Jeff Carr and Tom Kavet presented their consensus revenue report to the Emergency Board Thursday at the Governor's Ceremonial Office in the State House. VBM photo.

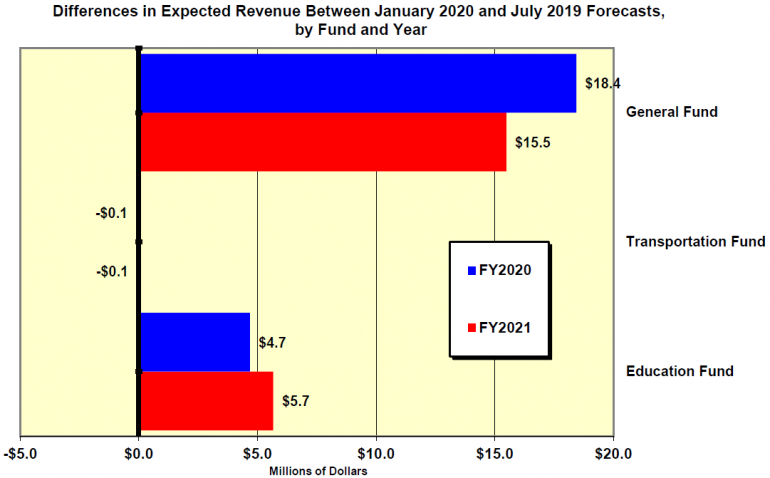

by Timothy McQuiston, Vermont Business Magazine The governor and key legislators received, as expected, good tax revenue news today. Economists Jeff Carr (for the Administration) and Tom Kavet (for the Legislature) issued their consensus projections showing that General Fund revenues should be $18.4 million ahead of the current year expectations and $15.5 million ahead for next year.

While Carr (Economic & Policy Resources of Williston) and Kavet (Kavet Rockler & Associates LLC of Williamstown) acknowledged that a recession will come at some point, they noted that, unlike the scare of just one year ago, there is no downturn likely in the near term nor one apparently lurking on the horizon.

“Recoveries just don’t die of old age,” Kavet told the Emergency Board.

The E-Board is chaired by Governor Phil Scott and is comprised of the chairs of the legislative money committees: Representatives Janet Ancel (Ways & Means) and Kitty Toll (Appropriations) and Senators Jane Kitchel (Appropriations) and Ann Cummings (Finance).

While the General Fund, with a resurgent personal income tax, continues to show strength, the Education Fund also is expected to beat previous expectations by $4.7 million this year (FY20) and by $5.7 million next year (FY21). This performance is largely based on the sales & use tax, which bounced back in 2019 after several years of sluggish performance.

However, the Transportation Fund continues to slog along compared to the other two major funds. It’s projected to be off by $100,000 this year and next from expectations Carr and Kavet calculated last July. While this is just a hair off from their previous report, the TF has had low expectations in recent years as the gasoline tax has been down and new car sales have been off.

Kavet Report

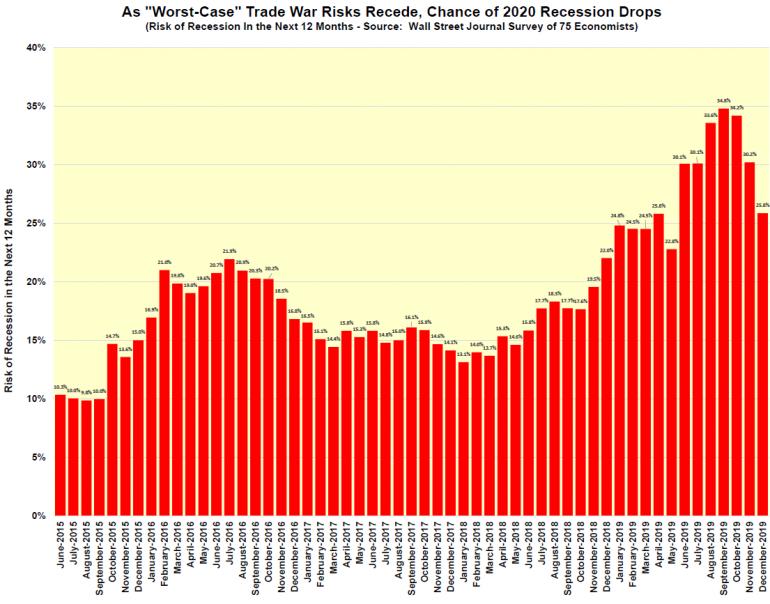

After rising recessionary concerns throughout most of 2019, the year ended on a positive note, with a “worst case” trade war with China seemingly averted, House approval of the slightly-revised NAFTA agreement (now called USMCA), the stock market soaring to record heights, bipartisan agreement on funding the federal government (no matter how big the deficits), and stabilizing global economic conditions. Accordingly, year ahead recession risks as measured by a Wall Street Journal survey of economists, has fallen from 34.8% in September to 25.8% in December.

Vermont revenues in the first half of FY20 have been slightly above expectations in all major funds, with the G-Fund excluding Healthcare about +1.4% above targets, the T-Fund, +0.5%, the E-Fund, +0.8%, and Healthcare, +5.2%. As a result of both technical and economic factors, total revenues from the funds analyzed herein will be about $23M higher in FY20 and $21M above FY21 levels estimated in July, a minor midcourse correction of about 1%.

Labor markets remain relatively tight in both the U.S. and Vermont, with each posting sustained unemployment rates in recent months close to their lowest levels ever. Vermont’s unemployment rate, at 2.3% in November (the latest available), was again the best in the nation, while the U.S. rate in both November and December, at 3.5%, was the lowest in more than 50 years. Even more broadly-measured unemployment rates, such as “U4” which includes discouraged workers, “U5” which adds marginally attached workers, and “U6” which adds those employed part time for economic reasons, all reached record U.S. lows (since their construct in 1994) in December.

U.S. payroll jobs set another record in December, registering the 111th consecutive monthly increase – the longest stretch in 80 years of data. Also, of note in the latest month, for only the second time ever, women held more jobs than men – a reflection of the faster relative growth in sectors such as healthcare and education, which women dominate. Service sector employment in 2019 grew 1.5%, while Goods producing job growth was only 0.8%, hobbled by tariffs and trade uncertainty.

As strong as labor markets appear, U.S. job growth in 2019 was the weakest since 2011 and nominal wage growth actually decelerated through most of the year, dropping from a peak of 3.4% in February to 2.9% in December. Underscoring the stark relative weakness of workers vs. employers, even in labor markets experiencing record unemployment, real wage growth in 2019 never reached 2% and in December slowed to a mere 0.6%.

As the expansion ages, growth rates are expected to slow. 2019 U.S. GDP growth is forecast to be about 2.3%, while 2020 and 2021 are likely to be at or slightly below 2%. The unemployment rate will move up a few ticks, but remain historically low, at 3.8% in 2020 and 4.1% in 2021.

Real estate and housing markets benefitted in 2019 from a swing away from Federal Reserve monetary tightening that had choked this sector in late 2018 and slowed transactions and price appreciation in most regions. With three interest rate cuts in 2019, real estate markets have revived and price appreciation is currently well above inflation.

In the latest quarter (2019:Q3), Vermont posted 4.3% year-over-year home price growth, trailing Maine (+5.9%), New Hampshire (+5.2%), New York (+4.5%) and Rhode Island (+4.4%) in the region. Idaho is currently the hottest housing market in the nation, with eight consecutive quarters of double-digit price growth. Such unsustainable runs can only end in one way…

For the 22nd consecutive quarter, housing prices increased on a year over year basis in virtually every U.S. state. As of the third quarter of 2019 (the most recent available), 43 states equaled or exceeded their pre-recession peak levels. Only 7 states were still below their pre-recession peak prices: NV, RI, DE, IL, NJ, MD and CT.

Notably, Connecticut has the worst housing market in the nation, with prices still almost 12% below pre-recession levels. Rhode Island (-1.5%) is close to pre-recession levels, with Vermont at +9.3%, NH at +7.8%, NY at +12.6%, Maine at +13.5% and MA at +15.3%.

After more than 10 years, Vermont real estate prices outside the Burlington MSA finally exceeded their pre-recession peaks (+2.2%). Meanwhile, the Burlington MSA – like many urban areas – has had price increases that are nearly 20% above prior peaks.

Through 2018 (the latest available data), the Vermont counties with the worst housing markets have been in the southern part of the State – where second home ownership is more heavily weighted to CT residents. Until the CT market returns to at least its pre-recession level, there will be very limited wealth effects from primary home equity and, even more important, there will be a searing memory that property ownership can be a losing financial proposition. Both of these effects may dampen second home ownership in southern Vermont in the near-term.

Despite the record longevity of the current economic cycle, and the certainty that there will be another downturn at some point, business cycles don’t die of old age. They usually die from either internal imbalances that are unsustainable and result in correction and rebalancing, or external shocks. So, how long could the current expansion keep going? If we look beyond our own borders, there are three economies that are currently experiencing economic expansions that have lasted longer than ours - with two of them more than twice as long. Australia has seen sustained growth for 112 quarters (since 1991), South Korea, for 85 quarters (since 1998) and Poland, for 73 quarters (since 2001). There are also eight other instances in the post-war period in which nations have had longer expansions.

The caveat here is that the wildfires that have stricken Australia in recent weeks could lead to a recession, but that will not be known for some months.