by Timothy McQuiston, Vermont Business Magazine The Vermont House of Representatives has taken a significant step to combat the state’s housing crisis with the passage (97-42) of H.829, which proposes to invest $100 million a year over the next 10 years on a broad range of housing needs. The legislation, primarily supported by creating a new income tax bracket for the wealthiest Vermonters, represents the latest in a series of House-approved bills committed to building affordable housing and ensuring that rental and homeownership are accessible for all Vermonters.

The bill outlines a ten-year plan to expand affordable housing options and essential housing services. It makes strategic investments in an updated Middle-Income Homeownership Program, bringing units online quickly through the successful Vermont Housing Improvement Program (VHIP), a new eviction protection program, increased permanent housing options for older Vermonters and Vermonters with developmental disabilities, refugee housing, and other housing needs.

If enacted, the bill would create a new tax bracket, increasing tax rates by 3% points on marginal income over $500,000 (which would be a 34.3% increase from 8.75% now to the higher 11.75%. See tables below). This tax change would raise over $74 million annually in state revenue and only affect the top 1.1% of Vermont taxpayers.

Advocates said that by taking a comprehensive approach, it tackles the immediate need for housing, and puts the state on a long-term trajectory to make affordable housing more attainable for all Vermonters.

"This is not just about building homes; it's about building communities and ensuring that every Vermonter has a place to call home," said Speaker Jill Krowinski. "When we commit to long-term strategic investments, families and working Vermonters are more stable, economies are stronger and communities more resilient. Vermont has seen a surge in income inequality since the pandemic. The rich are getting richer, and the middle class is disappearing. By asking our wealthiest Vermonters to pay a little more, we are able to invest in a historic affordable housing initiative to address the root causes of the housing crisis and provide lasting solutions for generations to come."

Key provisions of the bill include retaining and enhancing programs such as the Vermont Housing Improvement Program (VHIP), which has already rehabilitated over 500 units, and increasing investments in mobile and manufactured home parks. This long-term housing investment, coupled with the Act 250 modernization bill passed last week, is crucial in making sure that housing can become available rapidly and the cost of living can start to come down making Vermont more affordable.

"We’re making a plan to invest in housing at a time when failing to invest is not an option,” said Rep. Tom Stevens, chair of the House Committee on General and Housing. “This bill advances the policy and raises the revenue that’s needed to get the work done. That’s how we define leadership.”

STATE OF VERMONT LEGISLATIVE JOINT FISCAL OFFICE

To: Representative Kornheiser

From: Ted Barnett

Date: March 27, 2024

Subject: H.829 Amendment Fiscal Estimates

Sections 18-25: Property Transfer Tax

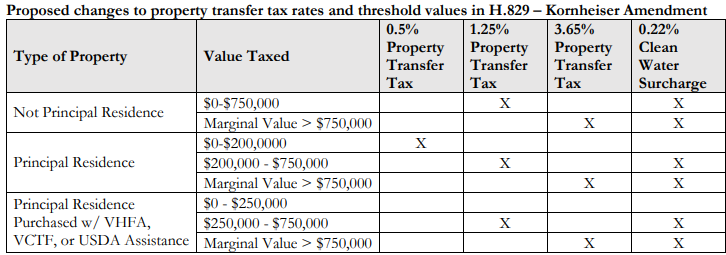

Section 18 would adjust threshold amounts for the property transfer tax (PTT). The bill would increase the $100,000 threshold value for the 1.25% general rate to $200,000 for principal residences, and from $110,000 to $250,000 for principal residences financed through VHFA, VCTF or USDA-RD housing programs. These exemptions are expected to cost $3.9 million annually. Section 18 also adds a 3.65% tax rate for the marginal value of transferred properties greater than $750,000, which would generate an additional $21.4 million per year. Together, these changes are estimated to result in $17.5 million in additional PTT revenue starting in fiscal year 2025.

Section 19 as recommended by Ways and Means would adjust the exemption from the Clean Water Surcharge from $100,000 to $200,000 in transfer value for principal residences and from $200,000 to $250,000 for principal residences financed through certain mortgage programs. As amended by Rep. Kornheiser, the bill would adjust that rate from 0.2% to 0.22%. Section 20 in the underlying bill would make conforming changes to account for the statutory adjustment to the Clean Water Surcharge rate starting in fiscal year 2028. The table below shows the new rates and threshold values as proposed in H.829. This adjustment in rate, combined with the changes to the Clean Water Surcharge exemptions outlined above would generate $60,000 in net revenue annually for the Clean Water Fund compared to current law.

Sections 21-24 propose changes to the allocation of PTT revenue. Under current statute, after bond payments and a 2% allocation to the Department of Property Valuation and Review (PVR) for administrative expenses, the Vermont Housing and Conservation Trust Fund (VCTF) receives 50% of PTT revenue, the Municipal and Regional Planning Fund (MRPF) receives 17%, and the General Fund receives 33%. These amounts have historically been notwithstood in the budget process.

The Kornheiser amendment would adjust percentage allocations of property transfer tax revenue. The Department of Tax allocation of overall revenue would be reduced from 2% to 1.5%. The General Fund portion would increase from 33 percent to 37 percent. The portion of revenues allocated to the Vermont Housing and Conservation Trust Fund would remain unchanged. Finally, the percentage allocated to the MRPF would decrease from 17 percent to 13 percent.

These percentage allocations are then notwithstood for fiscal year 2025, reflecting language and allocations from H.883, an act relating to making appropriations for the support of government. The base allocations of revenue to the VCTF and the MRPF would remain unchanged. The General Fund would receive an additional $17.5 million in revenue, which would then be allocated through the housing appropriations outlined in sections 3 through 15 of the bill.

Section 24 would exempt transfers of abandoned properties from the property transfer tax if the property is rehabilitated and used as a principal residence within three years of the transfer. The limited scope of the exemption means that very few properties meeting the criteria of “abandoned” will be transferred, leading to a negligible General Fund revenue impact starting in fiscal year 2025. Section 25 would exempt transfers of a new, energy efficient mobile home from the property transfer tax. The number of transfers of new mobile homes that are currently assessed the property transfer tax is limited, leading to a nominal loss in property transfer tax revenues compared to current law.

JFO March 21, 2024:

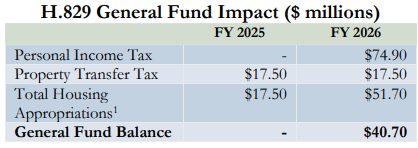

JFO estimates the bill would have various fiscal impacts starting in fiscal year 2025 for both the General Fund and the Clean Water Fund. The table below summarizes the General Fund impacts of the bill. In fiscal year 2025, revenue generated through the property transfer tax matches housing appropriations. In fiscal year 2026, the General Fund would receive $40.7 million after appropriations to housing programs from additional revenues generated by personal income and property transfer tax. Those funds are intended to be used for temporary emergency housing.

In addition to these General Fund impacts, the bill would also reduce Clean Water Fund revenues by $700,000 annually starting in fiscal year 2025.

1 A table in the background and details section of the fiscal note outlines the individual housing appropriations that would be made in the bill.

Section 26: Personal Income Tax

Section 26 would add a new top marginal bracket and tax rate for all filing statuses. The new top marginal bracket would tax filers at a rate of 11.75% on Vermont Taxable Income above:

• $410,650 for single filers,

• $500,000 for married filing jointly filers,

• $455,350 for head of household filers, and

• $250,000 for married filing separately filers. These new brackets would be effective starting in tax year 2025.

For more information on H.829, please visit the legislative website.

Source: 4.3.2024. Montpelier, VT - Office of the Speaker