Vermont Business Magazine The $6 billion state FY20 budget bill (H542 state budget) passed with overwhelming support this year. By the end of April, general fund tax revenue projections for FY19 were a whopping $50 million more than projected, which held through the May report and are expected to finish the fiscal year on June 30 at about that number. Lawmakers decided to dedicate a portion of the rooms and meals tax to the clean water fund and backfill the hole with the projected surplus funds rather than raise new taxes. Key areas of investment in the budget include early childhood education, workforce and economic development and programs to combat climate change.

Summary courtesy Leonine Public Affairs, Montpelier (See full JFO revenue report below)

H.514 - MISCELLANEOUS TAX

The Miscellaneous Tax Bill (H.514) makes various administrative changes to state tax laws that are estimated to raise $170,000 in revenue in FY20. The bill includes a provision clarifying that auto parts used by auto dealers to recondition used vehicles for resale will continue to be exempt from the sales tax. H.514 also revises the way, for the purposes of the state’s corporate income tax, income earned by companies that provide services in multiple states is to be allocated to Vermont. Currently Vermont uses the “cost of performance” methodology whereby income is allocated to the state where the company incurs the most costs in providing services. Under H.514, Vermont will switch to a “market based sourcing” methodology, that looks at the amount of sales made in the state. This change is likely to benefit Vermont-based service providers and increase the corporate income tax liability of out-of-state service providers.

Here is a link to the fiscal note for H.514 with more detail.

H.541 - REVENUE BILL

The revenue bill (H.541) makes changes to Vermont’s tax laws and is estimated to generate $4.83 million in state revenue in FY20. Some key provisions in the bill include limiting the capital gains exclusion, creating a new deduction for limited medical expenses within the personal income tax, increasing the estate tax exclusion over two years from $2.75 million to $5 million by January 1, 2021 and imposing taxes on travel agencies such as Expedia.

Here is a link to the Fiscal Note for H.541 with more detail.

Representative Heidi E. Scheuermann (R-Stowe) issued her take on FY2020 taxes:

Education Funding and Property Taxes

The Fiscal Year 2020 budget includes $14 million to buy down the property tax increase that is necessary due to the increase in school spending throughout the state. Spending had been predicted to increase 3.2%, but school budgets came in higher than that, so the spending increased by 4%.

In order to keep the property tax increase at just 1 cent per $100 of property value, $14 million is being used to fill the hole.

Increased spending is a direct result of our funding system. Until we comprehensively reform the education funding system, we will not see a financially sustainable pre-k - 12 education system. No amount of forced mergers of districts like Stowe and EMUU is going to save money, unless and until we reconnect voters to the budgets voted upon and money spent.

Like our education funding system in general, this tax rate buy-down is unsustainable, and, while it is appreciated to keep taxes lower than they would be otherwise, it cold mean a spike in property taxes next year.

As is the case every year, numerous proposals to increase taxes on Vermont families and businesses emerged to fund pet projects. In the end, though, there was a tax package that actually included some positive changes:

-

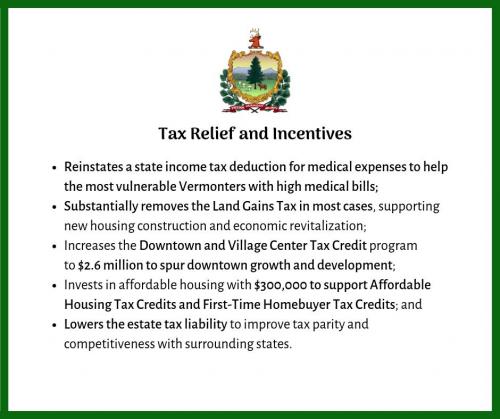

An increase in the estate tax exclusion from $2.75 million to $4.25 million in January 2020, and $5 million in January 2021;

-

An expansion of the Downtown Tax Credit Program from $2.4 million to $2.6 million;

-

The institution of a deduction for medical expenses within the personal income tax that will allow Taxpayers to deduct any medical expenses beyond Vermont's standard deduction and personal exemptions (with some exceptions);

-

The expansion of the cap on the Affordable Housing Tax Credit and the First-Time Homebuyer Tax Credit to $125,000 each;

-

A change in the definitions of "operator" and "rent" to include Online Travel Agencies, to ensure the OTAs remit to the state the entire tax collected from the client; and

-

Changes to the Land Gains Tax such that it would apply to a much smaller number of transfers - only land subdivided by the transferor within 6 years prior to the sale or exchange would be subject to it, and it exempts land transferred in a downtown, village center, or new town center.

Unfortunately, the tax bill also included a decrease in the Capital Gains Exemption by capping the exemption at $350,000. This change will have a considerable impact on some of our state's small businesses and their families.

Here is a graphic with Governor Phil Scott's bullet points:

Vermont Legislative Joint Fiscal Office |

May 23, 2019

H.541: An act relating to changes that affect the revenue of the State- Committee of Conference

Bill Summary

This bill makes numerous changes to various state revenue sources. These include:

- Limiting the capital gains exclusion to $350,000 in total capital gains exclusions. This would effectively limit the exclusion to capital gains of $875,000 or less.

- Creating a new deduction for medical expenses within the personal income tax. Taxpayers could deduct any medical expenses beyond Vermont’s standard deduction and personal exemptions. This deduction would be limited for entrance and monthly fees for continuing care retirement communities.

- Increasing the estate tax exclusion over two years. Beginning January 1, 2020, the estate tax exclusion rises from $2.75 million to $4.25 million. On January 1, 2021, the exclusion rises to $5 million.

- Expanding the cap on the Affordable Housing Tax Credit and the First Time Homebuyer Tax Credit by $125,000 each.

- Expanding the cap on the Downtown and Village Center Tax Credit program from $2.4 million to $2.6 million.

- Changing the definitions of “operator” and “rent” to include online travel agencies (OTAs) and their associated transaction fees or commissions.1

- Expanding the tax base for the Property Transfer Tax and Clean Water Surcharge to include transfers of controlling interests in a property. This would include property transfers where a business or entity takes a majority ownership stake in a property without a title change.

- Making significant changes to the Land Gains Tax such that it would apply to a small number of land transfers. Only land subdivided by the transferor within six years prior to the sale or exchange would be subject to the tax. This section also exempts land transferred in a downtown development district, a village center, or new town center development.

- Extending the sunset on the Fuel Tax for 5 years and expands the base to include any nonprofit agency and any governmental entity in Vermont.

- Extending the sunset for the health information technology tax to July 1, 2021.

- Extending the sunset for Home Health Provider Tax to July 1, 2021.

Fiscal Impact

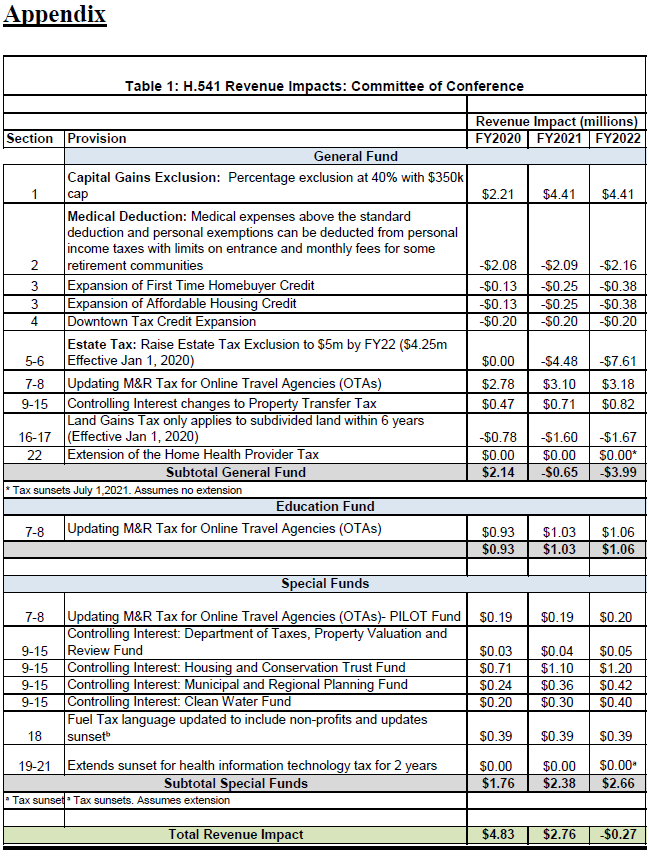

This bill would generate an additional $4.83 million in total State revenues in FY20. This revenue impact is spread across different funds:

- $2.14 million in General Fund revenues.2

- $930,000 in Education Fund revenues.

- $1.76 million in special fund revenues

2 H.532 (Budget Adjustment) also contains a change to the distribution of funds from the Department of Taxes Computer Modernization Fund to the General Fund from 80% to 40%. That change generates an additional $4.8 million for the General Fund. The House Budget bill furthers that change from 40% to 30% generating an additional $1.2 million.

Within the General Fund, the revenue impacts of the bill in FY2020 are the following:

- Sec. 1 (Capital Gains): +$2.21 million

- Sec. 2 (Medical Deduction): -$2.08 million

- Sec. 3 (First Time Homebuyer and Affordable Housing Tax Credit): -$0.25 million

- Sec. 4 (Downtown Tax Credits): -$0.2 million

- Secs. 5-6 (Estate Tax): No impact in FY20

- Secs. 7-8 (Online Travel Agents): +$2.78 million

- Secs. 9-15 (Controlling Interest Property Transfer Tax): +$0.47 million

- Secs. 16-17 (Land Gains Tax): -$0.78 million

- Sec 22 (Home Health Provider Tax sunset extension): No impact

Within the Education Fund, the revenue impacts of the bill in FY2020 are the following:

- Secs. 7-8 (Online Travel Agents): +$0.93 million

The bill also impacts numerous special funds in FY2020:

- Secs. 7-8 (Online Travel Agents): +$0.19 million to the PILOT Fund

- Secs. 9-15 (Controlling Interest Property Transfer Tax):

o +$0.03 million to the Department of Taxes Property Valuation and Review Fund

o +$0.71 million to the Housing and Conservation Trust Fund

o +$0.24 million to the Municipal and Regional Planning Fund

o +$0.20 million to the Clean Water Fund

- Sec 18 (Fuel Tax): +$0.39 million to the Weatherization Fund

- Secs 19-21 (Health Information Technology tax sunset extension): No impact

Table 1 in the Appendix provides projections of these revenue impacts in FY 2021 and 2022.

Explanation/Methodologies

Section 1: Limiting the percentage exclusion within the Capital Gains Exclusion to $350,000.

Vermont currently allows income taxpayers to exclude a portion of their capital gains from their taxable income. Taxpayers can either exclude up to $5,000 of capital gains or 40% of their capital gains on realized gains on certain assets, mainly businesses, farms, or investment properties.

Section 1 of the bill limits the amount of capital gains a taxpayer can exclude to $350,000, effective July 1, 2019. This section is expected to generate an additional $2.21 million in FY20. A full year of implementation increases the additional revenue to $4.41 million in FY21 and FY22.

Sources: Chainbridge Tax Model based upon 2016 tax year data.

Section 2: Creation of a new Vermont medical expenses deduction

Under current law, Vermont taxpayers are eligible to take a Vermont standard deduction (equal to $6,150 for a single taxpayer and $12,300 for a married taxpayer) and personal exemptions for themselves, their spouses and any dependents (equal to $4,250 per exemption). No other deductions, including Federal itemized deductions, are allowed.

This bill creates a new deduction that would allow taxpayers to deduct medical expenses on their Vermont personal income tax return. This deduction is equal to any expenses deducted at the Federal level (which is subject to a 10% Adjusted Gross Income floor) minus the Vermont standard deduction and personal exemptions.

The bill also creates limits on expenses that can be deducted. Entrance and monthly fees for residents of a continuing care retirement community (as defined by 8 V.S.A. § 8001(5)) will only be deductible up to the equivalent deduction allowable at the Federal level for long-term care insurance.

For example, for a married taxpayer (with no children) with $100,000 in Adjusted Gross Income, and $50,000 in medical expenses, the deductible amount would $18,900: $50,000 minus $10,000 (10% Federal AGI floor) minus $12,600 (VT standard deduction) minus $8500 (2 x $4250 per personal exemption).

This section is expected to decrease revenues by $2.08 million in FY20, growing in future years.

Source: Chainbridge Tax Model based upon 2016 tax year data.

Section 3: Expansion of the Affordable Housing and First Time Homebuyer Tax Credits

Section 2 of the bill expands two existing credits administered by the Vermont Housing Finance Agency (VHFA): the Affordable Housing Tax Credit and the First Time Homebuyer Tax Credit.

The current first year credit allocation for the Affordable Housing Credit is $300,000 for a maximum limit of $1.5 million over any 5 year period. The bill proposes to raise the first year credit allocation to $425,000, for a maximum 5 year allocation of $2.125 million.

The current first year credit allocation for the First Time Homebuyer Tax Credit is $125,000. This section of the bill raises the first year credit allocation to $250,000 and extends the program through FY2026. Because the program was set to expire in FY22, all credits awarded thereafter would be new fiscal cost relative to current law.

Both of these tax credits are 5 year tax credits, meaning a claimant claims the credit for 5 consecutive years. As such, the total credits awarded in a given year are the current year’s first year credit allocation, plus any credits from the previous five years. For any increase in the size of first year credit allocations, the cost increases each year by the size of that increase over the next five years.

The FY20 cost of increasing the first year credit allocations of the Affordable Housing Tax Credit and the First Time Homebuyer Tax Credits is $125,000 each, for a total of $250,000. However, in FY21, the cost is FY20’s second year cost ($250,000) plus the first year costs in FY21 ($250,000) for a total cost of $500,000. This continues over the next five years. Table 2 details the complete cost of the expansions over the next 5 fiscal years.

Sections 5 and 6: Raising the estate tax exclusion

Currently, the estate tax is 16% on the value of any estate over the exclusion amount of $2.75 million

The bill proposes to raise the estate tax exclusion over the course of two years. Beginning January 1, 2020, the estate tax exclusion rises from $2.75 million to $4.25 million. On January 1, 2021, the exclusion rises to $5 million.

Relative to current law, raising the exclusion is expected to have no fiscal impact FY2020. In FY2021, the cost increases to $4.48 million, increasing further to $7.61 million in FY2022 once the exclusion is fully phased-in.

Sources: Department of Taxes data, January 2019 Consensus Revenue Forecast.

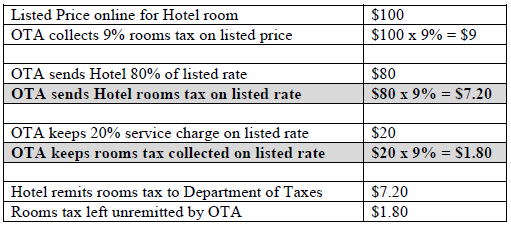

Sections 7-8: Online Travel Agencies (OTAs)

Under current law, online travel agencies3 (OTA) themselves are not required to remit the 9% rooms tax. In a typical transaction, when a customer reserves a room through an OTA, the OTA collects the 9% tax on the listed price of the room. The OTA then forwards an agreed-upon room rate to the operator (which is often 15-20% less than the listed room rate) plus the 9% rooms tax on only that agreed-upon rate. The operator remits the 9% tax on the agreed-upon rate to the Department of Taxes. The OTA keeps the 9% rooms tax on the difference between the listed rate and the agreed-upon rate.

The following example illustrates this process:

This section requires OTAs (“booking agents”) to remit the rooms tax on all amounts collected by the OTA. In the example above, the OTA would be required to collect and remit to the Department of Taxes both the $7.20 it was previously sending to the Hotel, but also the $1.80 in rooms tax it was previously keeping.

JFO estimates that requiring OTAs to collect and remit rooms tax on all amounts listed by the OTA will generate approximately $2.8 million in additional meals and rooms tax revenue in FY 2020 and growing in future fiscal years. 75% of this revenue will go to the General Fund and 25% will go to the Education Fund.

In addition to this revenue, the section also requires booking agents to remit the rooms tax on all amounts collected at the point of sale. Booking agents include websites that list short-term rental properties, in addition to websites that list traditional hotels and motels. Under current law, rooms tax is due on short-term (or any) rentals if the operator rents the room for greater than 15 days in a calendar year, and remittance of the tax is the responsibility of the operator, not the booking agent. The Department of Taxes and JFO have estimated that there is 40% noncompliance4 amongst short-term rentals who use booking agents other than AirBnB5. This section would require booking agents to collect on behalf of those noncompliant operators.

JFO estimates that closing the noncompliance gap amongst short term rentals would generate an additional $1 million in rooms tax in FY 2020 and growing in future fiscal years. 75% of this revenue will go to the General Fund and 25% will go to the Education Fund.

In total, JFO estimates that in total, this section of the bill will raise rooms tax revenues by $3.8 million in FY2020, growing to $4.2 million in FY21 and $4.4 million in FY2022. 75% of this revenue will go to the General Fund and 25% will go to the Education Fund.

Sources:

These estimates relied upon the following sources:

- Pennsylvania estimates on HB1511 of 2018

- 2017 Tourism Benchmark Report, Vermont Department of Tourism and Marketing6.

· Lodging Magazine

- Department of Taxes data

- January 2019 Consensus Revenue Forecast

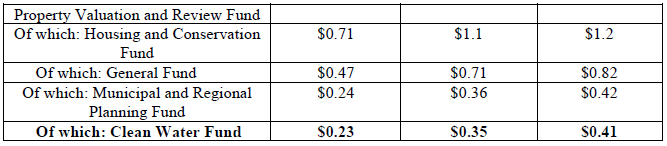

Sections 9 to 15: Controlling Interest Changes to the Property Transfer Tax

Under current law, the property transfer tax is due on the transfer of deed in a property. This section of the bill would extend that liability to transfers of controlling interest in a property.

The estimate for this section of the bill represents baseline revenues for typical year-to-year controlling interest transfers. However, this revenue could be very volatile due to large one-time controlling interest transfers in any given year. The additional revenue generated by these sections could be significantly higher in any single year due to these large one-time events.

The Joint Fiscal Office estimates that this section will generate an additional $1.6 million in baseline property transfer tax revenue in FY20 and growing in future years. The property transfer tax contains two components7:

- Property transfer tax revenues themselves which are allocated in the following fashion:

o The first 2% are these revenues are retained for the Department of Taxes for administration costs

o The remaining 98% are dedicated as follows:

§ 33% to the General Fund

§ 50% to the Housing and Conservation Trust Fund

§ 17% to the Municipal and Regional Planning Fund

- The Clean Water Surcharge (0.2%), the revenues of which are dedicated to the Clean Water Fund

This estimate is based upon data from other states that have similar controlling interest provisions within their property transfer taxes. Based upon these other state experiences, revenues from controlling interest transfers tend to increase year over year for the first two to three years as practitioners become more adept at applying the law to controlling interest transfers. This explains the ramp up in revenues in succeeding fiscal years.

Administrative costs for the section of the bill are expected to be minimal for the Department of Taxes. However, it is possible additional resources may be needed in the future should the Department discover future needs to ensure compliance.

Sources:

This estimate relied upon data from the Connecticut and Maine Departments of Revenue, the Department of Taxes 2018 Property Valuation and Review Annual Report8 and the January 2018 Consensus Revenue Forecast.

This estimate assumes that the vast majority of controlling interest sales will pay the 1.25% property transfer tax rate. Transfers that pay this tax are non-principal residences and principal residences on the marginal value above $100,000

Sections 16-17: Land Gains Tax

These sections of the bill redefine the definitions of land transfers subject to the tax. Should this bill become law, only land subdivided by the transferor within six years prior to the sale or exchange would be subject to the tax. This section also exempts land transferred in a downtown development district, a village center, or new town center development.

Together, these changes would greatly reduce the current tax base for the land gains tax. In 2017, of all returns that submitted a land gains tax, less than 15% had been subdivided and those properties paid land gains tax totaling around $400,000. The further exemption of land within a downtown or village center district would further narrow the subset of properties subject to the tax.

As such, JFO estimates that this section of the bill will reduce General Fund revenues by $1.55 million in FY20. As the current land gains tax generates between $1.6 and $1.75 million per year, these changes will reduce revenues from the tax by 88%. The number of returns that would be required to complete a land gains return is expected to drop significantly.

Sources: Department of Taxes

Section 18: Fuel Tax

This section clarifies that all Vermont entities purchasing heating or dyed diesel fuels, kerosene, propane, electricity, natural gas or coal shall pay the Fuel Tax without any exemptions. Current statute states that any residence or business shall pay the Fuel Tax, which in effect exempts nonprofit agencies, municipal, state, and Federal governments.

The inclusion of these agencies’ fuel purchases is expected to generate $390,000 in FY20. All these additional revenues will be dedicated to the Weatherization Fund.

Sources: Vermont Fuel Dealers Association, Seven Days Nonprofit Navigator9, Federal Reserve Bank of St. Louis, The Urban Institute10

Sections 19 to 21: Health Information Technology tax

There currently exists a 0.999% tax on the value of all private health insurance claims, of which 0.199% of this is deposited into the Health Information Technology (HIT) Fund. The current 0.999% is scheduled to decrease to 0.8% on July 1, 2019, eliminating the 0.199% that is deposited into the HIT fund. This section extends the current rate. This extension is revenue neutral for FY20.

Should the Legislature choose not to extend this sunset beyond July 1, 2021, the fiscal impact on the HIT Fund would be -$4.1 million in FY22.

Section 22: Home Health Provider Tax

There currently exists a tax on net patient revenues from core home health and hospice services equal to 4.25%. This tax was set to sunset July 1, 2019. This section would extend the sunset until July 1, 2021. This extension is revenue neutral for FY2020.

Should the Legislature choose not to extend this sunset beyond July 1, 2021, the fiscal impact on the General Fund would be -$10.4 million in FY22. -$4.8 million of this impact would be losses from current revenue from the tax and an additional -$5.6 million would be as a result of a loss of federal matching dollars.

1 These include most online travel websites, including Expedia, booking.com, Priceline but also include booking websites for short term rentals, including AirBnB, HomeAway, and VRBO.

2 H.532 (Budget Adjustment) also contains a change to the distribution of funds from the Department of Taxes Computer Modernization Fund to the General Fund from 80% to 40%. That change generates an additional $4.8 million for the General Fund. The House Budget bill furthers that change from 40% to 30% generating an additional $1.2 million.

3 These include most online travel websites, including Expedia, booking.com, Priceline, but also include booking websites for short term rentals, including AirBnB, HomeAway, and VRBO.

4 Fiscal Note: S.204 of the 2018 Session. https://ljfo.vermont.gov/assets/docs/fiscal_notes/76ee30e86b/2018_S_204_...

5 In 2016, AirBnB signed an agreement with the Department of Taxes to collect rooms tax on behalf of operators on its platform.

6 “2017 Benchmark Report: Tourism in Vermont.” Vermont Department of Tourism and Marketing. December 2018. https://accd.vermont.gov/sites/accdnew/files/documents/VDTM/BenchmarkStu...

7 In previous fiscal years, the Legislative budget and the Administration’s proposed budgets have allocated a certain amount of property transfer tax revenue to these funds. The remaining property transfer tax revenues are then distributed to the General Fund, notwithstanding the statute on the allocation of the various funds

9 https://nonprofits.sevendaysvt.com/

10 “The Nonprofit Sector in Brief 2015.” Brice McKeever. The Urban Institute. October 2015. https://www.urban.org/sites/default/files/publication/72536/2000497-The-...

8 “Annual Report: Based on 2018 Grand List Data.” Division of Property Valuation and Review. Vermont Department of Taxes. https://tax.vermont.gov/sites/tax/files/documents/PVR-Annual%20Report-20...