by Timothy McQuiston Vermont Business Magazine Casella Waste Systems, Inc is attempting to fend off one of its investors in a shareholders proxy fight that could result in Chairman and CEO John Casella being removed from the board of directors. JCP Investment Management, LLC, a small investment firm based in Houston, TX, holds just over a 5 percent stake in the Vermont-based firm. It claims it wants to replace the three board members up for re-election with three independent members of its choosing "because we are dedicated to maximizing shareholder value and improving corporate governance at Casella and we are confident that enhancing the Board is a critical first step towards these goals."

Casella released its statement Monday morning and by Tuesday afternoon shares were down slightly to about $5.80 (52-week range: $3.41 - $6.75) and down about 20 cents since their close Friday. JCP announced its intent to challenge the board nominees last April.

(SEE full statements from both companies below.)

Casella (Nasdaq:CWST), a regional solid waste, recycling, and resource management services company based in Rutland today announced that, in connection with its 2015 Annual Meeting of Stockholders to be held on November 6, 2015, its Board of Directors has issued a letter to its stockholders and a retort to JCP.

The letter, which includes a WHITE proxy card, outlines the significant and decisive actions that Casella’s Board and management have taken to enhance Casella’s long-term prospects and best position Casella to create value for its stockholders, and recommends that stockholders vote on the WHITE proxy card FOR the election of all three of Casella's highly qualified and very experienced nominees, John W Casella, William P Hulligan and James E O’Connor. Casella urges stockholders to promptly vote the WHITE proxy card via Internet, telephone or mail by following the instructions provided. The Board also urges stockholders to discard any gold proxy card or voting instruction form they may receive from the JCP Group.

As previously disclosed, JCP Investment Management, LLC (James C Pappas majority owner) and the other participants in its solicitation (the “JCP Group”) have indicated that they intend to conduct a proxy contest and seek the election at the 2015 Annual Meeting of director candidates in opposition to "the highly qualified and very experienced nominees unanimously recommended by the Casella Board."

JCP, in its statement, blistered the existing Board and managment by saying, in part, "In our view, Casella is deeply undervalued as a result of poor investment and operational decisions and a dual capital structure that has eroded shareholder rights and value." It is putting up three candidates, as is Casella.

In order for stockholders to have access to all relevant information concerning the 2015 Annual Meeting that Casella has made available, the Company has developed a website focused on the 2015 Annual Meeting, which is accessible at www.casellashareholders.com.

The full text of the Casella and JCP statements are below:

|

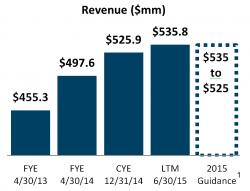

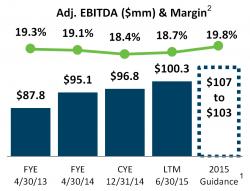

September 28, 2015 Dear Fellow Casella Stockholder: 2015 has been an exciting year for Casella Waste Systems, Inc. We believe the transformative process we began two and a half years ago to reconstitute and strengthen our management team, simplify and streamline our business, reduce our exposure to risk, increase our cash flows, improve our financial performance and position Casella for long-term growth and profitability is beginning to be reflected in our financial results and our stock price. We also believe that Casella is at a pivotal moment in its history and we are pursuing the right strategy for growing stockholder value. While your Board has been taking decisive action to enhance the value of your investment in Casella, JCP Investment Management, LLC, a dissident investor led by James C. Pappas that began accumulating its shares in Casella in May 2014, is seeking to disrupt our strategic trajectory. JCP is waging a proxy contest to elect its own candidates, including Mr. Pappas, to your Board at our upcoming 2015 Annual Meeting to be held on Friday, November 6, 2015. Over the past two and a half years, Casella has achieved significant progress and momentum in executing on its strategy, improving its financial and operating performance and growing stockholder value. As such, we question the judgment and logic of JCP in forcing upon Casella a costly and distracting proxy contest to replace highly qualified, experienced and valued members of your Board with its own candidates without providing stockholders with any credible arguments as to why its candidates, one of whom has no waste management industry experience whatsoever and one of whom has never served on a public company’s board of directors, are more qualified than your Board’s nominees to drive further stockholder value creation. We do not believe that JCP has proposed any director candidates who have experiences and competencies that would expand the depth and breadth of your Board. Nor has JCP shared with Casella’s management or your Board an alternative strategic plan or any specific ideas for improving Casella’s prospects or enhancing stockholder value. You now have an extremely important decision to make about the future of Casella and who should oversee Casella’s ongoing efforts to further improve its financial and operating performance and grow stockholder value. Once you review the facts, we hope you will agree to vote on the WHITE proxy card FOR ALL your Board’s nominees – John W. Casella, William P. Hulligan and James E. O’Connor – standing for election to your Board at this year’s Annual Meeting. Your Board urges you to sign and return the enclosed WHITE proxy card TODAY and vote FOR ALL your Board’s nominees. We urge you not to sign or return any gold proxy card you receive from JCP. YOUR BOARD HAS TAKEN DECISIVE ACTION TO DRIVE CASELLA’S STRATEGIC EXECUTION, DRIVE IMPROVED OPERATING AND FINANCIAL RESULTS, ENHANCE CASELLA’S LONG-TERM PROSPECTS AND POSITION CASELLA TO CREATE VALUE FOR ITS STOCKHOLDERS Over the past two and a half years, we have refocused our efforts and simplified our business structure. In December 2012, we recognized the need for a change in direction and thinking, and as such, we took the decisive steps to recast the senior management team by promoting Ed Johnson to the role of President & Chief Operating Officer as well as promoting Ned Coletta to the role of Chief Financial Officer. Under the leadership of John W. Casella, our Chairman and CEO, the team worked together to reset the strategic direction of the organization. In early 2013, we launched a comprehensive multi-year plan that we believed would improve our financial and operating performance, while reducing risk. We believe we have executed extremely well against this plan over the past two and a half years, as demonstrated in our improved financial performance. [Please see multimedia assets 1 and 2.]

Most recently, in July 2015, we reported second quarter results that we believe showed significant improvements in our financial performance. Revenues and Adjusted EBITDA were up 4.7% and 8.4% from the same period in 2014.2 With our improved operating performance and disciplined capital allocation, we generated strong cash flows in the second quarter and paid down $18.7 million of long-term debt from March 31, 2015 to June 30, 2015. NEXT STEPS: CONTINUE TO IMPROVE FREE CASH FLOW, FURTHER REDUCING LEVERAGE Early this summer, we refreshed our strategic plan since we had substantially completed the objectives we committed to in early 2013. Our newly launched plan focuses on further improving Free Cash Flow and reducing debt leverage through a focus in the following areas:

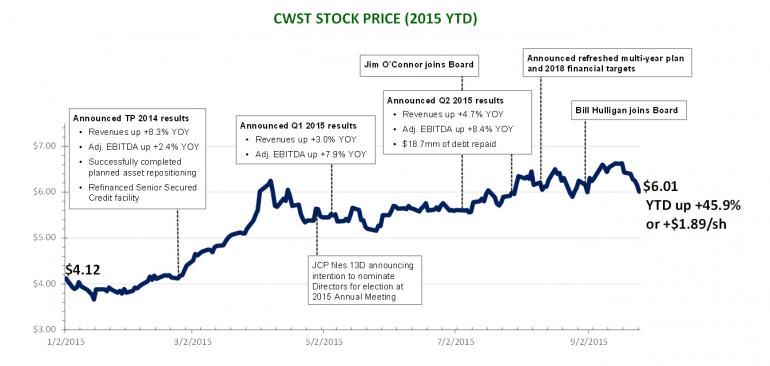

OUR DECISIVE ACTIONS TO TRANSFORM CASELLA AND THE SUCCESS OF OUR STRATEGY ARE NOT GOING UNNOTICED Our decisive actions to transform and reposition Casella, and our improved financial and operating performance, which we believe is attributable to our strategy, are not going unnoticed. In September 2015, Casella was named an Equity and Industry Research Best Ideas: Selecting Stocks to Outperform in a Volatile Environment, by Imperial Capital at its Global Opportunities Conference. Casella was 1 of 17 companies selected as a “Best Idea” by Imperial Capital. As the stock chart below indicates, we have generated a significant increase in stockholder value since the beginning of the year which we believe is attributable to the success we have had in executing our strategy, strengthening our management team, reducing our risk, exiting non-core businesses and improving our financial and operating performance. [Please see exhibit 3.] CASELLA’S NOMINEES ARE HIGHLY QUALIFIED AND JOIN A REFRESHED BOARD OVERSEEING OUR EFFORTS TO DRIVE STOCKHOLDER VALUE We believe that there are very real and stark differences between our nominees, John W. Casella, William P. Hulligan and James E. O’Connor, and the candidates proposed by JCP. We believe our director nominees are highly qualified and each have the integrity, knowledge, breadth of relevant and diverse experience and commitment necessary to navigate Casella through the complex, dynamic and challenging business environment in which we operate and to oversee our ongoing efforts to drive stockholder value. JOHN W. CASELLA - Director since 1993

JAMES E. O'CONNOR - Director since 2015

WILLIAM P. HULLIGAN - Director since 2015

Your Board believes that our newest independent directors and nominees, Messrs. Hulligan and O’Connor (both of whom have joined your Board within the past six months), are two of the most experienced, accomplished and admired individuals in the waste management industry and believe that both bring to your Board a proven record of success in leading and growing waste management businesses and creating stockholder value. We believe that their extensive senior management and governance experience at leading waste management companies and track record of driving growth and stockholder value creation will be extremely valuable to Casella as we continue to execute on our ongoing strategic initiatives to drive revenues and enhance profitability. If Messrs. Casella, Hulligan and O’Connor are re-elected at the 2015 Annual Meeting, your Board would be composed of nine directors, all of whom we believe to be highly qualified directors dedicated to serving the best interests of all stockholders. Of these nine directors, seven would be independent and four would have joined your Board since 2008, bringing fresh perspectives and relevant business experience to your Board. Further, your Board would collectively possess a broad and diverse set of skills, experiences and insights in the areas of solid waste collection, recycling, disposal services, operations, accounting, finance, investment banking, mergers and acquisitions, capital markets, capital allocation, capital structure, risk management, and strategic planning. The appointments of Messrs. Hulligan and O’Connor as new independent directors reflect your Board’s continuing commitment to recruit new independent and highly qualified directors who have perspectives, experiences and competencies that expand the Board’s scope and depth. Here is what third party analysts had to say about the appointments: "The appointment of Bill Hulligan, former president and COO of Progressive Waste Solutions, follows on the heels of former Republic Services CEO Jim O'Connor's addition to the board. We view both as strong industry executives who are well suited to make substantial contributions to Casella…. We take Hulligan's indication he had previously purchased 100,000 shares of Casella's stock as an additional sign of his confidence in the company's prospects." "We believe the board appointments provide evidence of its commitment to improving corporate governance and strengthening management oversight." JCP’S NOMINEES WOULD NOT BRING TO THE CASELLA BOARD ANY RELEVANT EXPERIENCE, SKILLS OR COMPETENCIES NOT ALREADY PRESENT AMONG CURRENT CASELLA BOARD MEMBERS We question JCP’s choice of nominees to replace two of your Board’s most highly qualified, experienced and valued directors – John W. Casella and William P. Hulligan. We do not believe that any of JCP’s nominees can be said to have experience comparable to that of either of the two members of your Board that JCP is seeking to replace. Further, we do not believe that any of JCP’s nominees would bring to the Casella Board any relevant insights, perspectives, skills or competencies not already present among the current members of the Casella Board. Consider the following with respect to JCP’s two proposed director candidates:

OUR BOARD HAS TAKEN CONCRETE ACTION TO ENHANCE ITS CORPORATE GOVERNANCE PRACTICES TO BE MORE CONSISTENT WITH BEST PRACTICES As part of your Board’s efforts to enhance its functionality and its ability to serve the long-term interests of stockholders, and in response to stockholder input, your Board has adopted the following corporate governance enhancements which it believes are consistent with best practices:

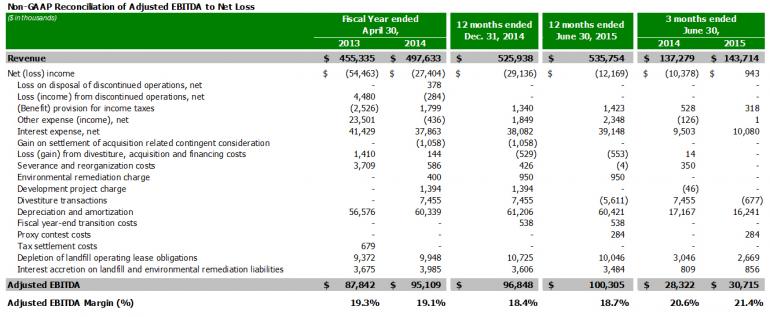

WE HAVE ATTEMPTED ON NUMEROUS OCCASIONS TO CONSTRUCTIVELY AND IN GOOD FAITH ENGAGE WITH JCP TO AVOID A PROXY CONTEST Casella maintains an open dialogue with all its stockholders, and is always open to constructive input. As such, over the past 6 months, we have attempted on numerous occasions to constructively and in good faith engage with JCP to hear its views on Casella. However, over the course of numerous telephone discussions and even an in-person meeting with our executive management at Casella’s headquarters in Rutland, Vermont, JCP has not shared with Casella’s management or your Board any suggestions for operational improvements, an alternative strategic plan or any specific ideas for improving Casella’s long-term prospects. Despite our open dialogue with JCP and the good faith manner in which we approached our discussions, the first time we heard any interest from JCP in proposing director candidates was in April 2015, when we received their notice indicating their intent to nominate three director candidates. In an attempt to avoid a costly and distracting proxy contest, we made clear our willingness to meet in-person with JCP’s nominees to assess whether JCP had proposed any director candidates who have experiences and competencies that could expand the depth and breadth of your Board. JCP’s initial response was to refuse to allow us to meet or speak with their director candidates or have their candidates complete Casella’s standard director questionnaire, insisting that we first reach agreement on a “settlement framework.” Eventually, JCP agreed to allow us to conduct phone interviews with its proposed director candidates but remained steadfast in refusing to allow us to interview any of its director candidates in person or have its candidates complete Casella’s standard director questionnaire. Your Board is very amenable to adding to its membership additional independent directors who would add to the depth and breadth of its insights, perspectives, competencies and skills and is receptive to considering and interviewing candidates referred to us by a stockholder but such candidates must be committed to acting in the best interests of ALL stockholders and must not be, in any way, obligated or expected to serve or advocate for the interests of any particular constituency. We question how serious JCP was about having its proposed candidates serve as directors who would represent the best interests of ALL stockholders when it would not even allow them to meet with us in person or complete our standard director questionnaire. JCP LACKS ANY SPECIFIC PLANS ON HOW TO ENHANCE STOCKHOLDER VALUE AT CASELLA To date, JCP has failed to put forward any ideas to further enhance Casella’s strong performance or enhance Casella’s long-term prospects. In fact, in its most recent amended proxy filing with the SEC, JCP openly stated the following in regards to their slate of proposed nominees: “The [JCP] Nominees do not have specific plans for the Company…” In addition, Mr. Pappas’ lack of any waste management industry experience whatsoever, the fact that Mr. Pappas’ public company board experience is mostly limited to food-related companies, and Mr. Frazier’s lack of experience ever serving on a public company’s board of directors calls in to question how they would better serve the interests of stockholders if they were elected to your Board to replace two of our most experienced and valued directors, both of whom have extensive experience in the waste management industry and both of whom have experience serving on one or more public company boards. The point is quite simple – despite their claimed “displeasure with our performance,” JCP fails to acknowledge the progress we have achieved in the past two and a half years and the momentum we believe we have going forward, and has yet to put forward any sort of credible plan of its own. Unlike JCP and its nominees, we have a plan – a plan that we believe is working and that we believe will continue to drive positive results and strong momentum. SUPPORT YOUR BOARD’S HIGHLY QUALIFIED NOMINEES BY VOTING THE WHITE PROXY CARD TODAY The upcoming Annual Meeting is a significant event that could determine the future of Casella. Your vote is important – no matter how many shares you own – as no stockholder is too small. Whether or not you plan to attend the Annual Meeting, we urge you to sign, date and return the enclosed WHITE proxy card in the postage-paid envelope provided and vote FOR ALL your Board’s highly qualified and very experienced nominees – John W. Casella, William P. Hulligan and James E. O’Connor. You may also vote by telephone or Internet by following the instructions on the enclosed WHITE proxy card. We also urge you to discard any proxy card or voting instruction form you may receive from JCP. Even a WITHHOLD vote with respect to JCP’s nominees on its proxy card will cancel any proxy previously given to Casella. If you previously signed a proxy card sent to you by JCP, you can revoke that proxy card and vote for your Board’s recommended nominees by voting a new WHITE proxy card. Only your latest-dated proxy card will count. Your Board encourages you to vote each WHITE proxy card you receive. On behalf of your Board of Directors, we thank you for your continued support of the Company. We look forward to communicating further with you in the coming weeks. Sincerely, John W. Casella Gregory B. Peters If you have any questions, require additional copies of Casella’s proxy materials or need assistance in voting your WHITE proxy card, please contact our proxy solicitor at the phone numbers or email listed below: MacKenzie Partners, Inc. 105 Madison Avenue Forward-Looking Statements Certain matters discussed in this letter are “forward-looking statements” intended to qualify for the safe harbors from liability established by the Private Securities Litigation Reform Act of 1995. These forward-looking statements can generally be identified as such by the context of the statements, including words such as “believe,” “expect,” “anticipate,” “plan,” “may,” “would,” “intend,” “estimate,” “guidance” and other similar expressions, whether in the negative or affirmative. Similarly, statements that describe the objectives, plans or goals of Casella are forward-looking. Such forward-looking statements include, but are not limited to, statements regarding the anticipated proxy contest by JCP Investment Management, LLC and the other participants in its solicitation, Casella’s initiatives to improve the Company’s performance and increase its growth and profitability, Casella’s future operational and financial performance, Casella’s actions taken or contemplated to enhance its long-term prospects and enhance value for its stockholders, Casella’s efforts to execute on and implement its strategic plan, Casella’s plans to simplify its business structure, Casella’s actions taken or contemplated with respect to corporate and board governance, Casella’s plans to improve its cash flows and reduce its risk exposure by divesting or closing operations that do not fit within its core strategy, Casella’s plans to strengthen its balance sheet, promote financial flexibility and position the Company to achieve its target growth trajectory and Casella’s plans to achieve its three (3) year financial objectives and to drive additional value creation for the benefit of all its stockholders. These forward-looking statements are based on current expectations, estimates, forecasts and projections and management’s current beliefs and assumptions and, accordingly, are not guarantees of future performance. Such forward-looking statements, and all phases of Casella’s operations, involve a number of risks and uncertainties, any one or more of which could cause actual results to differ materially from those described in Casella’s forward-looking statements. There are a number of important risks and uncertainties that could cause Casella’s actual events to differ materially from those indicated or implied by such forward-looking statements. These additional risks and uncertainties include, without limitation, risks related to the actions of JCP and other activist stockholders, including the amount of related costs incurred by Casella and the disruption caused to Casella’s business activities by these actions and those risks detailed in Item 1A, “Risk Factors” in Casella’s Form 10-KT for the transition period ended December 31, 2014, in its Form 10-Q for the quarterly period ended June 30, 2015 and in its subsequent filings with the SEC. Accordingly, you should not rely upon forward-looking statements as a prediction of actual results. Casella undertakes no obligation to update publicly any forward-looking statements whether as a result of new information, future events or otherwise, except as required by law. Important Information And Where To Find It Casella, its directors and certain of its executive officers are deemed to be participants in the solicitation of proxies from Casella’s stockholders in connection with the matters to be considered at Casella’s 2015 Annual Meeting of Stockholders. On September 22, 2015, Casella filed a definitive proxy statement and accompanyingdefinitive WHITEproxy card with the Securities and Exchange Commission (“SEC”) in connection with the solicitation of proxies from Casella stockholders in connection with the matters to be considered at Casella’s 2015 Annual Meeting of Stockholders. Information regarding the identity of participants, and their direct or indirect interests, by security holdings or otherwise, is set forth in such definitive proxy statement, including the schedules and appendices thereto.INVESTORS AND STOCKHOLDERS ARE STRONGLY ENCOURAGED TO READ THE PROXY STATEMENT, THE ACCOMPANYING WHITE PROXY CARD AND OTHER DOCUMENTS FILED BY CASELLA WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY WHEN THEY BECOME AVAILABLE AS THEY WILL CONTAIN IMPORTANT INFORMATION.Stockholders may obtain the definitive proxy statement, any amendments or supplements to the definitive proxy statement, the accompanyingdefinitive WHITEproxy card, and any other documents filed by Casella with the SEC for no charge at the SEC’s website at www.sec.gov. Copies are also available at no charge at the Investor Relations section of Casella’s corporate website at www.casella.com, by writing to Casella’s Corporate Secretary at Casella Waste Systems, Inc., 25 Greens Hill Lane, Rutland, VT 05701, or by calling Casella’s Corporate Secretary at (802)772-2257. Disclaimer Casella has neither sought nor obtained the consent from any third party to use any statements or information contained in this letter that have been obtained or derived from statements made or published by such third parties. Any such statements or information should not be viewed as indicating the support of such third parties for the views expressed herein. Non-GAAP Financial Measure As noted above, in addition to disclosing financial results prepared in accordance with Generally Accepted Accounting Principles in the United States (“GAAP”), Casella also discloses earnings before interest, taxes, depreciation and amortization, adjusted for accretion, depletion of landfill operating lease obligations, gain on sale of assets, development project charge write-offs, legal settlement costs, tax settlement costs, bargain purchase gains, asset impairment charges, environmental remediation charges, severance and reorganization costs, (gains) expenses from divestiture, acquisition and financing costs, gains on the settlement of acquisition related contingent consideration, fiscal year-end transition costs, proxy contest costs, as well as impacts from divestiture transactions (“Adjusted EBITDA”) which is a non-GAAP measure. Adjusted EBITDA is reconciled to net income (loss). Non-GAAP financial measures are not in accordance with or an alternative for GAAP. Adjusted EBITDA should not be considered in isolation from or as a substitute for financial information presented in accordance with GAAP, and may be different from Adjusted EBITDA presented by other companies. [Please see multimedia asset 4.] Casella is being advised in connection with the proxy contest by Wilmer Cutler Pickering Hale and Dorr LLP and Morgan, Lewis & Bockius LLP. Mackenzie Partners, Inc. is serving as Casella’s proxy solicitor. About Casella Waste Systems, Inc. Casella Waste Systems, Inc., headquartered in Rutland, Vermont, provides solid waste management services consisting of collection, transfer, disposal, and recycling services in the northeastern United States. For further information, investors may contact Ned Coletta, Chief Financial Officer at (802) 772-2239; media may contact Joseph Fusco, Vice President at (802) 772-2247; and anyone may visit the Company's website at http://www.casella.com. Forward-Looking Statements Certain matters discussed in this press release are “forward-looking statements” intended to qualify for the safe harbors from liability established by the Private Securities Litigation Reform Act of 1995. These forward-looking statements can generally be identified as such by the context of the statements, including words such as “believe,” “expect,” “anticipate,” “plan,” “may,” “would,” “intend,” “estimate,” “guidance” and other similar expressions, whether in the negative or affirmative. Similarly, statements that describe the objectives, plans or goals of Casella are forward-looking. Such forward-looking statements include, but are not limited to, statements regarding the anticipated proxy contest by JCP Investment Management, LLC and the other participants in its solicitation, Casella’s initiatives to improve the Company’s performance and increase its growth and profitability, Casella’s future operational and financial performance, Casella’s actions taken or contemplated to enhance its long-term prospects and enhance value for its stockholders, Casella’s efforts to execute on and implement its strategic plan, Casella’s plans to simplify its business structure, Casella’s actions taken or contemplated with respect to corporate and board governance, Casella’s plans to improve its cash flows and reduce its risk exposure by divesting or closing operations that do not fit within its core strategy, Casella’s plans to strengthen its balance sheet, promote financial flexibility and position the Company to achieve its target growth trajectory and Casella’s plans to achieve its three (3) year financial objectives and to drive additional value creation for the benefit of all its stockholders. These forward-looking statements are based on current expectations, estimates, forecasts and projections and management’s current beliefs and assumptions and, accordingly, are not guarantees of future performance. Such forward-looking statements, and all phases of Casella’s operations, involve a number of risks and uncertainties, any one or more of which could cause actual results to differ materially from those described in Casella’s forward-looking statements. There are a number of important risks and uncertainties that could cause Casella’s actual events to differ materially from those indicated or implied by such forward-looking statements. These additional risks and uncertainties include, without limitation, risks related to the actions of JCP and other activist stockholders, including the amount of related costs incurred by Casella and the disruption caused to Casella’s business activities by these actions and those risks detailed in Item 1A, “Risk Factors” in Casella’s Form 10-KT for the transition period ended December 31, 2014, in its Form 10-Q for the quarterly period ended June 30, 2015 and in its subsequent filings with the SEC. Accordingly, you should not rely upon forward-looking statements as a prediction of actual results. Casella undertakes no obligation to update publicly any forward-looking statements whether as a result of new information, future events or otherwise, except as required by law. Important Additional Information And Where To Find It Casella, its directors and certain of its executive officers are deemed to be participants in the solicitation of proxies from Casella’s stockholders in connection with the matters to be considered at Casella’s 2015 Annual Meeting of Stockholders. On September 22, 2015, Casella filed a definitive proxy statement and accompanyingdefinitive WHITEproxy card with the Securities and Exchange Commission (“SEC”) in connection with the solicitation of proxies from Casella stockholders in connection with the matters to be considered at Casella’s 2015 Annual Meeting of Stockholders. Information regarding the identity of participants, and their direct or indirect interests, by security holdings or otherwise, is set forth in such definitive proxy statement, including the schedules and appendices thereto.INVESTORS AND STOCKHOLDERS ARE STRONGLY ENCOURAGED TO READ THE PROXY STATEMENT, THE ACCOMPANYING WHITE PROXY CARD AND OTHER DOCUMENTS FILED BY CASELLA WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY WHEN THEY BECOME AVAILABLE AS THEY WILL CONTAIN IMPORTANT INFORMATION.Stockholders may obtain the definitive proxy statement, any amendments or supplements to the definitive proxy statement, the accompanyingdefinitive WHITEproxy card, and any other documents filed by Casella with the SEC for no charge at the SEC’s website at www.sec.gov. Copies are also available at no charge at the Investor Relations section of Casella’s corporate website at www.casella.com, by writing to Casella’s Corporate Secretary at Casella Waste Systems, Inc., 25 Greens Hill Lane, Rutland, VT 05701, or by calling Casella’s Corporate Secretary at (802)772-2257. 1 Calendar Year 2015 Guidance as updated/reaffirmed on 7/29/15. 2 Casella presents Adjusted EBITDA, a non-GAAP measure, because it considers it an important supplemental measure of its performance and believes it is frequently used by securities analysts, investors and other interested parties in the evaluation of Casella’s results. Management uses Adjusted EBITDA to further understand Casella’s “core operating performance.” Casella believes its “core operating performance” is helpful in understanding its ongoing performance in the ordinary course of operations. Casella believes that providing Adjusted EBITDA to investors, in addition to the corresponding income statement measures, affords investors the benefit of viewing its performance using the same financial metrics that the management team uses in making many key decisions and understanding how the core business and its results of operations has performed. Casella further believes that providing this information allows its investors greater transparency and a better understanding of its core financial performance. In addition, the instruments governing Casella’s indebtedness use EBITDA (with additional adjustments) to measure its compliance with covenants. Please refer to the appendix for further information on our use of non-GAAP measures, including a reconciliation of Adjusted EBITDA to net income (loss). Net income (loss) for the periods presented above was ($54.4) for the fiscal year ended 4/30/13, ($27.4) for the fiscal year ended 4/30/14, ($29.1) for the calendar year ended 12/31/14 and ($12.1) for the twelve months ended June 30, 2015. |

We have improved our performance and reduced exposure to risk by divesting or closing operations that did not fit within our core strategy and by focusing management’s attention and Casella’s capital resources on core operations to drive continued growth. Put plainly, by focusing on our core operations, we have significantly improved performance -- and we believe that our focused strategy provides a strong backbone for additional value creation.

We have improved our performance and reduced exposure to risk by divesting or closing operations that did not fit within our core strategy and by focusing management’s attention and Casella’s capital resources on core operations to drive continued growth. Put plainly, by focusing on our core operations, we have significantly improved performance -- and we believe that our focused strategy provides a strong backbone for additional value creation.|

JCP Dissent HOUSTON, April 28, 2015 /PRNewswire/ --JCP Investment Management, LLC ("JCP"), a significant shareholder of Casella Waste Systems,Inc. ("Casella" or the "Company") with aggregate ownership of approximately 5.0% of its outstanding Class Ashares, announced today it had formally notified Casella back on April 7, 2015 of its intention to seek the election of three independent, highly-qualified director candidates to the Board of Directors of Casella (the "Board") at the upcoming 2015 annual meeting of Casella shareholders (the "2015 Annual Meeting"). JCP is seeking Board change because we are dedicated to maximizing shareholder value and improving corporate governance at Casella and we are confident that enhancing the Board is a critical first step towards these goals.In our view, Casella is deeply undervalued as a result of poor investment and operational decisions and a dual capital structure that has eroded shareholder rights and value. We believe substantial shareholder representation is needed on the Board to ensure that appropriate actions are taken to drive better financial performance and create value for all shareholders. We are puzzled that having had almost a month's notice of our nominees' candidacy, and having interviewed them recently, the Board has nevertheless taken the questionable step of delaying its annual meeting of shareholders until an undefined date in the future. The Board claims it needs the delay to identify candidates with "industry experience." Notably, this is precisely what JCP's nominees offer to bring to the Board. Two of our three nominees are proven waste management industry leaders with extensive experience in the field. It is alarming that rather than allow shareholder representation in the boardroom and let shareholders vote in a timely manner on the candidates they believe will best represent their interests, this Board is trying instead to preempt shareholder input by adding to the Board candidates of their own choosing and postponing indefinitely shareholders' opportunity to vote on the matter. We strongly advise against any unilateral Board changes prior to a shareholder vote at the 2015 Annual Meeting. Such actions are inconsistent with a Board that open-mindedly and in good faith welcomes shareholder input. We continue to be open, as we always have been, to a constructive engagement with the Board, but will closely monitor the Board's actions to ensure they are driven by the best interests of Casella shareholders above all. Disappointing Total Shareholder Return (TSR) The current Board has presided over a prolonged underperformance. Casella continues to lack a strategically coherent plan to stop the value destruction. Casella's Total Shareholder Returns over the last -1, -3, -5 and -10-year periods on an absolute basis and relative to its peers and the S&P 500 Index have been abysmal. The Company has delivered negative returns to shareholders over many consecutive years.

Republic Services, Waste Management and Waste Connections have successfully: (1) controlled their debt load, (2) issued dividends and (3) produced significant value to their shareholders over the last 10 years. Casella has accomplished none of the above over the last 10 years. Since Casella's initial public offering in October 1997, the Company's stock price has declined by a staggering 70% to $5.38 per share as of market close on April 27, 2015 from $18.00 at the time of the IPO. Nearly half of the incumbent directors have been on the Board since the IPO and oversaw this massive destruction of shareholder value under their watch. Abysmal Corporate Governance The Company has a dual class capital structure that creates a gap between the economic investment of shareholders and their voting power. The Class B shares which have 10 votes per share are 100% held by John and Doug Casella. Such an unbalanced capitalization structure effectively allows insider control with a lesser economic stake in the Company and significantly impairs the rights of public shareholders. Furthermore, according to our research total payments to John and Doug Casella from related party transactions with the Company over the past 10 years aggregate to more than $70 million. The Board is classified and stale. Average incumbent tenure is over 14 years, with 4 directors having been on the Board for more than 20 years and only one addition (Emily Nagle Green) in the past 7 years. Absence of proactive change on the Board has been coupled with severe restrictions on the ability of shareholders to effect Board change. Shareholders are prohibited from calling special meetings and cannot act by written consent, which effectively means shareholders cannot seek Board change between annual meetings. Not surprisingly, leading proxy advisory firm, Institutional Shareholders Services (ISS) has raised high concerns with Casella's corporate governance and has assigned the Company a governance score of 9 out of 10 (with 10 being the highest governance concern). Poor Operational and Financial Performance Casella has suffered multi-year stagnation in cash flows and EBITDA while the rest of the industry continues to show growth and solid capital allocation. In 2005, Casella's EBITDA was approximately $107 million. Today, the Company forecasts approximately $105 million in EBITDA for 2015, showing a deterioration rather than growth in the past decade. Over that 10-year period, Casella has produced approximately $900 million to $1 billion in EBITDA and more than $600 million in cash flow from operations. Yet public shareholders have not seen a dime. Capital allocation through organic growth and acquisitions has not produced additional earning power and the Company has paid out more than $70 million to entities controlled by John and Doug Casella. Over this same time period, the share count has increased more than 60% without any increase in earning power. Shareholders continue to experience dilution, with the most recent issuance in September 2012. Summary As a significant shareholder of Casella, JCP has serious concerns with the chronic underperformance of the Company and the inability or unwillingness of this Board to take the right steps to enhance shareholder value. In our view, the underlying cause for these problems is a capitalization structure and decision-making construct that is heavily skewed to protect insiders at the expense of public shareholders. This has led in our view to complacency on the Board and lack of urgency in delivering value for public shareholders. Public shareholders must have a voice in the boardroom to ensure that decisions are made with their best interests in mind. We find it insincere that this Board which has resisted change for so long and has erected barriers to shareholder-initiated improvements to the Board, is now purporting to proactively seek candidates for addition to the Board and is delaying a critically important shareholder referendum on their performance, only now that they are facing shareholder pressure from JCP. We also question their purported explanation that they need time to find candidates with "industry experience" when JCP has identified two highly qualified candidates with impressive industry experience. We always have been, and remain, open to constructive engagement with the Board. We intend to continue to work hard to reach an amicable resolution on Board composition. However, to the extent that no agreement is reached, we will not hesitate to take all actions we believe necessary to protect the best interests of ALL Casella shareholders. JCP nominees are: Brett W. Frazier – currently retired after serving in multiple executive roles for Waste Management, Inc. ("Waste Management"), North America's leading provider of comprehensive waste management environmental services, from 2000 until July 2012. Mr. Frazier most recently served as Senior Vice President – Southern Group, where he had full P&L accountability for Waste Management's largest and most profitable operating group, and Senior Vice President – Eastern Group, where he had full P&L responsibility for the 13 states in the Northeast. From 1980 until 1999, Mr. Frazier held various leadership roles with Browning-Ferris Industries, Inc. (BFI Waste Services), formerly the second largest solid waste disposal company in the world, including Area Vice President – Marketing and Sales and Vice President of Investor Relations. Mr. Frazier's professional experience also includes serving as a Regional Vice President for TruGreen Limited Partnership, America's top lawn care company based on market share. Mr. Frazier earned an MBA from Tulane University. Mr. Frazier's extensive leadership experience and expertise in the waste management services industry will make him a valuable addition to the Board. James C. Pappas – Managing Member of JCP Investment Management, LLC and the sole member of JCP Investment Holdings, LLC. Mr. Pappas has also served as a director of Jamba, Inc., a leading health and wellness brand and the leading retailer of freshly squeezed juice, since January 2015. Previously, Mr. Pappas served as a director of The Pantry, Inc., a leading independently operated convenience store chain in the southeastern United States and one of the largest independently operated convenience store chains in the country, from March 2014 until the completion of its sale in March 2015.He also previously served as Chairman of the Board of Morgan's Foods, a then publicly traded company, from January 2013 until May 2014, when the company was acquired by Apex Restaurant Management, Inc., after initially joining as a director in February 2012. Mr. Pappas also served as a director of Samex Mining Corp, a junior resource company, in 2013. Previously, Mr. Pappas was with the Investment Banking / Leveraged Finance Division of Goldman Sachs Group, Inc. where he advised private equity groups and corporations on appropriate leveraged buyout, recapitalization and refinancing alternatives, and prior to that with Banc of America Securities, where he focused on Consumer and Retail Investment Banking, providing advice on a wide range of transactions including mergers and acquisitions, financings, restructurings and buyside engagements. Mr. Pappas received a BBA, and a Masters in Finance from Texas A&M University. Mr. Pappas' significant experience in the valuation and management of investment securities in addition to his experience in investment banking and corporate finance from his career with major investment banking firms will enable him to provide invaluable oversight to the Board. Joseph B. Swinbank – Partner of each of Sprint Waste Services LP, a waste collection and disposal company and the largest privately owned trash hauler in the Houston area with approximately $100 million in revenue, Sprint Fort Bend County Landfill, L.P., a Type IV landfill facility in Texas, Sprint Sand and Clay, LLC, a provider of sand and clay to various industries, and Sprint Transport, LLC, a tank trailer transport company. Mr. Swinbank also currently serves as a director of Community Bank of Texas and was a Founding Director of Vista Bank from 2006 until its merger with Community Bank of Texas in August 2013. From 2004 until its sale in March 2012, Mr. Swinbank served as a Partner of Sprint Pipeline Services, LP, a construction and maintenance company. Mr. Swinbank's professional experience includes 41 years as an entrepreneur involved in the transportation, environmental services, frac tank rental, mining, safety and construction materials industries. Mr. Swinbank earned a B.S. in Agricultural Economics from Texas A&M University. Mr. Swinbank's track-record of building and leading successful businesses, including in the waste management industry, well qualifies him to serve on the Board. CERTAIN INFORMATION CONCERNING PARTICIPANTS JCP Investment Management, LLC, together with the participants named herein, intends to file a preliminary proxy statement and accompanying proxy card with the Securities and Exchange Commission ("SEC") to be used to solicit votes for the election of their slate of three highly-qualified director nominees at the 2015 annual meeting of stockholders of Casella Waste Systems, Inc., a Delaware corporation (the "Company"). JCP INVESTMENT MANAGEMENT STRONGLY ADVISES ALL SHAREHOLDERS OF THE COMPANY TO READ THE PROXY STATEMENT AND OTHER PROXY MATERIALS AS THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. SUCH PROXY MATERIALS WILL BE AVAILABLE AT NO CHARGE ON THE SEC'S WEB SITE AT HTTP://WWW.SEC.GOV. IN ADDITION, THE PARTICIPANTS IN THIS PROXY SOLICITATION WILL PROVIDE COPIES OF THE PROXY STATEMENT WITHOUT CHARGE, WHEN AVAILABLE, UPON REQUEST. REQUESTS FOR COPIES SHOULD BE DIRECTED TO THE PARTICIPANTS' PROXY SOLICITOR. The participants in the proxy solicitation are JCP Investment Partnership, LP ("JCP Partnership"), JCP Single-Asset Partnership, LP ("JCP Single-Asset"), JCP Investment Partners, LP ("JCP Partners"), JCP Investment Holdings, LLC ("JCP Holdings"), JCP Investment Management, LLC ("JCP Management"), James C. Pappas, Brett W. Frazier and Joseph B. Swinbank (collectively, the "Participants"). As of the date hereof, JCP Partnership beneficially owned 1,483,435 shares of Class A Common Stock, $0.01 par value per share ("Common Stock"). As of the date hereof, JCP Single-Asset beneficially owned 496,670 shares of Common Stock. JCP Partners, as the general partner of each of JCP Partnership and JCP Single-Asset, may be deemed the beneficial owner of the 1,980,105 shares of Common Stock owned in the aggregate by JCP Partnership and JCP Single-Asset. JCP Holdings, as the general partner of JCP Partners, may be deemed the beneficial owner of the 1,980,105 shares of Common Stock owned in the aggregate by JCP Partnership and JCP Single-Asset. JCP Management, as the investment manager of each of JCP Partnership and JCP Single-Asset, may be deemed the beneficial owner of the 1,980,105 shares of Common Stock owned in the aggregate by JCP Partnership and JCP Single-Asset. Mr. Pappas, as the managing member of JCP Management and sole member of JCP Holdings, may be deemed the beneficial owner of the 1,980,105 shares of Common Stock owned in the aggregate by JCP Partnership and JCP Single-Asset. As of the date hereof, Messrs. Frazier and Swinbank did not beneficially own any shares of Common Stock. About JCP Investment Management: JCP Investment Management, LLC is an investment firm headquartered in Houston, TX that engages in value-based investing across the capital structure. JCP follows an opportunistic approach to investing across different equity, credit and distressed securities largely in North America. Investor Contacts: James C. Pappas John Glenn Grau SOURCE JCP Investment Management, LLC |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||