Maple Capital Management First it was Brexit and now it’s the election of Donald Trump to the Presidency of the United States. In both cases, voters acted with disdain for the status quo and markets reacted with glee. Investors positioned themselves ahead of both votes for what was sure to be the certain result, only to be proved wrong when the votes were counted. The initial reaction to the Trump victory was a sharp sell-off in most markets. Asian stock markets were down 3 to 5%, European markets down 1 to 2%, and US stock futures 1.5 to 2%. US Treasuries rallied on the news, with yields falling to the low 1.70’s, before sharply reversing to the mid 1.90’s level. Since, investors have embraced the pro-growth policies Trump has outlined, causing equity markets to surge and interest rates to climb.

How this will affect markets in the weeks ahead is still a big unknown. Mr Trump’s looming Presidency will definitely disrupt the status quo. With his final policy goals still unknown and a habit of making rash or insensitive comments, a Trump presidency is very hard to predict. He seems poised to reverse a trend of internationalism practiced by previous administrations, allowing America to focus on its own internal affairs. His positions on trade, immigration, and the deficit are particularly sensitive for global financial markets and will be closely watched. We expect volatility will be elevated for a while.

How this will affect markets in the weeks ahead is still a big unknown. Mr Trump’s looming Presidency will definitely disrupt the status quo. With his final policy goals still unknown and a habit of making rash or insensitive comments, a Trump presidency is very hard to predict. He seems poised to reverse a trend of internationalism practiced by previous administrations, allowing America to focus on its own internal affairs. His positions on trade, immigration, and the deficit are particularly sensitive for global financial markets and will be closely watched. We expect volatility will be elevated for a while.

The President-Elect could prove to be a great unifier in the bitterly divided halls of Congress. His positions often straddle party lines and may help unify the legislature. Several campaign pledges, including the promise to launch massive infrastructure spending projects, are likely to be supported by majorities of both parties in Congress. Even if his spending priorities are opposed, it is hard to act in open defiance against a new President so early in his first term.

The markets have already factored this anticipated growth into securities prices. Stocks have rallied sharply because people expect these policies to stimulate future growth. Bond prices have fallen in anticipation of higher inflation rates and a greater demand for capital in an expanding economy. We believe it is still too early for anyone to accurately model future inflation and growth. However, the direction on both should be up from pre-election levels.

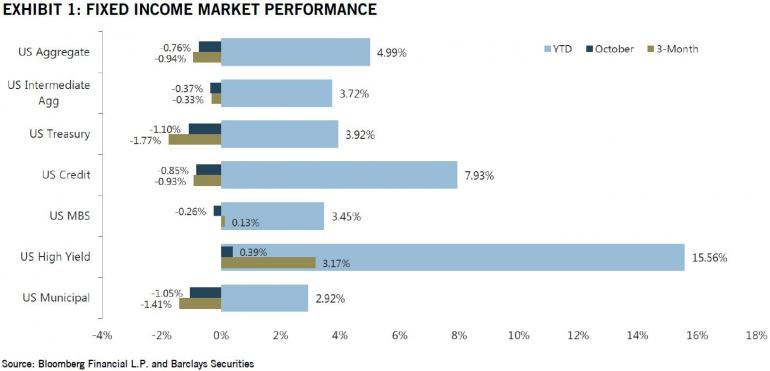

With delay for the election and the current state of flux markets have been thrown into with the outcome, it seems trivial to discuss October’s bond market performance. However, the data is eye-opening and highlights some of the risks that have built up over the past year. Bonds, in general, put in their third consecutive month of negative returns. The Bloomberg/Barclay’s index data provided in Exhibit 1 highlights the performance of the fixed income sectors.

High yield bonds continued to outperform, with the group being the best performer within the fixed-income asset class this year. We expect this trend to at least partially reverse in the months ahead. U.S. Treasuries put in a third straight monthly decline, and more should follow as rates begin to normalize. Municipal bonds have also had a tough time, as supply has swelled in the market. US credit has lost ground to the MBS sector over the last 3 months, but still has outperformed on a year-to-date basis.

Despite the positives for economic growth, there is reason for caution as the Trump Presidency unfolds. We are increasingly defensive on the bond market, especially with the Federal Reserve chomping at the bit to raise rates. The prospect of tightening monetary policy combined with fiscal policy uncertainties would be very disruptive for long duration portfolios. Corporate bonds – both investment grade and high yield – should do well with stronger economic growth. However, spreads are still tight and corporations have taken on a lot of debt in the past three years. There is little room for error at current prices.

Source: Maple Capital Management, Inc. MCM is an independent SEC Registered Investment Advisor with offices in Montpelier, Vermont and Atlanta, Georgia. This commentary reflects the views of MCM and should not be considered to be investment or financial advice. MCM does not warranty these views and will not update this communication after the date of publication. Any mention of specific securities is done for illustrative purposes and the securities mentioned may or may not be held in client accounts. No assumption or assurance should be taken that securities mentioned will be safe or profitable investments.

Source: Maple Capital Management, Inc. MCM is an independent SEC Registered Investment Advisor with offices in Montpelier, Vermont and Atlanta, Georgia. This commentary reflects the views of MCM and should not be considered to be investment or financial advice. MCM does not warranty these views and will not update this communication after the date of publication. Any mention of specific securities is done for illustrative purposes and the securities mentioned may or may not be held in client accounts. No assumption or assurance should be taken that securities mentioned will be safe or profitable investments.

For further information, please contact Steven Killoran, Vice President Business Development at 1-802-229-2838 or at [email protected]. For further information about Maple Capital, including a copy of our informational brochure, see www.maplecapital.com.