Vermont Business Magazine The ski industry has changed profoundly, but the long-term leases intended to boost this vital Vermont economic engine have not changed with it. Vermont State Auditor Doug Hoffer has released the findings of an investigation into the state’s land leases with seven ski resorts. The central aim of the inquiry was to evaluate the direct financial return to the public of the state leasing these unique land assets.

The 50- to 100-year leases stem from the mid-20th century and concern roughly 8,500 acres of public land on some of Vermont’s most iconic mountains, including Mount Mansfield, Jay Peak, and Killington Peak. The leases are aimed at promoting recreational sports and facilities in Vermont. They were designed to help resorts grow, while generating revenue for Vermont state parks and forests. According to the report, those lease revenues, however, have not kept pace with the resorts’ development.

“By most measures, this partnership has been a success, and our Green Mountains are now home to world-famous ski areas,” Auditor Hoffer said. “But the dramatic changes in the resort industry over the past half-century suggest the need to review the current leases, which stretch back to the presidency of Dwight D Eisenhower.”

“By most measures, this partnership has been a success, and our Green Mountains are now home to world-famous ski areas,” Auditor Hoffer said. “But the dramatic changes in the resort industry over the past half-century suggest the need to review the current leases, which stretch back to the presidency of Dwight D Eisenhower.”

Over the last half-century, locally owned resorts with several lifts and a few facilities have been transformed into year-round enterprises – some of which are now owned by large out-of-state corporations. Today’s resorts feature new lodges, hotels, condominiums, golf courses, retail stores, waterparks, and other high-end amenities.

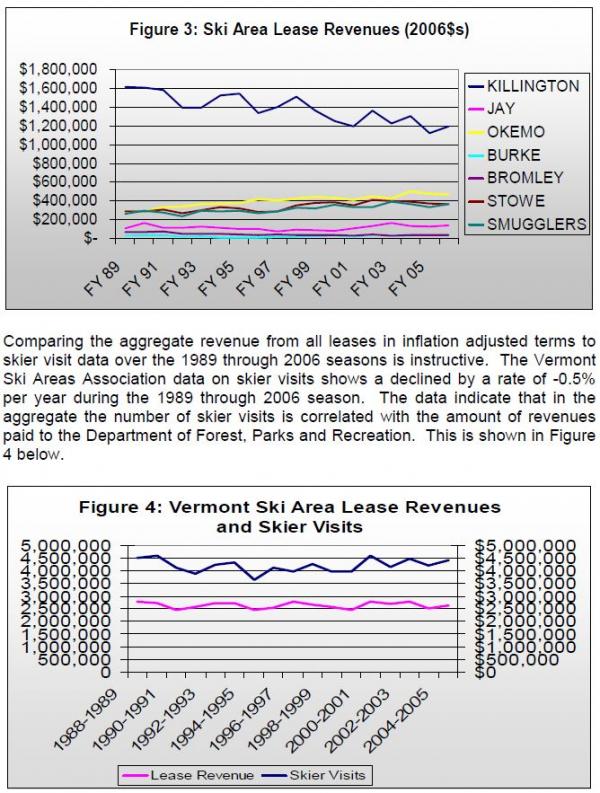

Between 2003 and 2013, development at the seven resorts spurred increases in sales of goods and services, property values, and revenues from excise taxes. But lease payments over this decade fell when adjusted for inflation. The leases were designed to capture a certain percentage of the primary revenue source, which 50 years ago was lift tickets. As the resorts have evolved, that revenue source has become one of many.

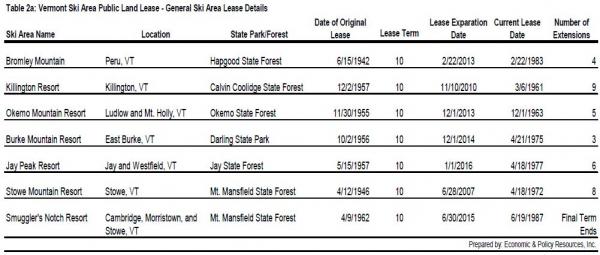

The leases were also created in a piecemeal fashion. They are written in non-standard terms and are inconsistent across key criteria, such as lease lengths, indemnity clauses, remedies for a breach of contract, and audit provisions. The lack of uniformity between the leases has produced a system that is difficult to administer and generates added costs for taxpayers.

One of the most problematic of the inconsistencies is the variation in assigning title to property on state land, which obstructs two towns’ power to tax and gives some resorts a tax advantage because property that belongs to the State is tax-exempt. Vermonters therefore pay for land and facilities used by the ski areas through the State’s Payment in Lieu of Taxes programs, which reimburses municipalities for taxes lost from state-owned property. These payments for property used and developed by the resorts reduce the value of the lease revenues to the State.

Additionally, when the State negotiated these lease agreements, it made a critical error by not stipulating regular opportunities to update the agreements, as the federal government does in its standardized 40-year permits with ski areas. The dated liability insurance language in the leases is one example of antiquated requirements and terminology that poses potential risk for the State.

“Our review points to old lease terms that may not be suitable for today and questions whether taxpayers are receiving fair value for these spectacular public assets,” Auditor Hoffer said. “It is my hope that this report will stimulate a discussion about all of these issues.”

Click here to read the full report “State Land Leases Boost Ski Industry, but Are Dated and Inconsistent” and watch a video overview above.

Source: State Auditor. 1.20.2015