municipalities of their education property tax liability.

For those municipalities with TIF districts, EPV includes the portion of incremental education property value that corresponds to 25 percent of the education tax increment, which is required to be paid to the Education Fund.16

Municipalities are required to use New England Municipal Resource Center (NEMRC®), for the Grand List listing program, valuation and tax billing.17 NEMRC® includes a built-in TIF Module, which is used to account for TIF district properties, automate tax increment calculation, and produce TIF-related reports.

Although tax increment calculation is automated, its accuracy directly or indirectly depends on the completeness and accuracy of various information components, including:

• Property assessment values, listed on the grand list of the municipality,

• Certified TIF OTV,

• State Education Property Tax Rates,

• Municipal Property Tax Rate, including local agreement components.

These information elements originate at the municipal level and are reflected on various NEMRC® reports, including TIF Education and TIF municipal Parcel Value reports, which are provided to PVR for use in determining EPV.

Barre City TIF District

Pursuant to VEPC’s 2012 approval, the maximum dollar amount of debt obligations to be paid with incremental property tax revenues, including the cost of financing, is $10.9 million.

The City of Barre’s planned improvements include structured parking (i.e., parking garage) and streetscape. See Appendix III for descriptions of the VEPC-approved TIF infrastructure projects and changes in estimated costs to be financed with TIF district debt.

According to Barre's projections, through FY2034 the City expects to retain $4,828,000 of education tax increment for debt repayment. It is expected to take about 12 years to recover the $4,828,000 diverted from the Education Fund over Barre's 20-year tax increment retention period.18

Barre uses its TIF Fund to record costs of improvements and related costs financed with incremental property tax revenues. Debt proceeds, as well as debt repayment, are recorded in the fund.

Pursuant the TIF Rules Sec. 902, Barre TIF District went through the OTV certification in 2017, establishing its education OTV at $51,046,870 and its municipal OTV at $50,203,270.

Objective 1: $2.2 million of TIF district debt was authorized and used to finance eligible improvement projects and related costs

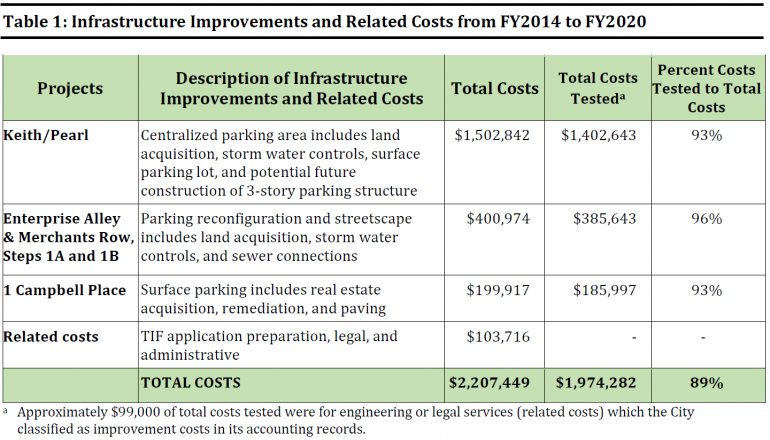

A $2.2 million general obligation (GO) bond issued by the City in August 2015 for TIF improvements and related costs was authorized by VEPC as part of the approval of the City’s TIF district December 2012. The GO bond was also authorized by municipal voters via a public vote held in November 2013. As of June 2020, the City had utilized all GO bond proceeds. We examined 89 percent of the TIF improvement project costs and related costs financed with the GO bond and concluded they were eligible to be financed with TIF district debt because the costs: 1) were authorized by VEPC and municipal voters as required by statute, 2) were for activities such as land acquisition and parking lot construction, which meet the definition of infrastructure improvements or related costs established in statute and the Adopted TIF Rules and 3) were approved in accordance with the City’s policies.

GO Bond Issuance Authorized by VEPC and Municipal Voters

VEPC approved the City of Barre’s TIF district plan on December 13, 2012 and its use of tax increment for $6,867,075 of improvements and related costs and an additional $4,050,981 of financing costs. The improvement projects to be financed included $4,462,500 for a centralized structured parking (i.e., parking garage) between Keith and Pearl Street and $2,374,075 for Merchants Row & Enterprise Alley parking reconfiguration and streetscape.

On October 24, 2013, VEPC also approved the City’s request (known as a substantial change request) to amend the approved TIF District Plan to 1) add a new project for acquisition, remediation and paving of a site at 1 Campbell Place at a cost of $195,000 and 2) install a surface parking lot on the site that was presented in the TIF district application as the site for a parking garage.19 In its request, the City stated that the installation of a parking lot does not preclude building structured parking in the future and VEPC concluded that surface parking was consistent with the need to develop parking in the downtown to encourage private sector development.

As required by 24 V.S.A. §1894(h), Barre held a public vote on November 5, 2013 and obtained municipal voter approval for the $2.2 million general obligation bond prior to issuing the debt for TIF improvements and related costs.

Barre City officials properly disclosed information required to be provided to the City's voters in advance of the public vote such as the type of debt to be issued, term of the debt, improvements and related costs that will be financed with the debt and expected private development. In addition, the City held a public meeting as required.

Eligible Costs Financed from FY2014 – FY2020

We examined $1,974,282 of infrastructure improvements and related costs financed with TIF district debt from FY2014 to FY2020 (89 percent of total costs financed) and concluded that costs during this period were eligible costs. Specifically, the costs align with the descriptions of and the total costs estimated for improvements described in the 2012 TIF district plan, the City’s 2013 substantial change request approved by VEPC, and an additional substantial change request conditionally approved by VEPC in 2019. The costs are also consistent with those disclosed in public notices provided to municipal voters in advance of public votes authorizing the City of Barre to incur TIF district debt. Further, the costs were for land acquisition, site remediation, streetscape, and surface parking lots and activities such as engineering that fit within the statutory and TIF Rules definitions of improvements and related costs.20 Lastly, the City generally followed its procurement policies and purchasing procedures.

Table 1 (above) describes improvements and related costs for the TIF district from FY2014 to FY2020 and the amounts we tested.

The City has until March 31, 2024 to incur additional debt to finance remaining planned improvements. The City’s 2019 substantial change request increased the amount of improvements and related costs to be financed with TIF debt by more than $1 million, from $7,031,575 to $8,093,941. See Appendix III for changes in cost for each improvement. In accordance with VEPC’s conditional approval of the request, the City must submit updated information on the remaining projects using the substantial change process when the city is ready to proceed.

Objective 2: Incorrect tax increment retained and paid to taxing authorities, but used for debt repayment as allowed

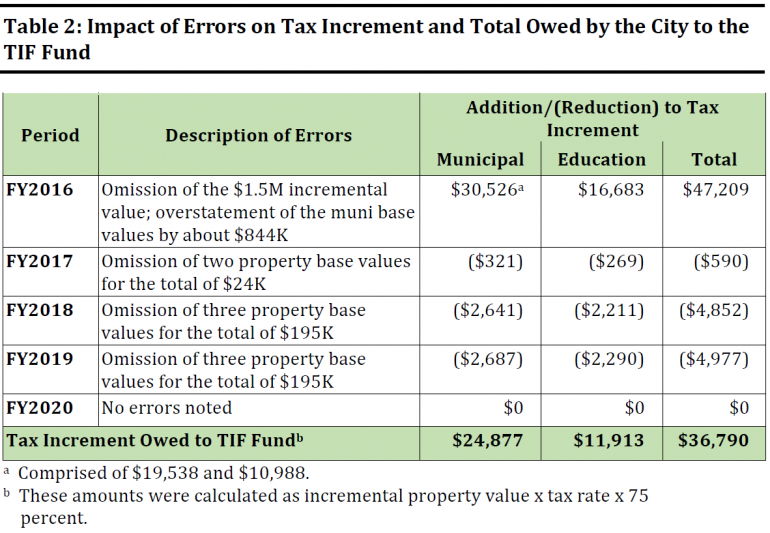

Through FY2020, the City of Barre retained $689,469 of tax increment in the TIF Fund but should have kept an additional $36,790. In addition, the City overpaid the share of tax increment required to be remitted to the local school district by $20,962. These inaccuracies were due to the omission of properties and incorrect original taxable value used in the calculation of tax increment from FY2016 to FY2019. Additionally, a reduction in assessed value for a TIF district property resulting from an appeal was not incorporated in the calculation of the amount the City owed the local school district. This occurred because the appeal resolution was settled after the AOE determined the amount the City owed to the local school district.21 Although there were mistakes in calculating tax increment and the amount owed to the school district, Barre City used tax increment plus interest income for debt service payments and related costs which are eligible uses. As of the FY2020 year-end, the corrected cumulative balance of Barre tax increment and interest income available for future use, was $40,842.

City Retained Too Little Tax Increment in TIF Fund and Remitted Too Much to the School District

As statute allows, Barre commenced its tax increment retention in FY2015.22 Since then Barre has recorded $689,469 cumulative tax increment in the TIF Fund, including $399,034 of municipal tax increment and $290,435 of education tax increment. Barre made several errors in the calculation of tax increment which resulted in too little tax increment recorded in its TIF Fund by $36,790, cumulatively. Some of the errors also affected the calculation of the amount the City owed the local school district. In total, Barre overpaid its school district by $20,962.

Errors that Impacted Tax Increment Recorded in TIF Fund

The most significant errors and their effects included:

Omission of a property from the NEMRC® TIF module in FY2016:23 Due to the omission of a property, the education and municipal incremental property values used in the tax increment calculation were understated by $1.5 million. As a result, the City recorded too little education and municipal tax increment in the TIF Fund, $16,683 and $19,538, respectively.

Barre officials could not explain what caused this error.

Erroneous substitution of municipal property base values with education base values for six properties in FY2016: Barre TIF district has six properties, for which each property has a different education and municipal base value.24 In total, the municipal OTV of these six properties was established at $843,600 lower than the education OTV. In FY2016, the municipal base value of all six properties was substituted with the education base values in error. As a result, the municipal OTV was too high by $843,600. Cumulatively, these base value substitutions caused an understatement of the municipal tax increment by $10,988.

Barre officials could not explain what caused this error.

Omission of property base values from the education and municipal OTV in FY2017 to FY2019: When the Barre TIF District OTV was certified by VEPC, PVR, and the City as required, the certified City TIF parcel listing incorporated some changes to OTV. However, the City failed to reflect these changes in the NEMRC® TIF module.

In one case, two missing base values, totaling $24,000, continued to be omitted from the NEMRC® TIF module in FY2017, FY2018 and FY2019.

In another case, the NEMRC® TIF module was missing a complete record of the property, including the base and the current list values. The City partially corrected the error, adding the property record to its NEMRC® TIF module in FY2018, however, that addition was made without a respective addition of $171,000 of its base value. This error was present in FY2018 and FY2019.

The base values omitted totaled $24,000 in FY2017 and $195,000 in FY2018 and FY2019. These omissions equally affected the calculation of the education and municipal tax increments. As a result, the City recorded too much tax increment in the TIF Fund.

These OTV omissions were identified by the independent City auditors in December 2019. At the time of the SAO audit, the City and PVR were in the process of reviewing the needed corrections.

Table 2 describes the errors, effect by fiscal year, and summarizes the additional $36,790 of tax increment owed to the TIF Fund.

The City records property tax receipts in its General Fund and periodically transfers the incremental municipal and education property taxes to the TIF Fund to record the amount of tax increment that may be retained each year. Since too little tax increment was transferred to the TIF Fund, an adjustment is required to transfer additional tax increment from the General Fund to the TIF Fund.

The two errors that impacted the amount of tax increment recorded in the TIF Fund in FY2016 also impacted the calculation of the amount of education property taxes (i.e., the education property tax liability) the City owed the school district. Additionally, the late settlement of an appeal of a property’s assessed value also impacted the amount owed to the school district.

Errors that Impacted Calculation of Amount Owed to School District

AOE calculates the amount of education property taxes each municipality owes its local school district based on taxable education property value (EPV) provided to AOE by VDT. For municipalities with TIF districts, EPV excludes 75 percent25 of the incremental education property value of the TIF district (e.g., the exemption) as allowed.

The following describes the City’s errors and the late settlement of a property tax appeal which impacted AOE’s calculation of the amount the City owed the local school district:

Omission of a property from the NEMRC® TIF module in FY2016: Because of this error, AOE used an EPV that was too high to calculate the amount of education property taxes the City owed the school district and Barre City overpaid by $16,645. Specifically, the exemption for TIF Non-Homestead incremental property value was understated by $1,125,000 (75 percent of the incremental property value of $1.5 million) in the EPV determined by PVR.26 Because the exemption amount was too low, the EPV was too high.

The City is required to upload grand list data via the Form 411 to PVR, including the exemption amount for the incremental education property value of the TIF district. However, a copy of Form 411, provided by the City to SAO did not agree with the information used by PVR and AOE and the City could not explain the discrepancy.27 Based on the information provided by Barre and PVR, it was not clear whether the data filed by Barre was erroneous or whether PVR used an outdated data upload to determine EPV. According to a Barre official, the error was discovered the following year and some discussions regarding this property omission were held with PVR; however, the error was not corrected. The official could not provide documentary evidence of the pertinent discussions but explained that based on their understanding, it was too late after the grand list final submission to correct the error.

To detect such errors timely, Barre could compare the EPV used by AOE to the City’s records. This can be done by the City confirming the Homestead and Non-Homestead grand list totals in the Cash Flow

Statement (form used to calculate education property tax liability for each municipality) prepared by AOE and provided to the City.

Omission of property base values from the education and municipal TIF OTV from FY2017 to FY2019: Because the OTV for certain properties was omitted from the NEMRC® TIF module, the incremental property value was too high and thus the exemption used by PVR to calculate EPV was too high.28 As a result, AOE used an EPV that was too low for the calculation of the amount of education property taxes the City owed the school district which resulted in the City paying too little.

Timing of a property tax appeal: A property assessment appeal that resulted in a $2.4 million reduction of the property taxable value was settled after the AOE issued its final calculation of the City’s FY2017 education tax liability.29 As a result, the EPV determined by PVR was too high.30 AOE used the overstated EPV, which resulted in the City paying too much to the local school district.

Barre could not produce a copy of the final grand list that was contemporaneous with the information submitted to PVR. A Barre official explained that the City reached out to PVR to see if an adjustment would be possible and stated that the request was denied. Barre did not retain documentation of the request to PVR or PVR’s response and it is not clear why a request for adjustment would be denied.31

Consistent retention of the contemporaneous data submission support records, timely reconciliation of the grand list amounts, presented on the AOE Cash Flow Statements with the respective City records and more proactive cooperation with the PVR and AOE in instances where large corrections are needed could have helped to identify grand list discrepancies.

Table 3 presents the effect of the errors on the education tax liability and the total owed by the Education Fund to the City of Barre.

AOE advised that it does not have statutory authority to initiate or make reimbursements from the State Education Fund, as such reimbursements are not one of the statutorily allowed uses of Education Fund resources. According to AOE, reimbursement from the Education Fund requires Legislative action. AOE suggested that the City seek a legislative remedy.

As noted above, Barre City officials were unable to explain the errors that occurred in FY2016 and did not retain copies of the various Forms 411 filed with PVR, so the cause of the errors is not clear. A report of changes to all municipal properties is available in NEMRC®. NEMRC® also has a change report specific to a TIF district, however, such report requires NEMRC® support to enable it. Barre City was not aware of this report, but when it was brought to their attention, Barre officials contacted NEMRC® and will be able to run TIF parcel comparison reports going forward. VDT is implementing a new integrated system to collect the statewide education grand list and to manage the statewide education property tax system. As a result, SAO suggested that VDT consider including a report of changes in TIF district properties in its system development requirements. Such a report would facilitate municipal review of changes to TIF district properties and we believe decrease the risk of errors that impact the tax increment and education property tax liability calculations.

Barre Used its Tax Increment Appropriately

Through FY2020, Barre used a combination of tax increment and interest income to pay $725,203 of debt service and $6,867 of related costs; both of which are eligible uses of tax increment and interest income earned per TIF Rule 714 and TIF Rule 912.32 The debt service payments included $677,848 of general obligation (GO) bond principal and interest, and $47,355 of BAN interest.

According to Barre calculations and the financial statements audited by independent public accountants, tax increment recorded in the TIF District Fund was less than the City’s debt payments. In addition to tax increment, Barre allocated interest earned on the BAN, GO bond, and tax increment to the TIF District Fund and used the interest earned to make up the shortfall in tax increment. In total, Barre recorded $46,654 of interest income in the TIF Fund.

In addition to debt service, Barre’s cumulative tax increment and interest income allowed Barre to cover about $6,867 of the TIF related costs, including annual audit fees.

Based on Barre’s calculation, the TIF Fund had about $3,000 of available cash at the FY2020 year-end. However, considering correction of the errors in the tax increment calculation noted in the previous section, as of the end of FY2020, Barre has $40,842 available for payment of debt service, related costs, or direct project costs in the future.

Descriptions of VEPC-approved TIF-funded infrastructure projects:

Structured parking: Centralized downtown parking area includes land acquisition, environmental assessment and removal of buried oil tank, creating a surface parking lot with an adjacent pedestrian walkway and potential future construction of 3-story parking structure.

Merchants Row & Enterprise Alley Streetscape: Parking reconfiguration and streetscape including land acquisition, storm water controls, and sewer connections.

Campbell Place: Centralized surface parking area including land acquisition, environmental assessment, demolition and remediation, site preparation and paving.

Recommendations

We make the recommendations in Table 4 to the City Manager of the Barre City.

|

Table 4: Recommendations and Related Issues Recommendation |

Report Pages |

Issue |

|

1. Establish and implement procedures, including maintenance of supporting documentation, for an annual reconciliation process between the City’s TIF district property records and the City’s property data used by PVR and AOE. Specifically, ensure the procedures include verification that 1) the TIF exemptions per the City’s final Form 411 submitted to PVR agrees to the TIF exemption stated on the City’s TIF Parcel Value report and 2) the total education grand list, after exemptions, per the City’s final Form 411 agrees to the EPV used by AOE for the education tax liability calculation. |

11,15 |

For several errors related to the calculation of tax increment, Barre officials could not explain what caused the error. In addition, Barre did not retain copies of the various Forms 411 filed with PVR, so the cause of the errors in the calculation of the education tax liability is not clear. |

|

2. Transfer $36,790 from the General Fund to the TIF Fund. |

10-12 |

Barre made several errors in the calculation of tax increment which resulted in too little tax increment recorded in its TIF Fund by $36,790, cumulatively. |

|

3. Retain documentation of Barre communication with VEPC and/or PVR, especially, in instances of error resolution. |

14 |

A property assessment appeal that resulted in an approximately $2.4 million reduction of the property taxable value was settled after the AOE issued its final calculation of the City’s FY2017 education tax liability. AOE used the overstated EPV, which resulted in the City paying too much to the local school district. Barre could not produce a copy of the final grand list that was contemporaneous with the information, submitted to PVR. A Barre official explained that the City reached out to PVR to see if an adjustment would be possible and stated that the request was denied. Barre did not retain documentation of the request to PVR or PVR’s response and it is not clear why a request for adjustment would be denied. |

1 Education funding is statewide and accounts for all the education taxes collected and spent in communities across the State. Municipalities collect statewide education property taxes on behalf of the State and remit the taxes collected to their local school systems, or to the state directly, depending on the amount collected relative to the amount required to fund the local school system.

2 Barre’s fiscal year is July 1 to June 30.

3 Act 73 (2021) Sec. 26a.

4 Appendix I details the scope and methodology of the audit. Appendix II contains a list of abbreviations used in this report.

5 Per 24 V.S.A. § 1891(5), OTV is the total valuation of all taxable real property located within the TIF district as of the creation date.

6 32 V.S.A. § 3325(a)(2) and 32 V.S.A. § 5404a(f)

7 32 V.S.A. § 5404a(j)

8 The Legislature provided for extensions for periods the debt may be issued – see Act 73 (2021) Sec. 26a.

9 24 V.S.A. § 1891(4)

10 24 V.S.A. § 1891(6)

11 Per TIF Rules Sec. 300, a substantial change is “an amendment to an approved District Plan or District Finance Plan which may result in a significant impact with respect to any of the criteria for approval by VEPC specified in 32 V.S.A. §5404a(h) and 24 V.S.A. Chapter 53, subchapter 5, or a request for an extension of the five-year period to incur indebtedness…” A request for substantial change must be submitted to VEPC for review.

12 TIF districts, approved by VEPC subsequent to 2017 (Act 69 (2017) Sec. J.3., amending 24 V.S.A. §1894(b) and (c)), may retain 70 percent of the education tax increment and are required to allocate 85 percent of the municipal tax increment to repay TIF district debt. A municipality may retain more than 85 percent of the municipal tax increment to service its TIF district debt.

13 32 V.S.A. § 5401 defines ”Homestead” to mean the principal dwelling and parcel of land surrounding the dwelling, owned and occupied by a resident individual as the individual's domicile or owned and fully leased on April 1, provided the property is not leased for more than 182 days out of the calendar year, or for purposes of the renter property tax credit under subsection 6066(b) of this title, is rented and occupied by a resident individual as the individual's domicile.

14 The grand list data forms the basis for the collection of property taxes for all the municipalities in Vermont and includes the owner’s name and assessed value for all real estate parcels, all taxable personal estates, and tax-exempt properties.

15 Per Act 69 (2017) Sec. J.3, future TIF districts approved by VEPC may only retain 70 percent of the incremental education property value.

16 For municipalities with TIF districts approved by VEPC subsequent to 2017 (Act 69 (2017) Sec. J.3., 24 V.S.A. §1894(b) and (c)), EPV includes 30 percent of the incremental education property value.

17 The Department of Taxes, Division of Property Valuation and Review is implementing a new integrated system to manage the statewide education property tax system – the Integrated Property Tax Management System (IPTMS). The IPTMS is scheduled to go live in Q2 of 2022.

18 Estimate of number of years is calculated using the total education increment projected to be retained divided by the amount expected to be retained in the final year. Specifically, $4,828,000/$395,000 = 12 years.

19 24 V.S.A. §1901(2)(B) requires any proposed substantial changes to the approved TIF district plan and approved TIF financing plan be submitted to VEPC for review.

20 24 VSA 1891(4) and TIF Rules Sec. 300 and Sec. 704.

21 AOE calculates the amount of education property taxes each municipality owes its local school district, based on a municipal submission of final Form 411 to PVR, which, in turn, comes to AOE in form of education property value (EPV) amounts.

22 Barre City TIF District incurred its first debt in January 2014. Accordingly, its tax increment starts on April 1, 2014 Tax Year (FY2015) and extends 20 years or through April 1, 2033 (FY2034).

23 Initially we designed this audit to cover FY2018 – FY2020. Our analyses indicated some issues with how certain properties were handled in earlier years of the TIF District and we expanded the audit scope for tax increment to FY2016.

24 The differences exist when a municipality votes to exempt a property from the grand list or stabilize the value or taxes on a property, but the exemption or stabilization does not affect the property’s education taxable value.

25 Per Act 69 (2017) Sec. J.3., future TIF districts approved by VEPC may only retain 70 percent of the incremental education property value which means only 70 percent will be excluded from the calculation of EPV.

26 As noted in the previous section, the omission of this property also impacted the calculation of tax increment.

27 The Final 411, retained by the City did not match the PVR EPV tables for Barre City, which, by design, should be the same.

28 These are the same properties described in the section regarding errors in tax increment calculation.

29 The property assessment appeal was finalized on April 12, 2017; the AOE Final Cash Flow Statement dated March 22, 2017.

30 The appeal changed property assessment from $4 million to $1.6 million. The TIF Non-Homestead exemption decreased from $3.6 million to $1.2 million. Barre correctly used the post-appeal value for its tax increment calculations, and it required no changes.

31 Per PVR and AOE, currently there are no mechanisms to make any corrections to the issued finalized education tax liability calculations without legislative action.

Source: Auditor of Accounts. Montpelier. 7.20.2021 https://auditor.vermont.gov