by Timothy McQuiston Vermont Business Magazine This historically long and slow recovery is beginning to reveal real growth in the economy, with many of the downside risks theoretical and the upside risks looking pervasive, at least for now. For instance, economist Tom Kavet said, global oil prices, which have cratered over the last year, look like they will remain low through 2016, which will continue to save consumers on gasoline, home heating and associated costs. The stock market, corporate profits and a low unemployment rate are all good for individuals, businesses and government.

Kavet gave his revenue and economic forecast to the Vermont Legislature December 1. Kavet has been the state economist and principal economic advisor to the Vermont State Legislature since 1996. He is a partner with the Williamstown consulting firm Kavet, Rockler & Associates, LLC.

Kavet gave his revenue and economic forecast to the Vermont Legislature December 1. Kavet has been the state economist and principal economic advisor to the Vermont State Legislature since 1996. He is a partner with the Williamstown consulting firm Kavet, Rockler & Associates, LLC.

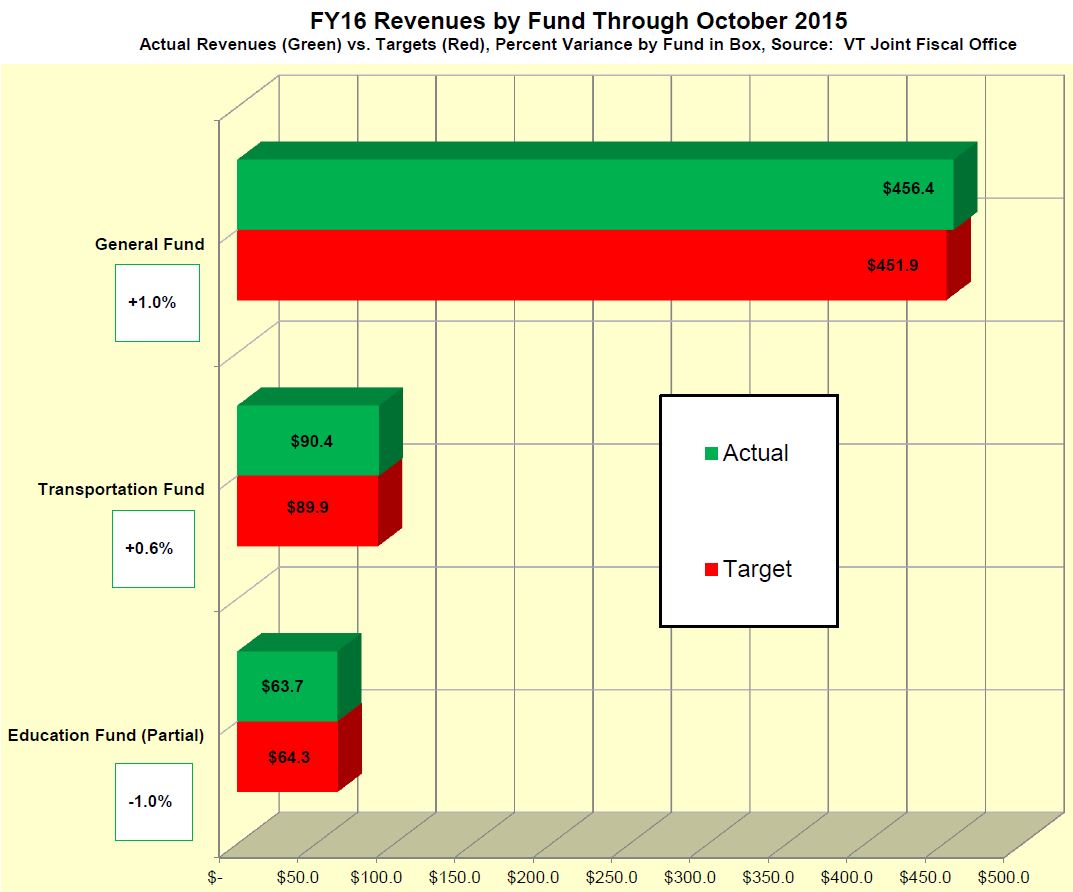

He reported that state tax revenues are slightly ahead of the forecast for this fiscal year, which began July 1.

Armed with that information, the Emergency Board on Tuesday approved GovernorPeter Shumlin’s recommendation to increase the cap on the Vermont Employment Growth Incentive for projects in economically distressed regions of Vermont from $1 million to $1.5 million for 2016. The approval allows for consideration of proposals that could, if approved, create 200 new full-time jobs and $6.5 million in new payroll, he said. The E-Board is comprised of the governor and the chairs of the four money committees in the Legislature.

“Allowing increased incentives for these regions of the state means job creation and opportunity for Vermonters where it is most needed without additional cost to the rest of the state,” Shumlin said.

Regions of the state that have historically higher-than-state-average unemployment and lower-than-state-average wages are eligible for increased incentives under the Vermont Employment Growth Incentive (VEGI) program. Applications to the Vermont Economic Progress Council (VEPC) from businesses proposing job creation and investment projects in these regions have recently increased, causing the cap to be reached.

Regions of the state that have historically higher-than-state-average unemployment and lower-than-state-average wages are eligible for increased incentives under the Vermont Employment Growth Incentive (VEGI) program. Applications to the Vermont Economic Progress Council (VEPC) from businesses proposing job creation and investment projects in these regions have recently increased, causing the cap to be reached.

Two of the proposed projects are in the Northeast Kingdom. Even with the higher incentive approvals, these projects will also generate an estimated half a million dollars in net new revenue to the state.

Companies are paid VEGI incentives - over an extended period of time –onlyif the new, full-time jobs and payroll are created and maintained and capital investments are made. New tax revenues flow to the state from this economic activity before incentives are paid to the company and, in the end, the state receives more new tax revenue than is paid out in incentive payments.

“We want to raise that cap so we can grow more jobs and grow that payroll,” the governor said.

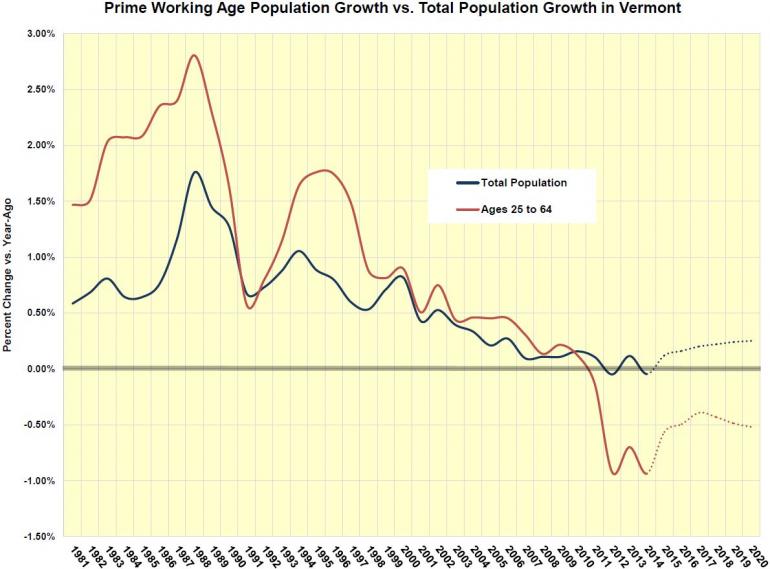

In his presentation, Kavet said meaningful vigor in the economy during the recovery has been elusive. For instance, Kavet said, wages and home prices continue to lag, despite tight labor and real estate markets. Vermont is making babies at a slower rate than any state in the nation except New Hampshire. Indeed, the Northeast has a very slow population growth. Consequently the state is getting older and the number of “working age” Vermonters is actually declining.

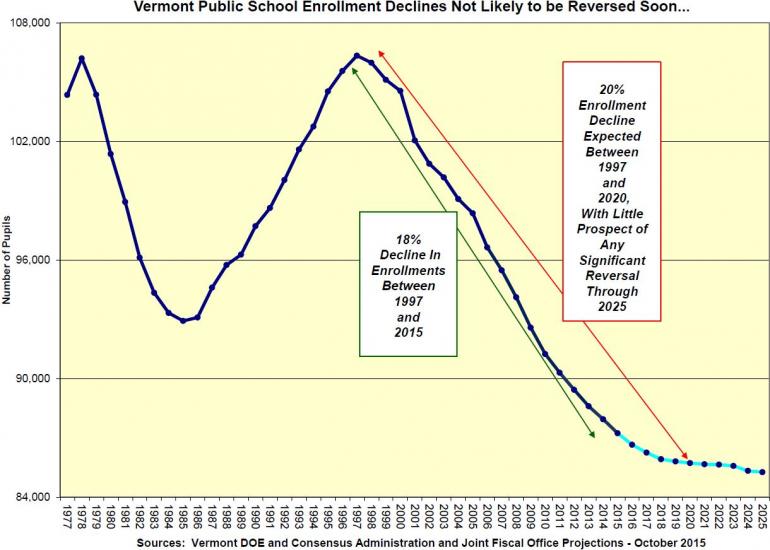

Education cost increases have slowed, but the population of school-age children continues to decline.

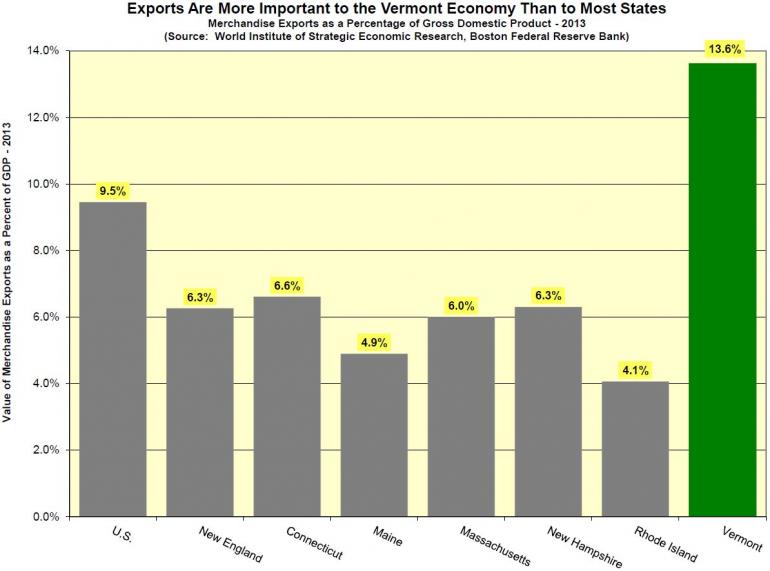

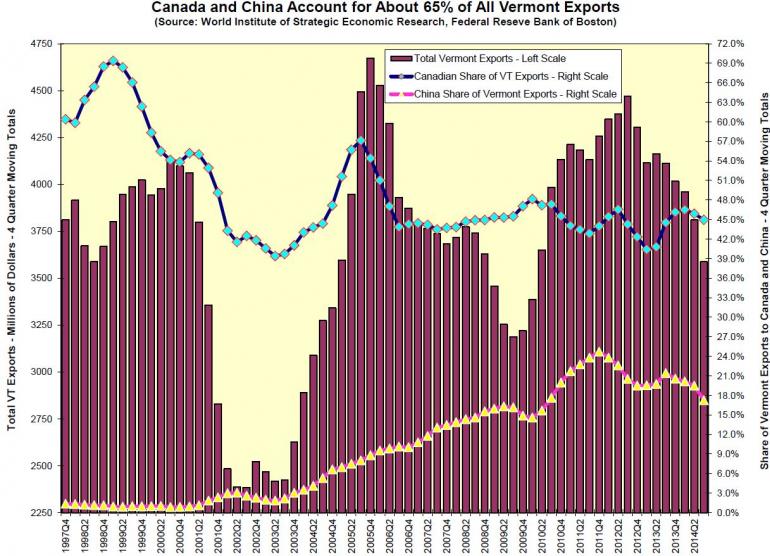

And one of Vermont’s economic strengths – exports – has suffered because of the strength of the dollar. Canadian tourism, according to anecdotal reports, has also suffered, even though tourism overall has benefitted from cheaper gas prices and a growing (albeit slowly) economy.

And there is also the nagging issue of increasing wage disparity across the country.

Here are Kavet’s bullet points from his presentation to the Legislature. (CLICK FOR FULL REPORT)

The Current Economic Recovery is Beginning to Make Up in Duration What it has Lacked in both Vigor and Speed…

•After 77 months, the current economic expansion is among the longer expansionary periods in business cycle history

•Despite significant vulnerabilities, especially global economic weakness, major imbalances that could lead to recession in 2016 are not evident

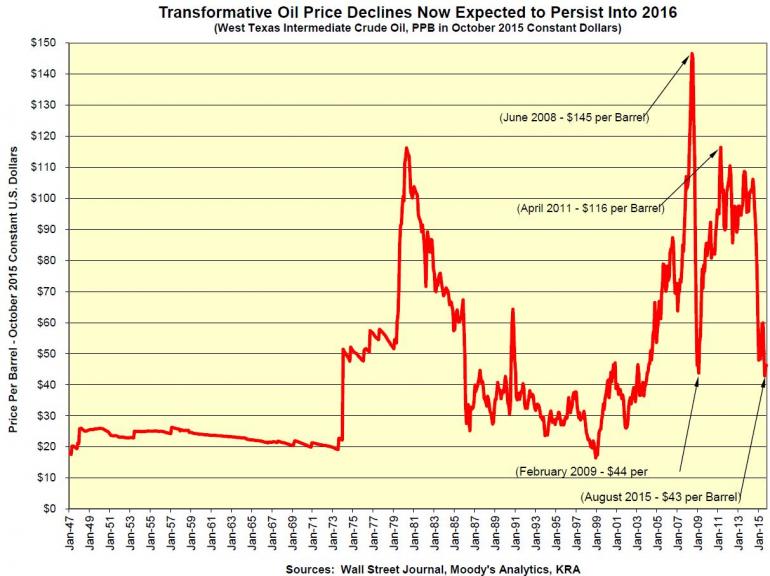

•The gradual recovery in home prices and soaring equity markets will bolster household wealth and along with continued low energy prices in 2016, will support consumer spending – 70% of the economy

•Lower energy prices in Vermont could shave nearly $700 million off the 2016 energy bill expected as of 2014 – a savings of more than $2,600 per Vermont household

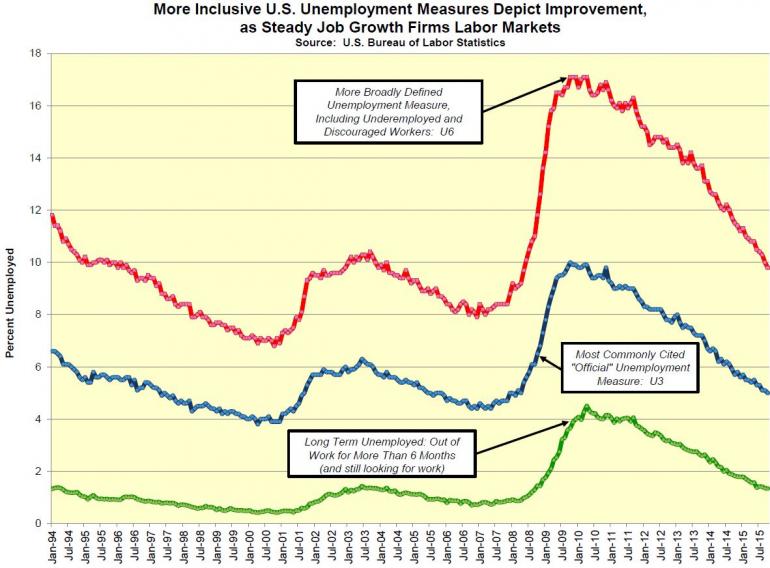

•More than 13 million jobs have been added since February of 2010, pushing the U.S. unemployment rate to 5.0% in October. Whereas there were 7 people looking for work for every job opening in late 2009, the figure is currently about 1.5 – close to prior lows last seen in 2007. “Full employment” is now expected to be reached in mid-2016

•This will soon translate into upward pressure on real wages, which have been stagnant throughout the recovery

•Inflation has been tame as energy prices remain subdued

Labor Markets Are Approaching Full Employment

Labor Markets Are Approaching Full Employment

•Total U.S. nonagricultural employment has increased for 61 consecutive months and after losing 8.7M jobs between January 2008 and February 2010, the U.S. economy has now regained more than 13M jobs, averaging more than 230,000 jobs per month during the past 12 months

•Vermont payroll employment finally topped its pre-recession peak in June of 2014 and is currently about 18,500 jobs above its recessionary trough, reached in July of 2009

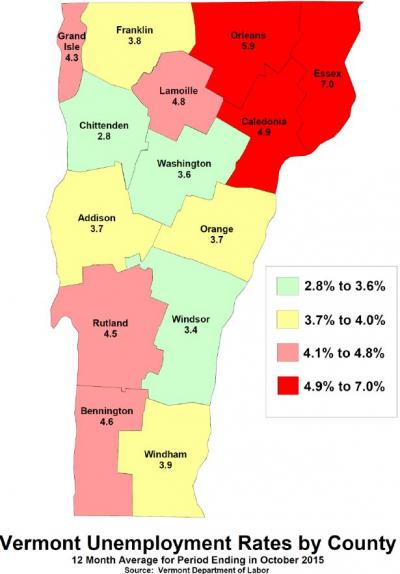

•Vermont’s unemployment rate is still among the top ten U.S. states, at 3.7%; however, it has been surpassed in the last two months in New England by New Hampshire, currently at 3.3%

•Initial Claims for Unemployment Insurance in Vermont dropped to their lowest levels in more than 25 years in September and portend continued improvement in the State labor market

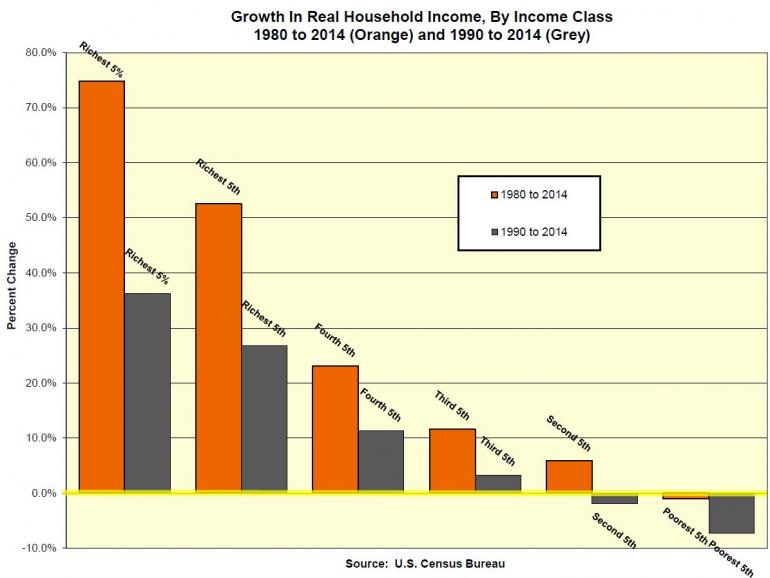

•Real wage and income growth has remained flat or negative for lower income groups, with virtually all recent gains in income accruing to the highest income quintile

•Although chronic unemployment is reflected in a still elevated share of long-term unemployed workers, almost every measure of unemployment has improved in the last year.

Real Estate Markets have Bottomed Out but Full Recovery is Still Elusive

Real Estate Markets have Bottomed Out but Full Recovery is Still Elusive

•Real estate markets are characterized by pronounced cyclicality and regional variation

•For the sixth consecutive quarter, housing prices increased on a year over year basis in every U.S. state. As of the third quarter of 2015 (the most recent available), 19 states equaled or exceeded their pre-recession peak levels (ND, DC, TX, CO, SD, NE, AK, IA, OK, LA, WY, KY, KS, MT, TN, WV, IN, HI and AR)

•Vermont is the closest New England state to exceeding its pre-recession valuations, currently just 0.8% shy of this. The next closest NE state is Massachusetts, which, despite recovering 15% above its recessionary low, is still about 5% below its prior peak. Continued home price weakness in surrounding regional states, especially CT, MA, NY and NJ, will affect second home markets in Vermont, via wealth effects

•Real estate markets attracting international investment – especially large US cities - have experienced some of the strongest price appreciation of late

•As previously forecast, the Vermont Property Tax base (Grand List) will not exceed 2009 peak levels until 2017, putting continued pressure on tax rates to cover rising education costs.

The Economy is About People: Vermont Demographics

•A major new State demographic analysis is currently being undertaken by JFO and Administration economists, using detailed, and previously unavailable, Health Department data at the Town level. Output from this analysis should be available within the next year

•The movement over time of the “baby-boom” population bulge continues to dominate VT and U.S. demographics, and is responsible for the aging profile of both. The children of this large cohort, referred to as the “baby-boom echo,” represents a much more diffuse wave, as families have fewer children and at older ages

•Significant declines in fertility rates in the past 20 years have dropped Vermont births from about 8,000 per year in the early 1990’s to about 6,000 per year at present

•In addition to the large declines in enrollments experienced in the State over the past 20 years, these two demographic events have (since 2011) and will combine to create declines in the prime working age population, ages 25-64 over the next 20 years. This, in turn, will affect employment, earned income and selected tax revenues in the State

Forecast Risks Remain

•The age and tenuity of the recovery makes the current expansion more susceptible to external shocks, such as severe weather, Fed miscalculation and other policy mistakes, and external global economic crises (especially emanating from China and other emerging countries), including military conflict

•Prominent near-term hazards include continued strengthening of the U.S. dollar and attendant export weakness and domestic industrial stress. Vermont has already experienced a 24% decline in exports over the past three years, during this period of rising exchange rates. The exchange rate with Canada, our largest trading partner, has been particularly impacted, rising more than 35%

•Slumping productivity growth of late threatens to limit non-inflationary potential economic growth to under 1%. New business formations, despite ample credit, are also abnormally low – only slightly above recessionary lows. Unless these important components of economic health recover, it could cripple future growth

•Widening income distribution inequality in the U.S. will dampen demand and slow growth relative to “normal” demographic-based indicators

•The rapid recent rise in equity markets could make them vulnerable to correction and amplify impacts from other negative events affecting market valuations and/or psychology.