by Timothy McQuiston, Vermont Business Magazine Vermont budget writers should not get comfortable with the windfall tax revenue surplus the state enjoyed in the recently concluded fiscal year (June 30), because much of it was generated by one-time events. The General Fund surplus was nearly $60 million. And while you might want to walk on eggshells around it, two state economists told Governor Scott and key legislators that even with their concerns, the economy is still doing well and tax revenues the next couple of years should increase about another $20 million.

Economists Jeff Carr of Economic & Policy Resources of Williston (for the administration) and Tom Kavet of Kavet, Rockler & Associates, LLC of Williamstown (for lawmakers), joined the Emergency Board today to provide their tax revenue projections for the new fiscal year and assess the current condition of the Vermont and national economies.

Kavet and Carr laid out their vision of the economy in what Carr described as having “downside risk” to what is otherwise positive economic conditions.

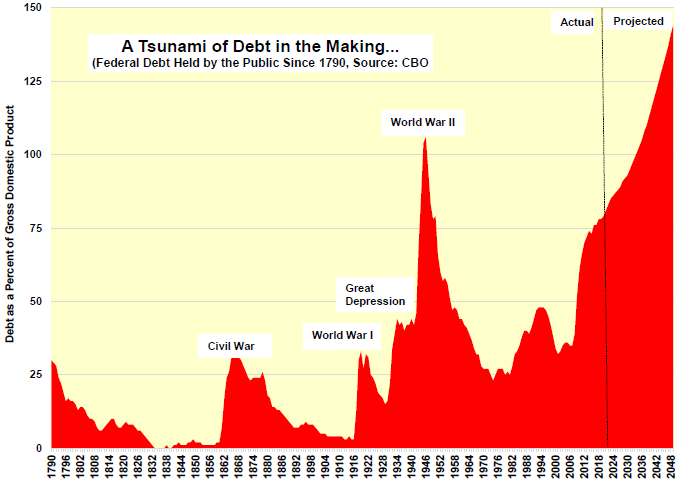

Kavet said the same, but emphasized that not only will the federal government run a trillion dollar deficit, in the foreseeable future the debt and interest on the debt will dwarf where we are now. In fact, interest will surpass the primary debt starting next year. Debt has also fueled much of the current economic expansion, but it is also the largest peacetime borrowing.

They also said that the Fed is likely to cut interest rates in two days. In 2018 they raised rates, which caused consternation in the economy and led to whispers of a possible recession. But the economy rebounded as the Fed first indicated earlier this year it would not raise rates. And now the Fed is leading everyone to believe they will once again cut rates to further stimulate the economy.

Highlights

- Historically low unemployment rates nationally and in Vermont.

- Increased revenues from high earners because of capital gains and adjusted gross income increases and repatriation of overseas corporate earnings resulted in more than a $50 million Vermont budget surplus.

- Personal income tax receipts topped $1 billion for the first time in April.

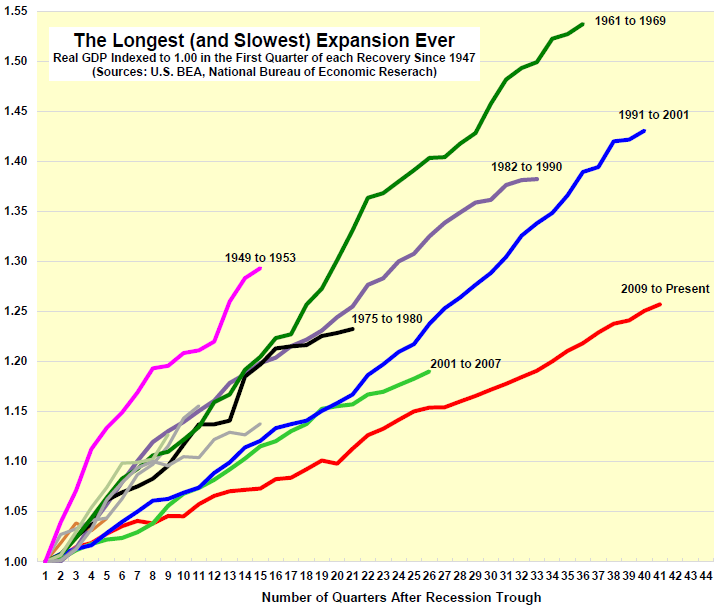

- Longest US expansion ever at a very slow climb

- Federal government is running a trillion dollar deficit, which is also stimulating the economy.

- The debt is at its highest peacetime level (78 percent of GDP) and the interest alone in the new fiscal year will surpass the amount of the actual principal.

- Tight labor market has finally resulted in real wage growth.

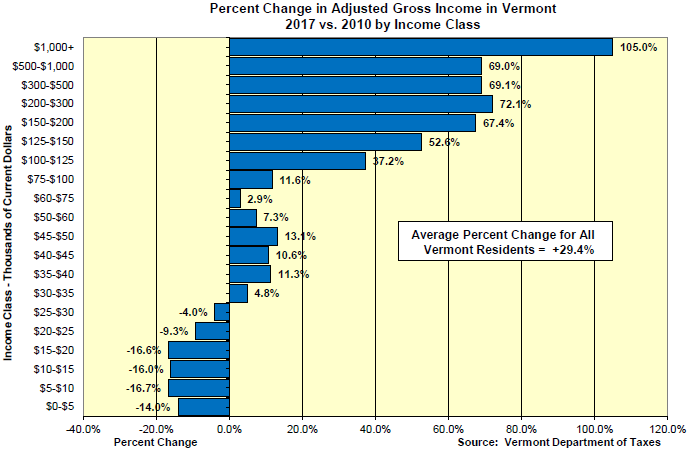

- The highest income earners have seen the highest gains; the lowest have lost income (under $30,000).

- Average home prices in Vermont have risen to highest levels ever (5.4 percent above peak) and recovered from the Great Recession (12.7 percent above low point), but this has been generated almost entirely by growth in the Burlington area.

- New home construction has slowed nationally and in Vermont are down 24 percent, as mortgage interest rates have increased and some tax breaks have been discontinued.

- Escalation of trade wars is biggest threat to economy.

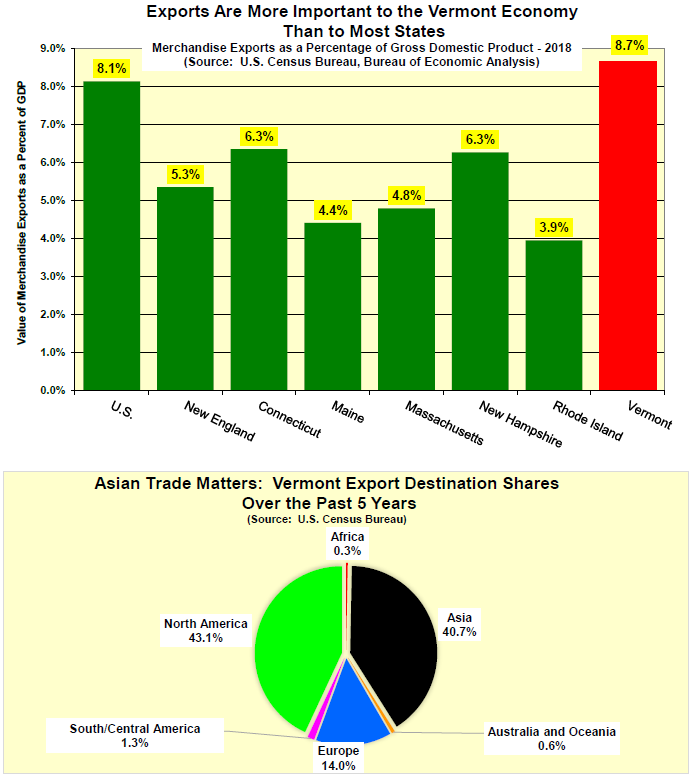

- Vermont still has the highest percentage of export trade in New England, despite recent declines, and is still higher than the US average. Vermont exports focused on trade-war sensitive areas in Asia and North America.

- No immediate threat of recession.

(Charts and commentary courtesy of Kavet, Rockler & Associates, LLC

With both federal fiscal and monetary policy now favorably aligned, and deficit hawks an endangered species, the U.S. economy celebrated its longest expansion in recorded economic history (since 1854) this month and will likely continue to expand through the next fiscal year. After seven interest rate hikes in 2017 and 2018 that had slowed credit-sensitive industries like housing and autos, the Fed reversed course in 2019, cancelling expected further hikes and signaling possible interest rate cuts in order to sustain the expansion – the first of which may occur in a few days.

Meanwhile, fiscal policy has been powerfully stimulative, with deficit-funded tax cuts inflating corporate profits and personal income while bipartisan budget deals look to add more than $2 trillion in debt through 2029. The combined effect of all this represents more than $4 trillion in additional deficit spending over this period. The current year federal deficit is expected to be nearly $1 trillion, pumping up near-term growth at the expense of longer-term borrowing capacity and soaring future debt payment liabilities.

With the economy humming, both corporate and personal income tax receipts in Vermont were extremely strong in FY19, lifting Source G-Fund revenues over $2 billion in both April and June (at seasonally adjusted annual rates) for the first time ever. Total FY19 revenues across all three major funds ended the year about 2.5% above prior January forecasts, with the G-Fund up about 4.5%, the T-Fund down about 1.2% and the E-Fund 0.4% below target. Much of this strength is expected to continue into FY20 and FY21, though at slower rates of growth. Allocative and other tax changes to the various funds enacted during the 2019 legislative session make comparisons to January projections difficult, but revenue impacts associated with macroeconomic changes will add about $20-$30 million per year (approximately 1%) across all three funds relative to prior estimates.

State Revenues

• Aggregate revenues across all three major funds forecast closed the fiscal year more than $50 million (2.5%) above prior January expectations. Revenues benefitted from a strong economy, continued concentrations of wealth and income among high-income taxpayers, and provisions in the Tax Cuts and Jobs Act that resulted in both effective personal income tax rate increases for some and one-time revenues from repatriation of corporate earnings placed in foreign tax jurisdictions that had avoided prior taxation. These two income tax sources alone closed the fiscal year about $60 million over target, offsetting net misses in smaller revenue categories, including a $6.5M shortfall in volatile Estate tax revenues.

• Major definitional changes were made to various funds and revenue sources in this forecast update that make comparisons with prior data and projections moot. Notable among these, selected healthcare-related taxes totaling about $270M, previously in other funds, were transferred to the Available General Fund in an effort to offset prior year out-transfers to other funds. These revenues are not new to the State, nor do they increase its financial capacity in any way. In other such changes, the allocation of Meals and Rooms revenues to the Available General Fund, after being reduced from 100% to 75% in FY19, was further reduced by $7.5M in FY20 and thereafter from 75% to 69%. Other budgetary maneuvers will leave Liquor revenues in the Available General Fund reported herein about $18M per year below prior estimates, even though these funds will still ultimately end up as “available” to the General Fund via transfers from the “Enterprise Fund” to the General Fund.

• Corporate tax revenues closed the fiscal year $11.7M over target, due primarily to one-time payments associated with repatriation liabilities. Unfortunately, after 18 months and a great deal of Tax Department effort following passage of the Tax Cuts and Jobs Act (TCJA), we have very little additional hard information on exactly which corporate payments may be associated with repatriation liabilities - and what liabilities may remain. Initial FY estimates put potential corporate repatriation revenues between $17M and $46M, with expectations for continued FY20 payments of about half this amount. FY21 could still benefit from lingering repatriation payments, but these are expected to largely disappear by FY22, resulting in a three-year decline between FY19 and FY22 of more than $40M. As noted in detail in the past two forecast updates, there is still considerable uncertainty regarding the payment, legal liability, timing and rule-making associated with repatriation payments at both the federal and state levels.

• Personal income tax receipts were exceptionally strong in April, topping $1 billion at seasonally adjusted annual rates for the first time ever. This revenue source is notoriously volatile and becoming more so over time. Sharp variations can occur with April tax filings. FY19 represented one of the largest such deviations, resulting in about $37M in additional revenue in April, and closing the fiscal year about $50M (6%) above expectations. Although we will not know the full story behind FY19 PI revenues until the filing year is closed in October, early information indicates a continuation of significant capital gains and AGI growth among the highest income classes. More Adjusted Gross Income (AGI) among high income groups results in greater State revenue, since the effective tax rates for these groups are also higher. While this is positive for State revenues, it also exacerbates revenue volatility and uncertainty. This component of personal income tax revenue is capable of dropping precipitously during a downturn and spiking in random years during expansions.

• Some of the FY19 strength in personal income taxes is due to effective State tax increases from the TCJA that affected a limited subset of filers. Although these effects may diminish over time, there are still aspects of the legislation we are analyzing with respect to the FY19 returns, such as the treatment of loss limitations (referred to as “excess business losses”) that could end up being be substantial. In addition to trailing TCJA impacts, legislative changes in the 2019 session will net out to about $0.2M in FY20 and $2M in FY21 to this revenue category. Because of the concentration of a small number of “one-time” high-income tax events in FY19, net growth in FY20 may be subdued, before advancing in FY21 at about 2% and higher thereafter.

• Brick and mortar Sales and Use tax revenues were sluggish in FY19, as higher interest rates affected purchases of consumer durables and rising trade war fears dampened consumer sentiment. Inflation-adjusted retail sales have recently recovered, but have been stuck below 2% for most of the last year. Despite generating significant additional revenue in FY19 from both existing and new e-commerce vendors as a result of the Supreme Court decision in the Wayfair case (Internet sales), Sales and Use receipts ended the year slightly below (-0.6%) projections. In FY20, S&U tax revenues are expected to accelerate, as marketplace facilitators join the growing ranks of new e-commerce filers – ultimately contributing between about 8% to 10% of total sales and use tax revenue over the forecast horizon.

Meals & Rooms tax receipts continued to be solid in FY19, with a healthy winter skiing season supporting visitation and spending. Total year-end revenues were about 0.3% above targets, in part due to strong rental receipts from Airbnb. With the same fundamentals in FY20 (favorable demographics, a robust economy, accommodating winter weather and high regional income), and new revenue from other e-commerce market participants, Source Meals & Rooms revenue growth could approach 6%. Statutory changes in the last legislative session, however, will shave $7.5M from this for the Clean Water Fund and send portions of the remainder to the Available General and Education Funds. This allocation will change to a fixed transfer of 69% to the G-Fund, 25% to the E-Fund and 6% to the CW-Fund in FY21.

Cigarette and Tobacco Products revenue closed FY19 almost exactly as forecast in the earlier July 2018 Revenue Update (-0.1%), however, an unprecedented inventory build-up in December prompted a January upgrade to the forecast that ended up being 4% above final year-end revenues. Other Tobacco Products also registered their first annual decline ever in FY19. In FY20 and beyond, Cigarette tax revenues have been moved to a new Healthcare Revenue sub-category within the Available General Fund, and will be supplemented by a new tax on vaping products - and diminished by a new 21 year old (from 18) age restriction for legal purchase. These two changes will result in slightly higher net revenues, but will be imperceptible amidst the declining longer term trajectory of cigarette sales caused by persistent antismoking measures.

• The Estate tax ended the fiscal year $6.4 million below target – the largest percentage miss of any tax category (-34%) – but well within its “normal” year to year variation. Because of the exceedingly small number of affected taxpayers in any given year, this revenue category is among the most volatile of all revenue sources. The sum of any consecutive 4 quarters over the past 10 years has ranged from $10M to $40M, with very little correlation with short-term external economic events. This will continue in FY20, however, statutory changes effective January 1, 2020 that raise the Estate tax exclusion from $3.25M to $4.25M will reduce revenues by about $4.5M in FY21. A further increase in the exclusion to $5 million, effective January 1, 2021, is expected to reduce FY22 revenues by about $7.5M. As equity markets, real estate prices and business valuations increase, the potential for large estate remittances will continue, however, in any given year, actual revenues could vary significantly from projections.

• Property Transfer Tax revenues in FY19 were affected by rising mortgage rates throughout 2018, slowing both property price appreciation and the volume of transactions, and leading to a $1M year-end shortfall. Lower mortgage rates heading into FY20 and legislation in the last session that extends taxation to controlling interest ownership transfers should result in growth of more than 10% in FY20 and about 8% in FY21.

• The Telephone Property tax continues to decline as projected and ended FY19 at less than half its FY14 level, due to aggressive depreciation being taken by some of the largest payers and statutory ambiguity regarding such depreciation and the applicability of the tax to wireless and VoIP providers. Without statutory clarification, this revenue source will likely continue to decline, generating at least $5 to $6 million less than FY14 levels for the foreseeable future.

• Other General Fund Tax revenue, which primarily consists of the Land Gains tax, was almost exactly on target in FY19 at $2.4M. Statutory changes to this tax in the last legislative session, however, will reduce FY20 revenues by about 30% and FY21 revenues by more than 60% (about $1.6M).

• Transportation Fund revenues were very close to targets through the first 11 months of FY19, but fell short in June by $2.6M, ending the year 1.2% below target. The June miss was spread across virtually every T-Fund revenue source, suggesting a possible administrative or processing cause. The largest percentage miss was in the Diesel tax, -2.8%, but this tax is affected by various transfers and inventory fluctuations that make it irregular on a monthly basis. Motor Vehicle Purchase and Use revenues were also down 2.0% in FY19, but this category had been affected by rising interest rates through much of 2018 and the slowdown in consumer spending in early 2019. Motor Vehicle Fees were off by 1.0%, but new registrations (about half of the revenue in this category) in FY19 were strong and all of the shortfall was due to higher than expected out-transfers of other fees. Gasoline revenue was very close to expectations with a 0.5% miss, but relatively low gas prices and continued sluggish volume demand during the forecast period will keep revenues from both gasoline-derived taxes relatively flat. Electric vehicle market penetration, although growing (see below map) and relatively high on a per capita basis in Vermont, is still a very small percentage of vehicles on the road and not yet a major factor in FY20 and FY21 gasoline revenue projections.

General Discussion

Since the recession’s low point more than 9 years ago, the U.S. has added 23.6 million jobs (16.6%), including a span of 105 consecutive months – and counting. Although job growth in Vermont since its recessionary trough has only been about half the U.S. rate (totaling 8.1% through June), the State has added 23,900 nonagricultural payroll jobs. This growth has pushed the Vermont unemployment rate to an all-time record low and the U.S, rate to its lowest level in nearly five decades. As illustrated in the chart on the following page, Vermont’s 2.1% unemployment rate in both May and June was the lowest in the nation.

As a coincident economic indicator, the unemployment rate is a key measure of economic health. Because it is a relatively stable metric, any sustained increase in the unemployment rate can also flag the start of a downturn. If the rate increases by more than a quarter percentage point in a three-month period, a recession is likely. All 10 of the recessions since World War II have begun with such an increase in the U.S. unemployment rate.

Sub-state unemployment rates have also dropped and narrowed throughout the U.S. and Vermont, the highest county unemployment rate is now in Orleans County, at just 4%, with the lowest, as almost always, in Chittenden County, at 1.9%. Even Essex County, which experienced unemployment rates of nearly 10% during the worst of the last recession, registered an unemployment rate during the 12 months between June of 2018 and May of 2019 of only 3.2%. 11 of Vermont’s 14 counties now have average annualized unemployment rates below 3%.

The tightness in U.S. labor markets is finally manifesting in real wage growth. After nearly two years of flat or negative real wage changes, nominal wage growth accelerated to more than 3% during most of the last year and inflation-adjusted growth has been between 1% and 2% since November of 2018.

Real estate markets continue to improve throughout the nation – though with stark regional differences. Home prices have now exceeded their pre-recession peaks in all but 10 states – roughly characterized by a group that experienced huge speculative excesses (AZ, NV and FL) and associated pre-recession price spikes and those with fundamental or sectoral economic weakness (CT, RI, IL, MD, NJ, DE, NM). Despite these pockets of weaker relative performance, virtually every state has experienced home price growth in each of the last 20 quarters.

Vermont home prices are now about 5.4% above their prior peak and 12.7% above their lowest levels during the last recession. However, within the State, as is true with many State economic metrics, the Burlington metropolitan area has dramatically outperformed the rest of the State. Home prices in the Burlington MSA through the first quarter of 2019 (the latest data available) exceeded their prior cyclical peak by 13.9%, while prices in the balance of the State were still 1.2% below their prior peak level, reached in the first quarter of 2008.

Although home prices in the first quarter of 2019 rose in every state relative to year-ago levels, there has been a noticeable price deceleration in most states, due to steadily increasing home mortgage rates through 2018 and tax deductibility changes in the TCJA that effectively raised the cost of property ownership in many states. This also acted to slow new residential construction, with Vermont housing starts down 24% in the first half of 2019.

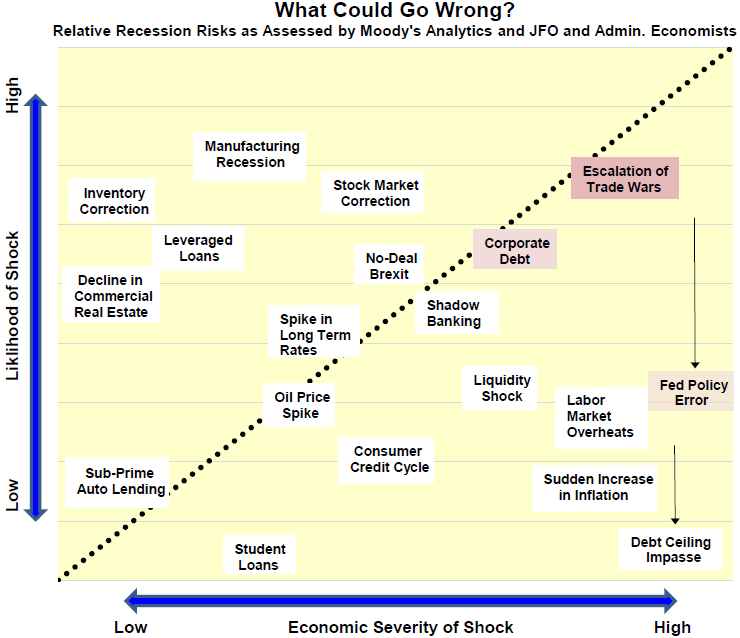

At this stage of the business cycle, forecast risks abound. The chart above outlines a number of events (many of which are interrelated) that could dent or terminate the current expansion. Prominent in this risk matrix, is the rising likelihood of trade war escalation, particularly with China. To date, trade rhetoric with Mexico, Canada, the E.U. and Japan has been more bark than bite, with a revised NAFTA agreement that is not meaningfully different than its predecessor. The tariffs imposed on China have been much more impactful, but have mostly been limited to intermediate goods that have not yet fully hit U.S. consumers, who will ultimately pay most of this cost. If further escalation occurs, it may destabilize portions of the global economy that could lead to recession and ultimately weaken U.S. global economic strength and influence. The use of punitive tariffs as an instrument of foreign policy for non-economic purposes (such as with Turkey and Mexico) also threatens to undermine the U.S. economy and harm long-term relationships with both allies and adversaries.

Ironically, one of the reasons this economic cycle may still have room to grow despite being the longest ever, is its tepid growth trajectory. This expansion is both the longest and slowest on record. This slow, steady pace, and the institutional memory of the deep recent recession, have contributed to the avoidance of major economic imbalances, despite the recovery’s longevity. Although near-term recession risks have risen, according to the Wall Street Journal’s Economic Forecasting Survey, from about 20% to 30%, there are not obvious imbalances that suggest an imminent decline.

If there is an expanded trade war, the Vermont economy is not likely to be spared. Despite declining trade as a share of State GDP, Vermont still has the highest reliance on exports in the New England region and is above the national average. Vermont also has a relatively high trade dependence on Asia and North America, regions in which trade hostility could be especially severe.

Though not an imminent recession risk, the ballooning federal debt as a share of Gross Domestic Product – especially during a time of economic vigor, when debt levels normally recede – represents a serious longer-term economic risk and one that could, as the Congressional Budget Office recently warned, provoke a sudden fiscal and economic crisis. Recent projections from the CBO show current law U.S. debt as a percentage of GDP rising from about 78% in Federal FY19 – the highest peacetime level ever - to 144% in 2049.

While deficit spending can stimulate the economy and is an important countercyclical policy tool, it is rarely beneficial in an economy operating close to or at its full potential. The political restraint controlling such borrowing seems to have evaporated amidst the abbreviated political time horizon within which such issues are evaluated and the ease with which the U.S. can currently borrow due to the widespread use of the U.S. dollar as a global currency. Like the pension funding issues now plaguing our State budgetary processes, however, someone in the future will pay for these policy mistakes. Without a change of course, CBO projects annual interest costs alone will exceed the primary debt starting in FY20.